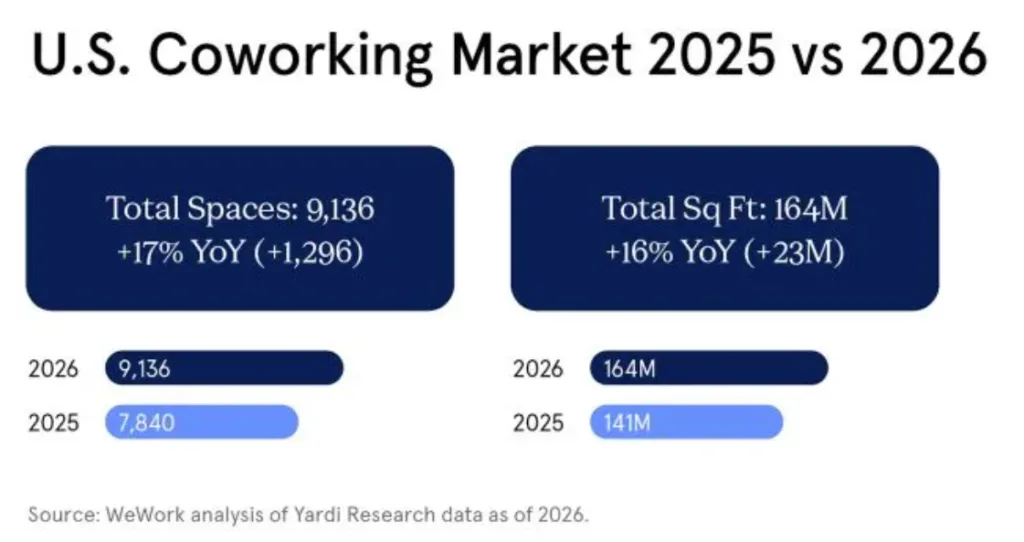

- The US coworking market grew 17% year over year to 9,136 locations, with growth concentrated in the country’s top startup ecosystems, according to WeWork, Yardi Research, and StartupBlink.

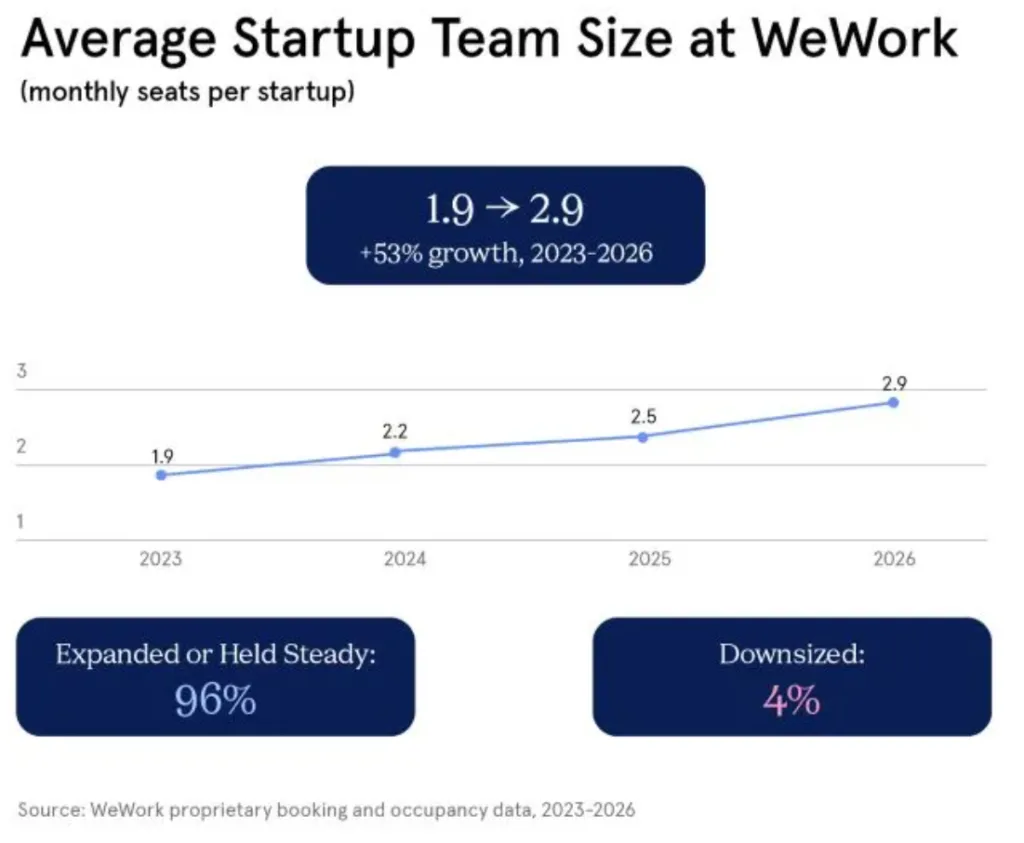

- Startup users are scaling inside flexible office portfolios, with 96% of active startups maintaining or expanding their footprint and average team sizes increasing more than 50% since 2023.

- Markets with strong AI, biotech, fintech, and defense-tech ecosystems are increasingly treating coworking as core business infrastructure rather than temporary office space.

Flexible workspace is becoming a growth engine for startup-heavy office markets. A new WeWork-backed analysis of the top 20 US startup metros found coworking demand rising fastest in the same cities attracting venture capital, AI hiring, and emerging tech companies.

The report combined StartupBlink’s 2025 Global Startup Ecosystem Index with Yardi Research coworking data and internal occupancy metrics from WeWork’s 146 US locations. The findings point to a broader shift in office demand: startups are not only using flexible space more frequently, they are also expanding within those portfolios instead of graduating into traditional leases.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Startup Metros Drive Coworking Demand

The US coworking market added nearly 1,300 locations over the past year, reaching 9,136 nationwide, while total coworking inventory climbed to 164M SF, according to Yardi Research and WeWork data. The top startup metros identified in the report were San Francisco, New York, Los Angeles, Boston, Seattle, Austin, Chicago, Washington, DC, Philadelphia, and San Diego.

New York remains the country’s largest coworking market with 753 locations and nearly 20M SF of flex office inventory. San Francisco, meanwhile, continues to dominate startup activity globally and saw coworking inventory expand to more than 5M SF. Philadelphia posted the fastest coworking growth rate among the top 10 startup metros, adding 43 locations for a 28% annual increase.

The Details

WeWork said more than 42,000 startups and SMBs joined its US locations between 2023 and April 2026, with more than 9,000 still active today. Among those active members, 96% either maintained or expanded their office footprint, while average team size increased by more than half during the same period.

Several markets posted especially sharp growth metrics. Chicago startups using WeWork expanded team sizes by 77% on average, the highest among the top 10 metros. San Diego recorded a 33-percentage-point jump in occupancy, while Denver posted 111% team growth among active users. Roughly one in 12 startups now operates from multiple WeWork locations, signaling that flex office networks are increasingly supporting multi-market expansion.

The report also highlighted how sector specialization is shaping office demand. San Francisco continues to benefit from AI-related growth, New York remains heavily tied to fintech, Boston’s ecosystem centers on biotech and life sciences, while Washington, DC, leans heavily into govtech and cybersecurity.

Flexible Office Becomes Startup Infrastructure

The latest numbers reinforce how flex office operators are repositioning themselves after years of volatility. Coworking was once viewed primarily as overflow space for freelancers or early-stage companies. But the newest data suggests startups increasingly see flexible office as a long-term operating model.

That shift comes as many venture-backed companies remain cautious about committing to large, long-duration leases. Flexible space offers shorter commitments, built-out offices, and geographic scalability at a time when hiring patterns remain uneven and workplace strategies continue evolving.

The report’s findings also align with broader office leasing trends. JLL’s May 2026 Global Real Estate Perspective found tenants favoring newer buildings and flexible layouts. That trend is also reshaping demand patterns across major US office markets.

Why It Matters

The data offers another signal that startup ecosystems are becoming increasingly concentrated around cities with strong talent pipelines, venture funding, and specialized industries. Those same markets are now producing some of the healthiest flex office demand in the country.

For landlords, that could reshape how office product is leased and operated. Larger coworking operators increasingly function as enterprise-style office providers rather than short-term desk rentals. WeWork noted its portfolio represents just 2% of US coworking locations but more than 5% of total coworking SF, reflecting a focus on larger-format space designed to accommodate growing teams.

The trend could also help stabilize select urban office markets that continue battling elevated vacancy. Startup demand may not fully offset downsizing by large corporate tenants, but expanding small-team users are becoming a more meaningful source of absorption.

What’s Next

AI, biotech, fintech, and defense-tech growth will likely continue steering flexible office demand toward established innovation hubs over the next several years. Markets like Austin, Denver, and Philadelphia could also gain additional momentum as startups seek lower-cost alternatives to coastal gateway cities.

At the same time, coworking operators appear increasingly focused on portfolio optimization rather than rapid expansion. Some metros, including Salt Lake City, saw coworking SF contract even as startup users inside existing locations expanded rapidly, signaling a shift toward higher-performing assets and more efficient space utilization.

The bigger question for office landlords is whether flexible workspace evolves from a niche amenity into a permanent layer of urban office infrastructure. Based on the latest startup growth patterns, that transition is already underway.