- The Federal Reserve relies on estimated benchmarks like the neutral interest rate and potential economic growth to determine whether policy is restrictive or supportive.

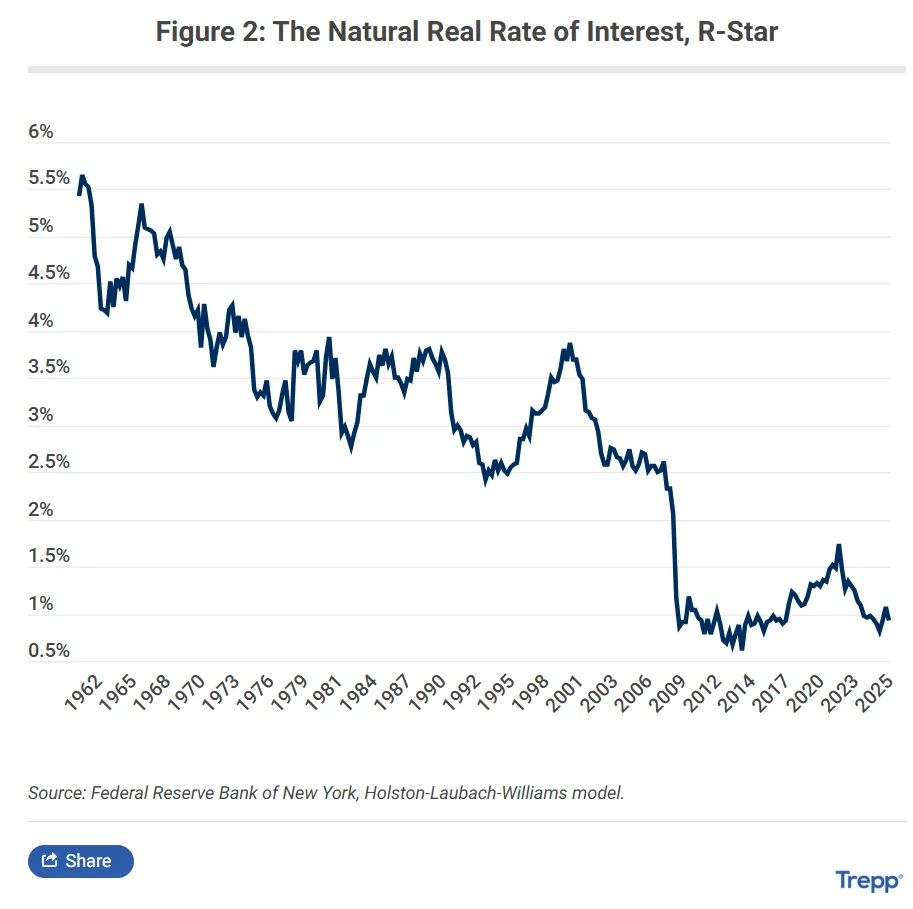

- A higher estimate of the neutral rate, known as r*, could keep Treasury yields and CRE borrowing costs elevated even if the Fed cuts rates later this year.

- CRE owners face a growing disconnect where strong economic growth supports leasing fundamentals while simultaneously delaying rate relief and refinancing recovery.

Commercial real estate investors are watching inflation prints, Treasury yields, and Fed meetings closely, but the most important drivers of monetary policy may be the benchmarks nobody can directly observe.

A May 2026 Trepp analysis explored how the Federal Reserve uses estimated economic “star” variables — including r* (the neutral real interest rate) and potential GDP growth — to determine whether monetary policy is restrictive, neutral, or accommodative. Those assumptions increasingly matter for CRE because they shape rate expectations, credit spreads, refinancing conditions, and valuation models.

Fed officials may be looking at the same economic data as lenders and borrowers, but their interpretation depends on where they believe the economy’s sustainable “speed limit” and long-run interest-rate equilibrium sit.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Framework Investors Rarely See

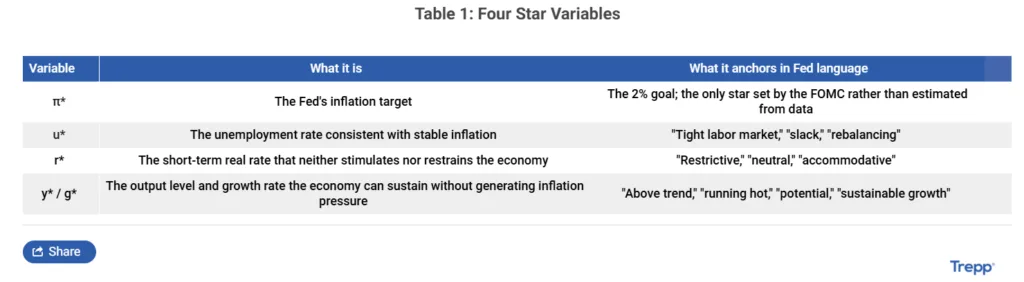

The Fed regularly describes the economy using phrases like “above trend growth,” “restrictive policy,” and “labor-market rebalancing.” Behind those terms are benchmark estimates rather than fixed data points.

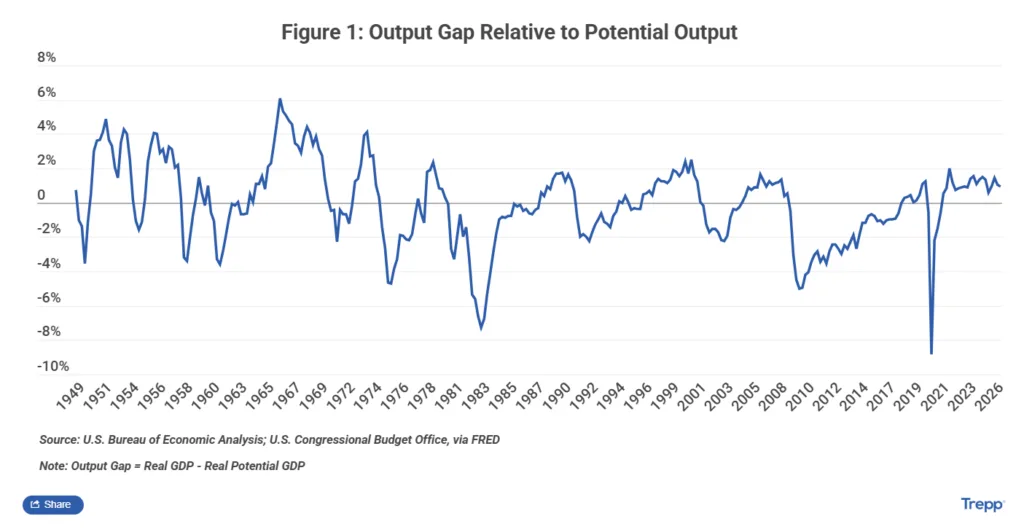

Potential growth — often referred to as y* — represents the economy’s sustainable growth rate without generating inflation pressure. Meanwhile, r* represents the neutral real interest rate where policy neither stimulates nor restrains growth.

Those benchmarks directly influence how the Fed interprets GDP growth, inflation, and labor-market data. A 3% GDP growth rate may appear inflationary if policymakers estimate potential growth near 2%, but look sustainable if they believe productivity gains or labor-force expansion lifted the economy’s capacity.

That distinction matters for CRE because stronger economic growth can improve occupancy, rents, and leasing demand while simultaneously pushing Treasury yields higher if the Fed believes the economy is overheating.

The Financing Connection

Trepp noted that policy rates alone do not determine how restrictive monetary conditions are. The Fed’s stance depends on where policymakers believe neutral rates sit relative to current interest rates.

That dynamic is becoming increasingly important for commercial real estate financing. If policymakers conclude that r* has permanently moved higher following the pandemic, the long-run destination for rates may also settle above pre-2020 norms.

Borrowers that underwrote deals during the low-rate era could face a much different refinancing environment even if the Fed eventually resumes easing.

That pressure is already visible across CRE lending markets. According to NAIOP’s Q1 2026 Debt Market Survey, falling SOFR lowered floating-rate borrowing costs. Meanwhile, rising Treasury yields kept fixed-rate financing elevated. At the same time, AI-driven leasing demand continues supporting office fundamentals in select gateway markets.

At the same time, the 10-year Treasury yield climbed toward 4.6% in mid-May as investors reassessed inflation risks, energy prices, and the Fed’s policy outlook.

The AI Productivity Debate

One major wildcard shaping the Fed’s thinking is artificial intelligence.

Trepp highlighted how policymakers are increasingly debating whether AI-driven productivity gains could raise the economy’s long-run growth potential. If productivity accelerates meaningfully, the economy may be able to grow faster without reigniting inflation.

But stronger productivity could also push the neutral rate higher by increasing investment demand and economic capacity. That would imply structurally higher long-term rates even if inflation stabilizes near the Fed’s 2% target.

Several CRE market participants are already linking AI investment to broader economic resilience. Northmarq’s March 2026 Build-to-Rent Report said recent GDP expansion was partly supported by “business investment in artificial intelligence and the capital investment required to build out the infrastructure that will fuel it.”

Why It Matters

For commercial real estate, the Fed’s benchmark assumptions increasingly matter as much as the economic data itself.

A stronger-than-expected GDP report can improve property fundamentals while also delaying rate cuts and increasing refinancing pressure. Likewise, slowing labor markets may support eventual easing but weaken tenant demand and leasing activity.

That balancing act is already shaping investment strategy across sectors. Northmarq’s March 2026 report noted that many developers are using bridge financing in anticipation of lower permanent financing rates later this year, while lenders remain cautious about inflation and elevated Treasury yields.

The result is a CRE market where financing assumptions increasingly depend on how the Fed interprets the economy’s underlying capacity rather than any single inflation or employment report.

What’s Next

Investors will likely watch the Fed’s long-run projections more closely in upcoming SEP releases. They will focus on neutral rates and long-term GDP growth estimates.

Kevin Warsh became Fed chair in May 2026. Since then, investors have closely tracked how policymakers view inflation, productivity, and labor markets.

CRE owners and lenders now face a different question. They no longer ask when rate cuts will begin. Instead, they ask where rates will settle after this cycle ends.