- The K-shaped economy is steering capital into asset classes serving high-income tenants and investors, per Bisnow and MetLife Investment Management.

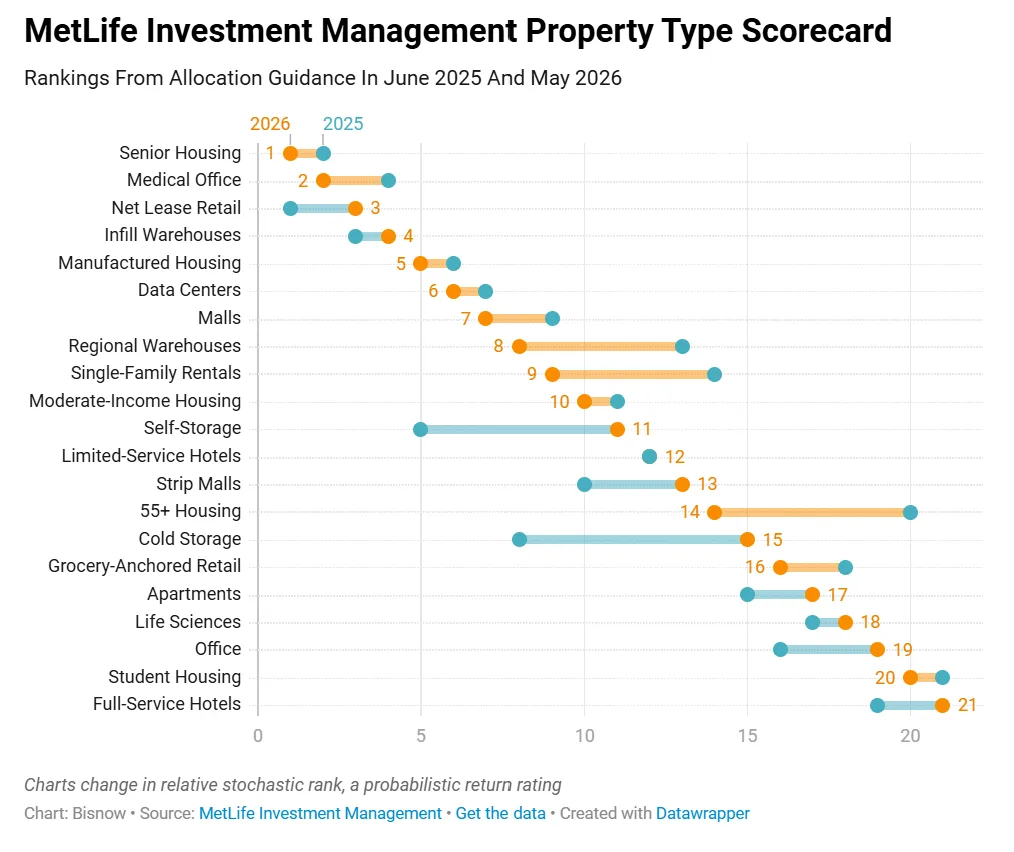

- Senior housing and net lease retail rose in MetLife’s asset rankings, while cold storage saw a sharp drop amid rising supply and vacancy.

- Institutional investors are targeting consolidation plays in asset types once dominated by individuals, like net lease retail and single-family rentals.

Class Divide Shapes Investment Focus

Bisnow reports that surging oil prices and a deepening economic divide are leading investors to rethink their real estate allocations. The so-called K-shaped economy—marked by high earners driving spending and growth while lower-income households pull back—has intensified since oil jumped on the back of the recent conflict with Iran. William Pattison, MetLife Investment Management’s head of research and strategy for real estate, told Bisnow that the asset split matters more than property type as investors hunt for resilience in a volatile environment shaped by inflation and bifurcated demand.

MetLife’s May 2026 US Chartbook highlights how investment strategies are adapting. Despite strong short-term sector returns for assets like lodging, investors are favoring niches that stand to benefit from demographic shifts and persistent demand from affluent renters and consumers. The latest ranking shuffle illustrates how a K-shaped recovery is influencing both asset allocation and private capital placements.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Asset Rankings Reflect Shifting Priorities

In response to shifting fundamentals, MetLife Investment Management—overseeing $736B in assets, including $106B of real estate—recently updated its allocation scorecard. Senior housing claimed the top spot, up from second place last year. That’s a result of baby boomers aging into the 75-plus bracket, finally unlocking pent-up demand after two soft decades. Pattison noted surging rents above $10K per month in states like Texas and Florida, even as overall US costs remain moderate.

Net lease retail, a favorite for consolidation and institutional capital, remains among the highest-rated asset types despite an M&A-driven shakeup in public REITs. Meanwhile, cold storage tumbled seven spots to No. 15. According to Newmark, speculative development during the pandemic added nearly 300 new cold storage operators from 2020–2025, leading to a 20-year high in vacancy. Industrial assets overall stayed strong but gave up one ranking position, now sitting in third, just below net lease retail.

Asset Quality, Not Just Type, Sets the Pace

Pattison emphasized that the real story is within the asset classes themselves. Nowhere is the split clearer than in lodging: his team parsed the sector into nine quality tiers and found a striking pattern—luxury hotels are outpacing their economy counterparts, with the latter seeing revenue per available room slide by around 5%.

Despite beating last year’s performance on the public market, lodging sits in the lower half of MetLife’s risk-weighted ranking, as near-term success isn’t enough to outweigh longer-term uncertainty tied to economic stratification. A similar divide has emerged in grocery-anchored centers, where necessity spending remains resilient despite softer consumer activity elsewhere.

Industrial—especially cold storage—highlights how rapid demand during the pandemic can give way to oversupply. The cold storage boom drove exceptional returns from 2020 to early 2025, but aggressive development has now caught up, softening the sector’s performance as vacancies rise.

Why It Matters

The K-shaped economy is changing the game for CRE strategy, as investors pivot from broad property types to nuanced bets on class and end-user demand. Affluent consumers and aging boomers are exerting outsize influence: witness senior housing moving into the top slot in MetLife’s 2026 rankings, driven by renters with the means to spend $10K or more per month. This accelerates a years-long demographic transformation that was delayed by the small Silent Generation—now baby boomers are entering the market in force, per MetLife’s May chartbook.

Meanwhile, surging oil prices—spurred by the Iran conflict—are feeding inflation and further splitting spending patterns, as high-income households drive growth and everyone else pulls back. This bifurcation is showing up in everything from hotel performance to retail and industrial demand. Net lease retail, often owned by high-net-worth individuals but now facing a wave of institutional interest, exemplifies the shift toward asset classes that offer stability and strong potential for consolidation. As technology facilitates access to formerly niche sectors like self-storage and single-family rentals, analysts expect more institutional capital to flow into net lease retail.

Cold storage’s reversal is a warning: rapid sector momentum can quickly reverse when aggressive construction overtakes demand, a dynamic many pandemic-darling asset classes could face as the economic split persists.

What’s Next

As the effects of surging oil prices and the K-shaped recovery play out, expect more investors to prioritize asset quality and demographic-driven demand over property type. MetLife predicts ongoing consolidation in net lease retail and increased institutionalization of mature sectors—especially as capital seeks resilience amid uncertainty. Industrial demand will likely remain solid for well-located assets, but sectors burdened by oversupply, like cold storage, may see further reset as vacancies adjust toward historic averages. The scorecard approach favored by MetLife and its $736B portfolio could become a model for capital allocation in a market defined by divergence, not convergence.