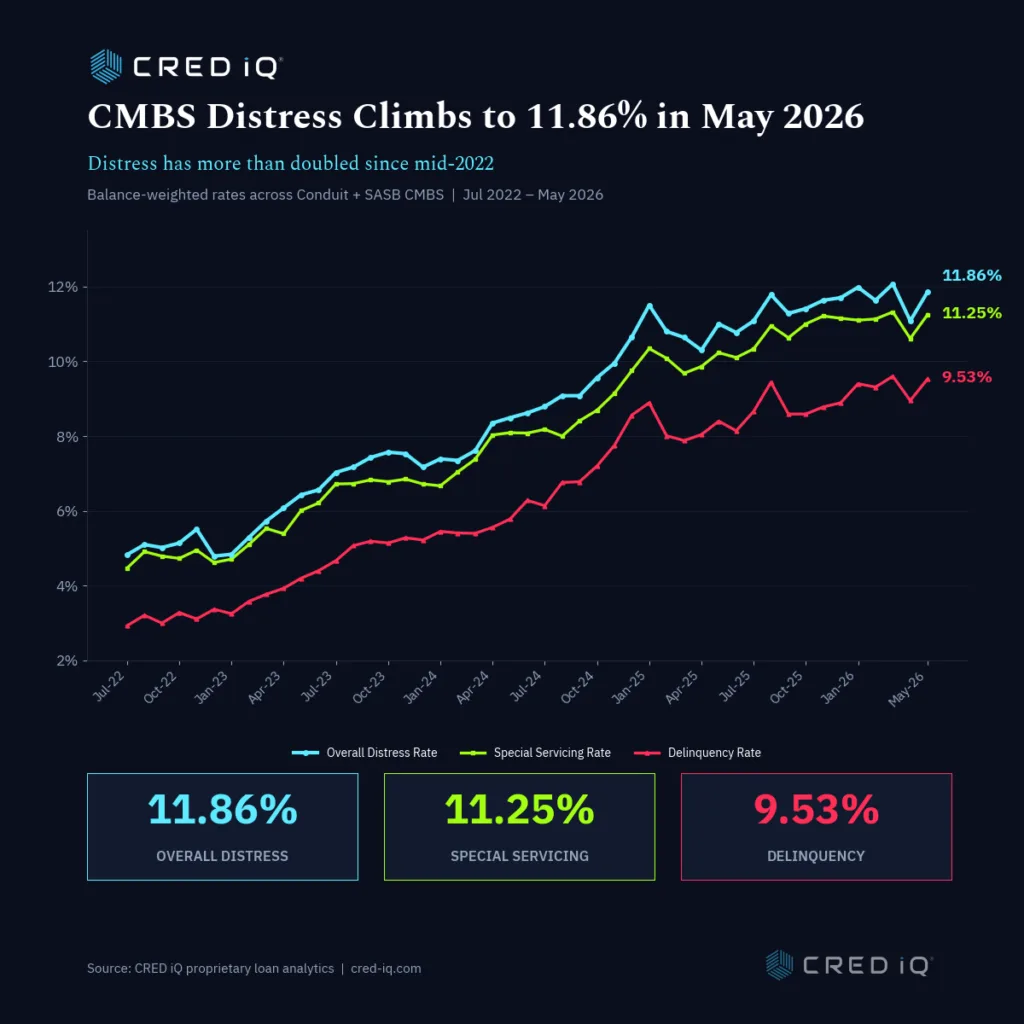

- The overall CMBS distress rate hit 11.86% in May 2026, up from April’s 11.08%, according to CRED iQ.

- Office properties posted a 17.11% distress rate, with mixed-use and lodging segments also exceeding the average.

- Persistent distress signals continued headwinds for investors and lenders as loan resolutions lag new transfers.

Distress Extends Rebound From April Dip

CRED iQ reported that the overall CMBS distress rate increased to 11.86% in May 2026, reversing April’s minor improvement and pushing the market closer to cycle-highs. This marks a full percentage-point shift higher in less than half a year, erasing hopes that distress might plateau after prior turbulence. For industry participants, the move underscores an ongoing imbalance: new distress continues to outpace loan resolutions, threatening underwriting assumptions even as maturities loom.

Since mid-2022, when the metric sat near 5%, the distress rate has more than doubled. According to CRED iQ’s methodology—which combines loans that are either delinquent or in special servicing—headline numbers actually understate emerging risks, since special servicers often become involved before payments are officially missed.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

May’s increase was broad-based across key metrics tracked by CRED iQ: the overall distress rate advanced by 78 basis points to 11.86%. The special servicing rate climbed 64 basis points to 11.25%, while delinquency rose 58 basis points to 9.53%. The roughly 170-basis-point spread between special servicing and delinquency rates highlights active but unresolved loan workouts—the distressed balance is shifting, not shrinking. By CRED iQ’s measure, these readings cover both Conduit and SASB deals and are weighted by loan balance for precision, offering a sharper view than simple loan counts would suggest.

Office and Mixed-Use Lead Distress Rankings

Office loans remain the main trouble spot, with a 17.11% distress rate in May, according to CRED iQ. Mixed-use follows at 16.12%, while lodging sits at 12.27%. Multifamily also reached double digits at 10.95%, as higher rates pressure floating-rate and bridge loans. That pressure follows April’s multifamily-led distress surge, which showed stress spreading beyond office earlier in the cycle.

Meanwhile, industrial, manufactured housing, and self storage remain mostly insulated. Industrial distress sits at 1.04%, manufactured housing at 1.19%, and self storage at just 0.15%. Persistent demand and steadier operating fundamentals continue to support those sectors.

These splits show a more divided market. Investors in stronger sectors can still find safety. Others face more turbulence as loan stress spreads.

Why It Matters

CMBS distress rates do more than reflect market sentiment. They shape liquidity, lender behavior, and deal flow across commercial real estate. April’s brief pause now looks short-lived. CRED iQ’s May increase pushed distress back near prior cycle peaks.

For brokers and institutional capital, conditions keep shifting in real time. Distressed loan balances are moving into special servicing before formal delinquency. That trend signals earlier intervention and likely negotiations before default occurs.

Office remains the clearest outlier. Its 17.11% distress rate reflects pandemic demand erosion and longer-term structural pressure. Together, those forces continue to weaken asset cash flows and values. CRED iQ’s loan-level data gives market participants sharper visibility. It tracks loans, servicers, and metros in detail. As a result, investors can benchmark exposures and spot risks earlier.

That granularity matters as the market cycles. Participants need to know which credits can work out. They also need to know which loans may transfer again. In some markets, future pricing may still need to capitulate.

For lenders, investors, and analysts, early visibility creates a real advantage. The sector faces another stress wave, with major maturity cliffs approaching in 2026 and 2027.

What’s Next

The CMBS market still faces major headwinds. Distress keeps rising across office, mixed-use, and hospitality. Therefore, mature and seasoned portfolios could see more special servicing transfers before relief arrives.

Resolution activity still trails new transfers. As a result, distress rates could stay elevated through the second half of 2026. They could also rise further as more loan maturities come due. For CRE stakeholders, granular performance data remains essential. Portfolio stress-testing also matters more in this cycle. The sector still needs to find a bottom before capital deployment can reset.