- Manhattan’s office availability fell to 13.0% in Q2 2026, its lowest level since October 2020, according to Colliers.

- Office conversions, distressed buildings, and less accessible properties reduce the pool of viable space far below headline availability figures.

- Strong leasing demand is shifting negotiating leverage back to landlords, especially for newer, amenity-rich buildings.

Manhattan’s office market continues to tighten, but the headline availability rate only tells part of the story.

Colliers reported a 13.0% availability rate in Q2 2026, down sharply from the market’s 18.2% peak in February 2024 and the lowest reading since October 2020. Even so, many tenants searching for high-quality space face far fewer options than the overall numbers suggest. As premium inventory becomes scarcer, landlords are gaining leverage in many of Manhattan’s strongest office corridors.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Competitive Space Keeps Shrinking

The Manhattan office market still has 68.1M SF of available space, but much of that inventory sits outside the preferences of today’s occupiers. According to Colliers, roughly 2.41M SF belongs to buildings under consideration for residential conversion, where leasing activity often slows as owners weigh redevelopment options. Another 3.96M SF sits in properties under special servicing, creating longer approval processes and less leasing flexibility.

Location also continues to separate winners from laggards. Buildings located more than a 10-minute walk from a subway station account for another 3.5M SF of available inventory and post a 31.2% availability rate, more than double the Manhattan average. Removing these categories reduces effective availability to 58.23M SF, or about 11.1%, much closer to a balanced market.

The Details

Demand has accelerated at the same time effective supply has contracted. Manhattan recorded 22.8M SF of leasing volume during the first half of 2026, its strongest first half since 2002, according to Colliers. If activity continues at the same pace through year-end, 2026 would produce the market’s strongest annual leasing total since 2000.

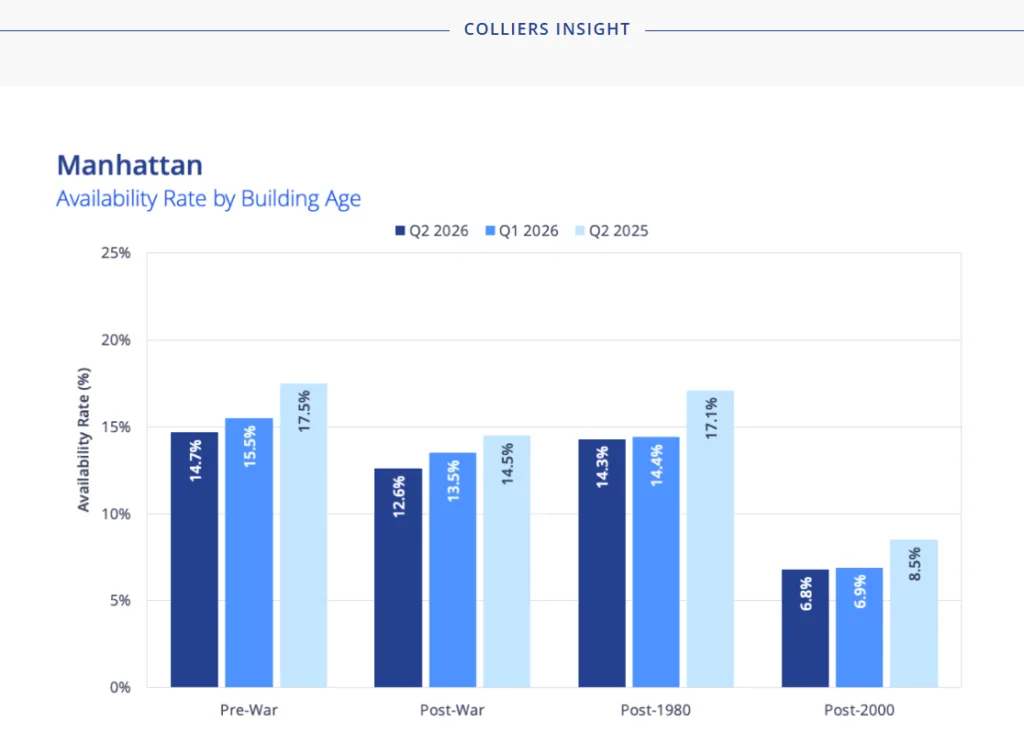

The recovery remains highly uneven across building types. Post-2000 office buildings reported just a 6.8% availability rate, below their March 2020 level of 10.1%. Older inventory continues to carry much higher availability, including 14.7% for pre-war buildings, 12.6% for post-war assets, and 14.3% for buildings constructed after 1980. That imbalance has fueled intense competition for the newest office product, with some tenants entering bidding contests for limited space.

Premium Buildings Pull Ahead

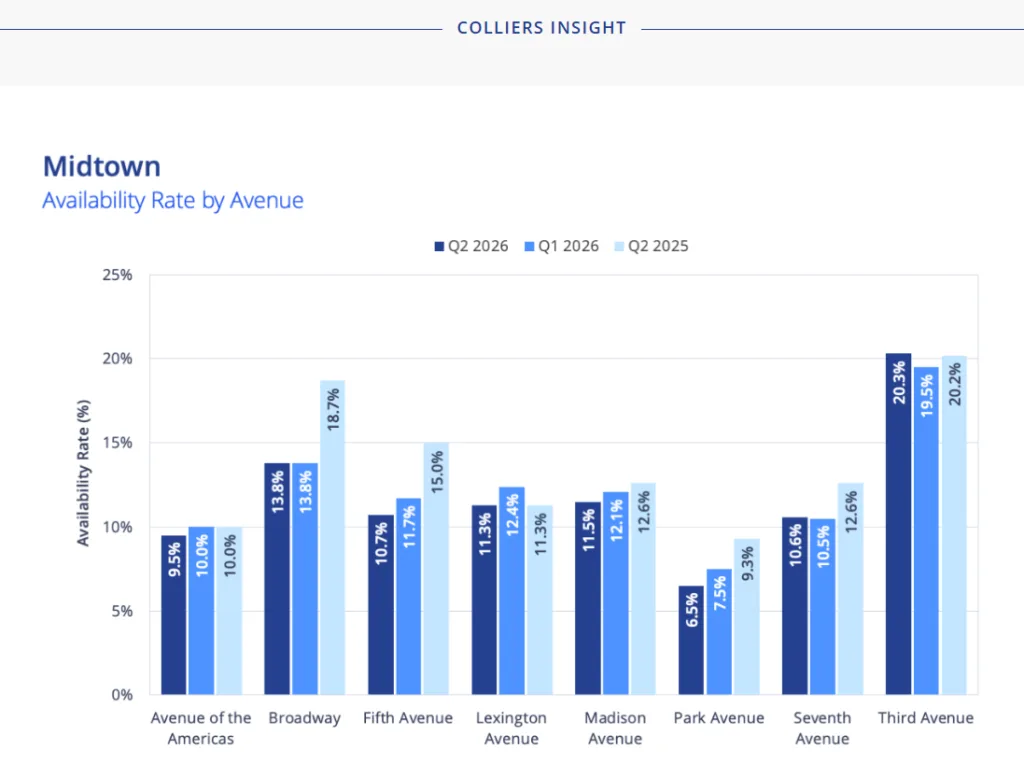

The divide extends beyond building age. Midtown’s Park Avenue corridor reported a 6.5% availability rate, compared with 11.5% along Madison Avenue and 20.3% on Third Avenue, illustrating how location continues to shape tenant demand.

At the same time, a sizable portion of available inventory has remained on the market for years. Nearly 19.72M SF, or 29% of available space, has sat vacant for more than three years. More than 10.44M SF has remained available for over five years. Before the pandemic, those shares were substantially lower despite similar leasing activity. Many tenants simply bypass these properties in favor of newer, amenitized buildings.

Why It Matters

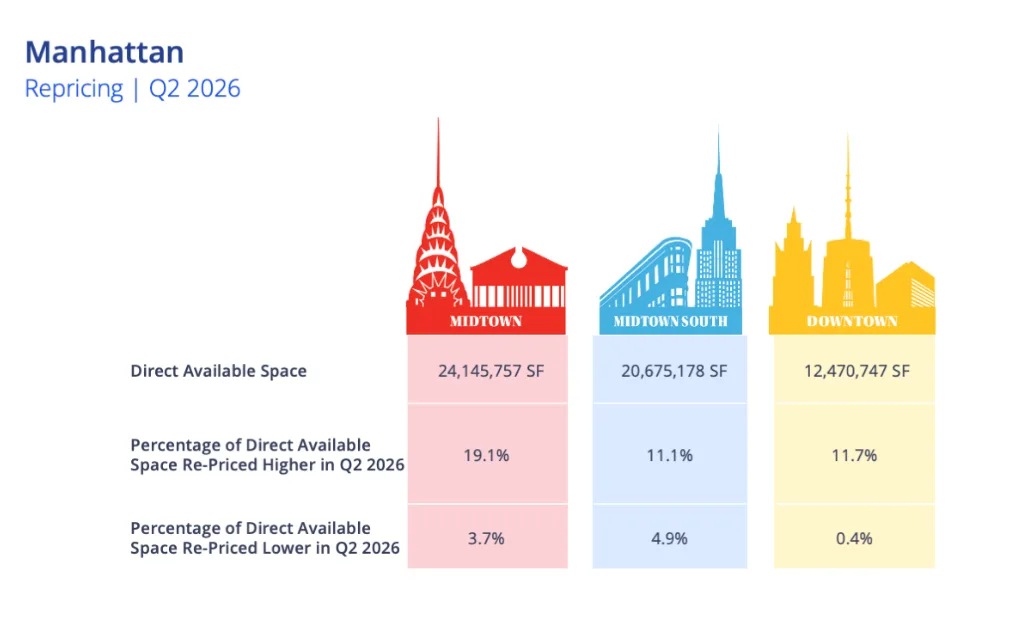

The market’s tightening conditions are beginning to restore landlord pricing power. Colliers found that landlords increased asking rents on far more listings than they reduced during Q2 2026, particularly in Midtown. Free rent packages have also declined, with average rental abatements falling to 12.4 months during the first half of 2026, the lowest level since 2019.

Tenant improvement allowances have stabilized near $140.02 PSF, although rising construction costs continue to pressure landlords. Together, those trends suggest owners no longer need to rely on aggressive concession packages to attract tenants in the market’s most competitive buildings.

What’s Next

Manhattan still carries more available office space than it did before the pandemic, leaving value-oriented tenants with meaningful options. Premium office users, however, face a much tighter market than the headline availability rate implies.

Future leasing momentum, additional office-to-residential conversions, and continued reductions in sublease inventory could tighten effective supply even further. If demand remains near current levels, competition for modern, well-located office space is likely to intensify, giving landlords additional pricing leverage across Manhattan’s highest-performing assets.