- Building material inflation is accelerating, with copper, lumber, diesel, and aluminum prices all rising sharply and increasing home construction costs across the US.

- Supply disruptions, tariffs, geopolitical conflict, and strong demand from sectors such as data centers and electric vehicles are driving higher input prices for builders and developers.

- Rising construction expenses are compounding housing affordability challenges and could slow residential development activity if cost pressures persist.

Building material inflation is becoming a major challenge for the housing market as prices for key inputs—including copper, lumber, diesel, and aluminum—rise simultaneously. The WSJ reports that the cost increases are pushing home construction costs higher and creating new hurdles for builders, developers, and homeowners planning renovation projects.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A New Cost Burden for Builders

While borrowing costs remain elevated, construction materials have emerged as another significant headwind. According to Freddie Mac, the average 30-year fixed mortgage rate reached 6.51% in the week ending May 28, 2026, its highest level since August 2025. At the same time, builders are navigating volatile pricing across multiple product categories, making it increasingly difficult to estimate project costs and set home prices.

The National Association of Home Builders reported that 70% of respondents in its April 2026 builder-confidence survey experienced difficulty pricing homes due to uncertainty surrounding material costs. Associated Builders and Contractors Chief Economist Anirban Basu said input prices have risen more during the first four months of 2026 than during the previous three years combined.

The Details

Several market forces are converging to drive costs higher.

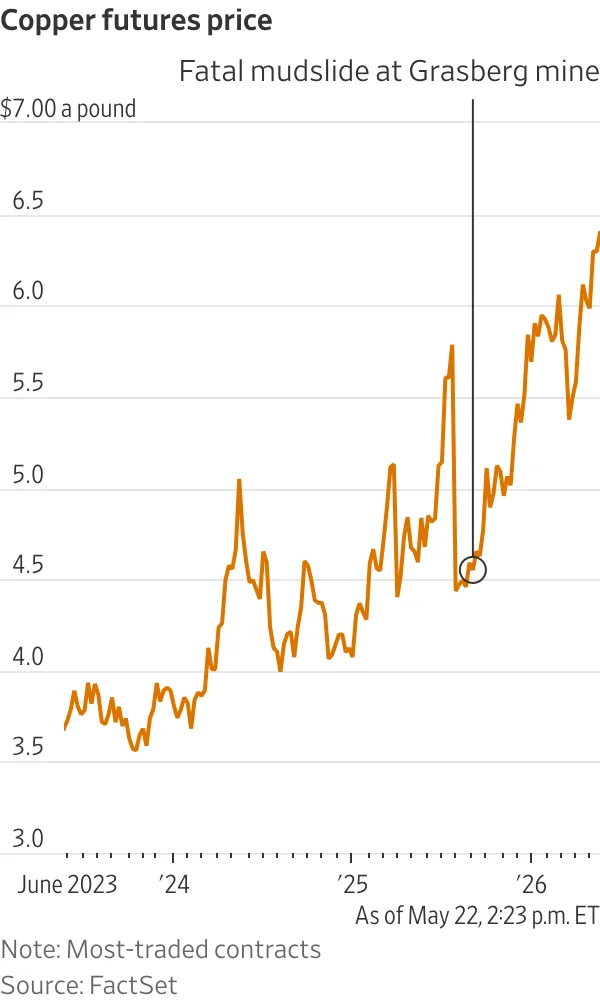

Copper prices have climbed to record levels as supply disruptions hit the global market. According to Freeport-McMoRan, production at its Grasberg mine in Indonesia—the world’s second-largest copper mine—will recover more slowly than previously expected following operational challenges tied to a 2025 mudslide. At the same time, growing demand from data centers and electric vehicle manufacturers continues to increase competition for the metal.

The impact on housing is significant. A typical US home contains more than 400 pounds of copper across electrical systems, plumbing, appliances, and fixtures.

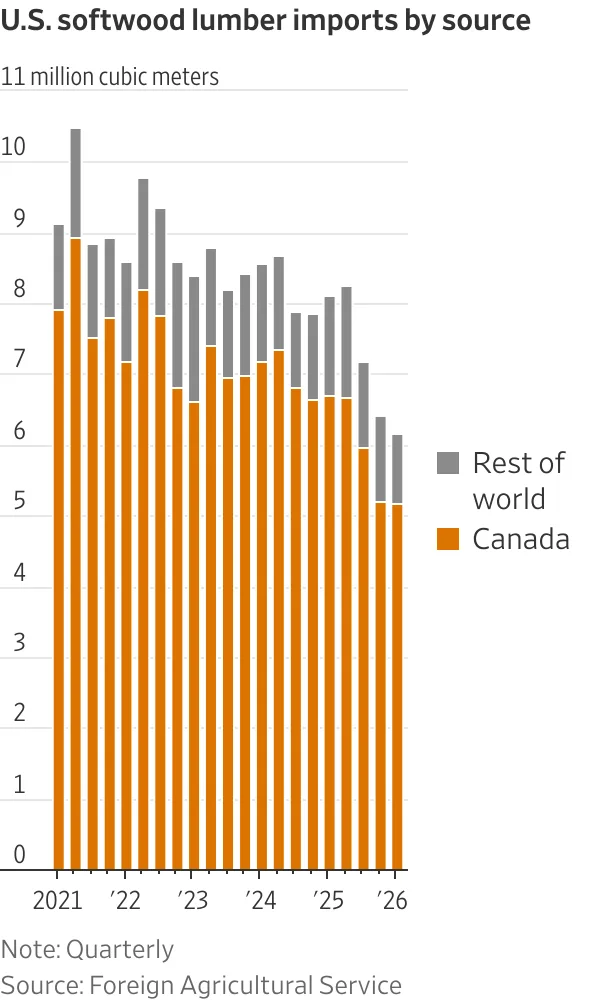

Lumber prices are also moving higher. Random Lengths’ Framing Lumber Composite Price has increased more than 30% from its December 2025 lows, according to the trade publication. Industry participants attribute the increase to Canadian sawmill closures, reduced production, and elevated import duties. Combined tariffs and trade-related duties have pushed effective taxes on many Canadian lumber imports to roughly 45%.

Fuel costs represent another growing challenge. The conflict involving Iran has disrupted energy and petrochemical markets, increasing diesel prices and raising transportation expenses for construction materials. Eagle Materials recently reported that higher fuel costs increased wallboard freight expenses by more than $2 per thousand SF during its fiscal fourth quarter and prompted cement price increases across many markets.

Meanwhile, aluminum prices remain near record highs on the London Metal Exchange. US buyers face additional pressure from a 50% tariff, increasing costs for products ranging from HVAC systems and ductwork to building facades and structural components.

Supply Shocks Meet Policy Pressures

Unlike previous construction inflation cycles driven primarily by demand, today’s pricing environment reflects a combination of supply constraints, geopolitical disruptions, and trade policy.

Copper markets are dealing with both mine disruptions and shortages of sulfuric acid, a key input in copper production. Those challenges are amplifying cost pressures already emerging from record copper prices and tightening global supply. Lumber markets face constrained supply and elevated import costs. Aluminum buyers are contending with both global price increases and tariff-related premiums. Diesel and petrochemical markets have been affected by conflict-driven supply concerns.

The result is broad-based inflation across the construction supply chain rather than isolated spikes in individual materials.

Why It Matters

For developers and builders, rising material costs create margin pressure at a time when buyers are already struggling with affordability. Higher construction expenses ultimately feed into home prices, making it harder for consumers to enter the market.

The broader CRE industry also faces implications. Residential developers may delay projects, reduce planned unit counts, or seek value-engineering opportunities if cost escalation continues. According to Associated Builders and Contractors, sustained input-cost growth could weigh on construction activity over the coming months.

Higher material prices also contribute to inflation concerns in financial markets, which can influence bond yields and borrowing costs for both residential and commercial projects.

What’s Next

Builders are watching several potential relief valves. Lumber buyers expect Canadian import duties to decline later in 2026, which could ease pricing pressure heading into future construction cycles. Market participants are also monitoring developments in global energy markets and production recovery at major copper operations.

For now, most signs point to continued volatility. As long as supply disruptions, tariffs, and geopolitical risks remain in play, building material inflation is likely to remain a central challenge for the housing sector—and another obstacle to improving affordability.