- Major US banks are quietly financing the rapid expansion of private credit in commercial real estate, mainly through back-leverage deals.

- Major US banks are quietly financing the rapid expansion of private credit in commercial real estate, mainly through back-leverage deals.

- Private credit loans to US nonfinancial corporations have nearly doubled since 2021, reaching $1.4T by late 2025, per Federal Reserve data.

- This evolving structure is blurring traditional lender-borrower roles and spreading risk—while making the true sources of CRE capital harder to track.

CRE’s Back-Channel Lending Evolution

Banks that once shunned or competed with private credit lenders are now providing the core financing that sustains the sector’s growth. Bisnow reports that despite regulatory pressure and pandemic-driven balance sheet woes, major institutions like Goldman Sachs, Bank of America, and JPMorgan Chase are supplying the back-leverage capital powering alternative lenders’ surge into CRE debt. By structuring this support at the fund or platform level rather than as direct property loans, banks are still in the game—just with less visibility and risk exposure.

According to the Federal Reserve, private credit entities nearly doubled their share of US nonfinancial corporate debt since 2021, holding $1.4T by mid-2025. Bank credit commitments to other financial entities hit $2.6T by the end of 2025, more than doubling since 2018. This marks a profound shift in how CRE deals are capitalized and who’s shouldering the risk.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

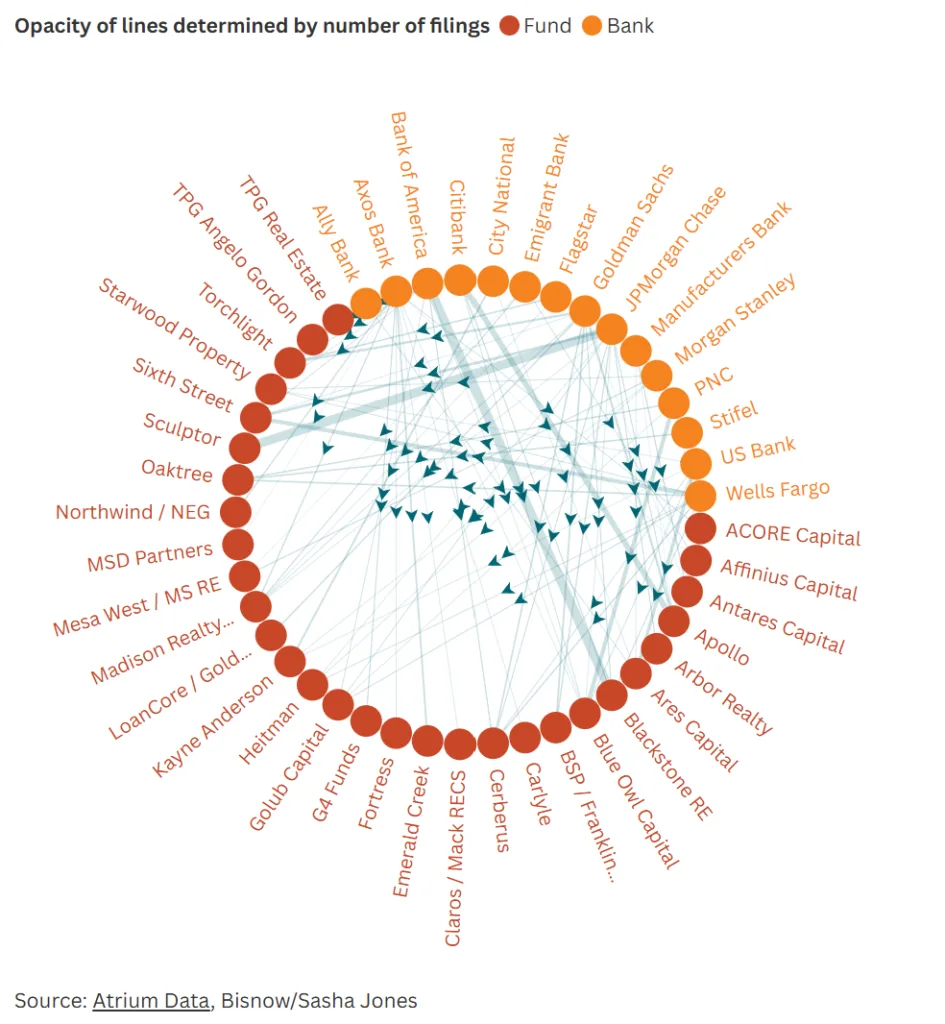

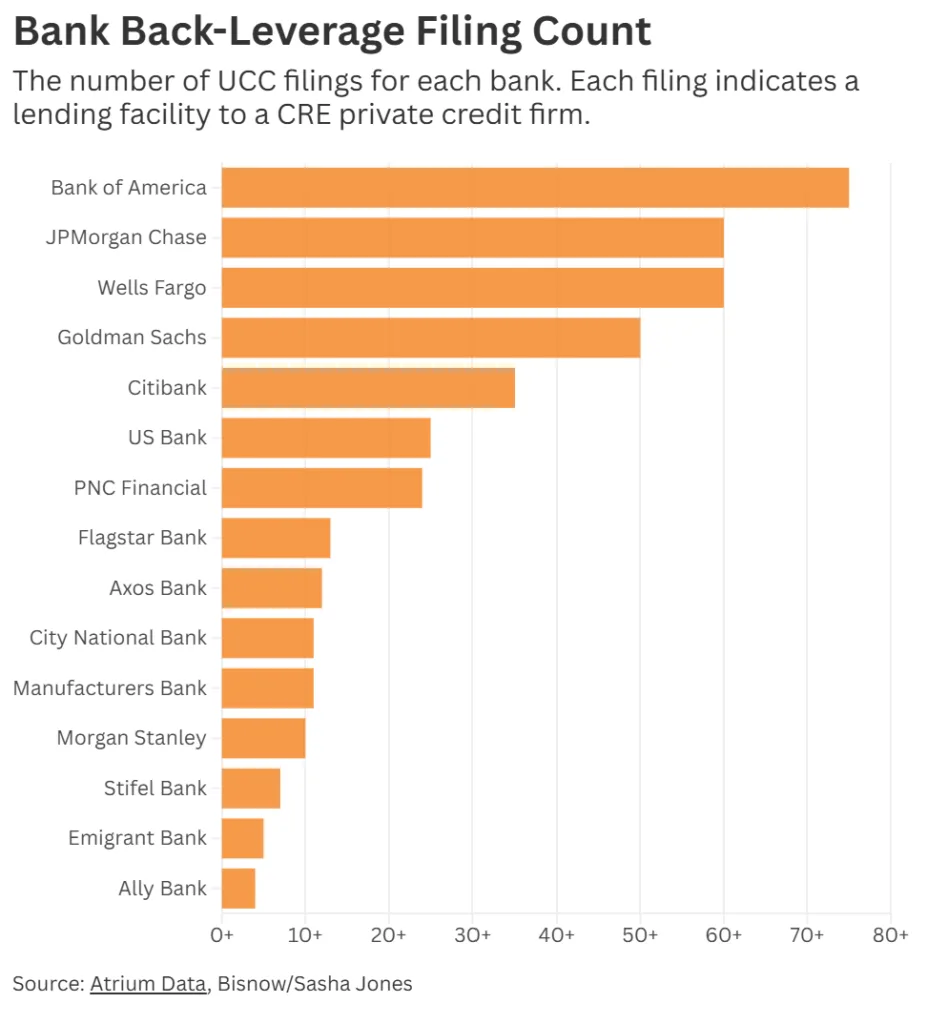

Atrium Data, an intelligence platform, tracked bank-private credit partnerships using Uniform Commercial Code filings, mostly in New York City, and mapped an opaque but intricate web. The five largest US banks account for the lion’s share.

Goldman Sachs had over 50 filings with nine different private credit operators. Bank of America’s commitments, the most by volume, are concentrated among TPG Real Estate and Blackstone. Of JPMorgan’s 60+ filings, most support Sculptor Capital Management’s funds. Citibank’s efforts are mainly funneled to Athene Global Funding, Apollo’s insurance subsidiary.

Smaller players like Stifel Bank (exclusive with Oaktree Direct Lending) and City National Bank (focused on Kayne Anderson) hint at specialized strategies, while digital-first Axos Financial stands out for its aggressive approach, backing at least 30 alternative asset managers ranging from the Carlyle Group and Blue Owl Capital to Madison Realty Capital. Relationship structures include warehouse lines, subscription facilities, and repurchase agreements, tailored to both risk appetite and regulatory requirements.

Basel III and CRE’s Invisible Capital Flows

Basel III capital rules are prompting banks to move CRE risk off their books by financing private credit lenders rather than offering direct loans. Instead, loans to these intermediaries are treated as commercial and industrial (C&I) loans, considered less risky. This reclassification allows banks to maintain real estate exposure with lower capital requirements. Recent regulatory changes have also expanded the menu of risk-transfer structures banks can use to manage CRE exposure more efficiently. Case Equity Partners’ Shlomo Chopp and others say these structures also allow lenders to magnify deal volume while limiting on-paper risk.

The dynamic is mutually beneficial. For private lenders, bank back-leverage expands lending firepower and lowers costs. For banks, it’s a way to stay active in CRE lending without breaching regulatory constraints. But this creates an increasingly complex web, where tracing risk to its true source is challenging even for seasoned market participants.

Why It Matters

Private credit’s ascent is fundamentally changing CRE financing. According to Federal Reserve data, private credit’s share of corporate debt nearly doubled in four years, reshaping the capital landscape. Banks’ shift toward back-leverage facilities has helped alternative lenders originate bigger and riskier loans—even as higher interest rates and thin equity have made deal-making harder for traditional players.

This dynamic blurs the distinction between banks and private lenders. Asset managers and insurers are no longer just borrowers—they are structuring, syndicating, and even taking the keys to CRE assets if things go south. This expansion of nonbank lending is dispersing risk widely—but also making the market harder to see or measure. As Fairbridge Asset Management’s Brian Walter notes, banks’ bar for direct CRE is higher than ever—but private lenders, with bank support, are filling the gap with more creative structures.

What’s less visible is that much of this risk ultimately sits with ordinary investors through pension funds or wealth management accounts, as Case Equity Partners’ Chopp notes. If private credit players get aggressive and the cycle turns, the systemic risk could extend far beyond the rarefied world of alternative finance. At the same time, bank back-leverage is keeping the capital flowing for now—potentially insulating the CRE system from shocks, but raising the stakes if cracks appear.

What’s Next

With Basel III implementation and persistently high rates, banks are unlikely to resume traditional CRE lending at scale. Instead, the pattern of financing private credit lenders—rather than making direct property loans—seems poised to persist and grow. Back-leverage is already lowering costs and boosting volumes across the private credit platform, as lenders like Acore Capital and Northwind Group diversify their facilities to access capital wherever possible.

Market participants expect even more innovation in risk-sharing structures, as both bank and nonbank players look to navigate regulation and market volatility. But this raises a question for the industry: As risk disperses and transparency wanes, will the market’s plumbing hold if defaults rise? For now, the money pipeline is open—just less visible than ever.