- Nationwide multifamily rent growth is subdued, but Midwest and core metros are outperforming high-supply Sun Belt markets, per Yardi Matrix’s Summer 2026 Outlook.

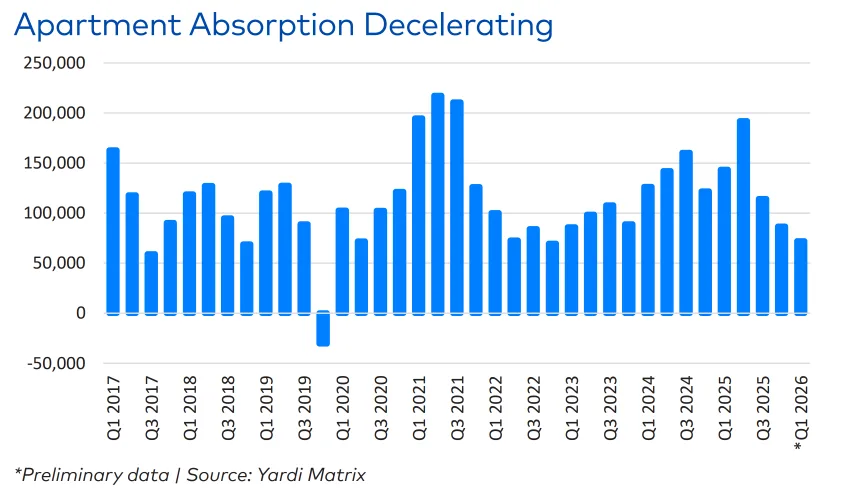

- Over 1.3M units remain in lease-up nationally as absorption lags, with below-average demand extending the timeline for rent recovery.

- Investors face limited acquisitions due to persistent bid-ask gaps, while robust debt market activity is dominated by refinancings rather than property sales.

Demand Outpaced by Supply Cycle Aftershocks

According to Yardi Matrix’s Summer 2026 Multifamily Outlook, the US multifamily sector faces muted recovery mid-year, with tepid demand set against a backdrop of persistent oversupply. National rent growth is modest and highly market-specific, with the Midwest and several core metros driving positive momentum. Meanwhile, Sun Belt and Mountain West markets continue to digest a historic supply wave that is weighing on new lease pricing. Although capital flows into multifamily remain strong, deal activity is constrained as sellers hold out for higher prices and investors hesitate in the absence of lower interest rates.

As 2026 progresses, more than 1.3M apartments nationally are in the lease-up phase, far surpassing the 2017–2019 norm, signaling ongoing pressure on rents and longer absorption timelines. With expectations of near-term interest rate cuts delayed by inflation and global uncertainty, portfolio managers are shifting focus to operational efficiency and niche segments rather than broad market gain.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Supply Glut Extends Rent Recovery Window

The multifamily sector is still feeling the impact of one of the largest development booms in decades, with more than 1.9M units delivered nationally between 2023 and 2025. While starts dropped by over a third in 2025—down from the 703,000-unit peak in 2022 to around 460,000 units in 2024 and 2025—the pipeline remains elevated. Yardi Matrix forecasts 488,000 new units will deliver in 2026, another 454,000 in 2027, and a slight uptick to 460,000 in 2028. Nearly 6.9% of the nation’s total apartment stock remains in lease-up, an unprecedented glut that will require time to absorb and keep a lid on rent increases.

The impact is most pronounced in the Sun Belt, where demand lags supply even as metros like Austin, Phoenix, and Charlotte show strong leasing activity. Markets with modest inventory growth—namely in the Midwest and key Northeast gateways—are outperforming as demand exceeds limited supply. These dynamics continue to drive divergence in rent performance across metros and asset types.

Regional Divergence Defines the Multifamily Map

The strongest rent growth is forecast in the Twin Cities (+4.6%), Chicago (+4.1%), Detroit (+4.0%), Kansas City (+3.9%), and Philadelphia (+2.9%), reflecting limited new deliveries and enduring affordability advantages. By contrast, Sun Belt cities like Phoenix (-6.2%), Denver (-5.9%), Austin (-5.2%), and Dallas (-4.3%) are still struggling to stabilize from the supply surge, with rents down sharply since 2023.

Leasing absorption has not kept pace with deliveries. National absorption in Q1 2026 was roughly 72,000 units—well below the 136,000 quarterly average of the prior two years and pre-pandemic averages of about 101,000 units. Recent data also show absorption slowing across parts of the Midwest and South, despite stronger rent trends in several metros. Despite negative rent growth, markets including Austin, Phoenix, and Raleigh–Durham continue to post some of the strongest leasing activity relative to inventory, underscoring the intensity of the supply/demand mismatch in those metros.

Why It Matters

For investors and operators, 2026 shows how excess supply keeps limiting rent growth nationwide. Yardi Matrix expects national rent growth to finish the year at just 0.5%. The Sun Belt faces the sharpest pressure after leading the last expansion cycle. Phoenix rents have dropped 14.7% since 2023. Austin rents fell 11.3% in the single-family rental segment alone. As a result, supply-heavy markets now report rent growth far below long-term averages. This shift has challenged assumptions from the early-2020s boom.

Meanwhile, the Midwest and select core urban markets continue to outperform. Limited new supply and stronger affordability support demand in these markets. New York, Chicago, and Kansas City all posted double-digit rent gains since January 2023. However, the recovery still looks uneven. Yardi Matrix expects rent growth to stay weak into 2027. Then, growth could recover to 2.3%–3.5% by 2028 and beyond. Until then, weak absorption and concessions will pressure NOI growth and underwriting. Therefore, investors must reset expectations around rent growth and lease-up timelines.

On the capital side, transaction activity has slowed. Sales volume fell 10.7% year-over-year to $26.6B through May 2026. Sellers remain reluctant to meet buyer pricing that reflects today’s debt costs. That gap continues to delay broader liquidity. Still, lender activity remains strong, led by the GSEs. Fannie Mae originated $17.1B in Q1 2026, mostly through refinancings. Freddie Mac originated $13B during the same period. However, most originations now support existing borrowers rather than new acquisitions.

What’s Next

Through late 2026 and beyond, absorption will drive rent stabilization. The national pipeline still includes nearly 1.8M units. Oversupplied metros will feel the most pressure. Matrix expects national rent growth to rebound modestly to 1.0% in 2027. Then, growth could normalize between 2.3% and 3.5% by decade-end. In the meantime, high-supply Sun Belt markets will likely lag. Most metros may return to positive rent growth only by 2028 or 2029.

Investors and operators should expect continued concessions and longer lease-up periods. They should also prioritize operational efficiency and targeted value-add strategies over broad rent growth plays. Regional performance gaps will likely persist. Investors may keep favoring less-volatile, supply-constrained markets until the national supply overhang fades.