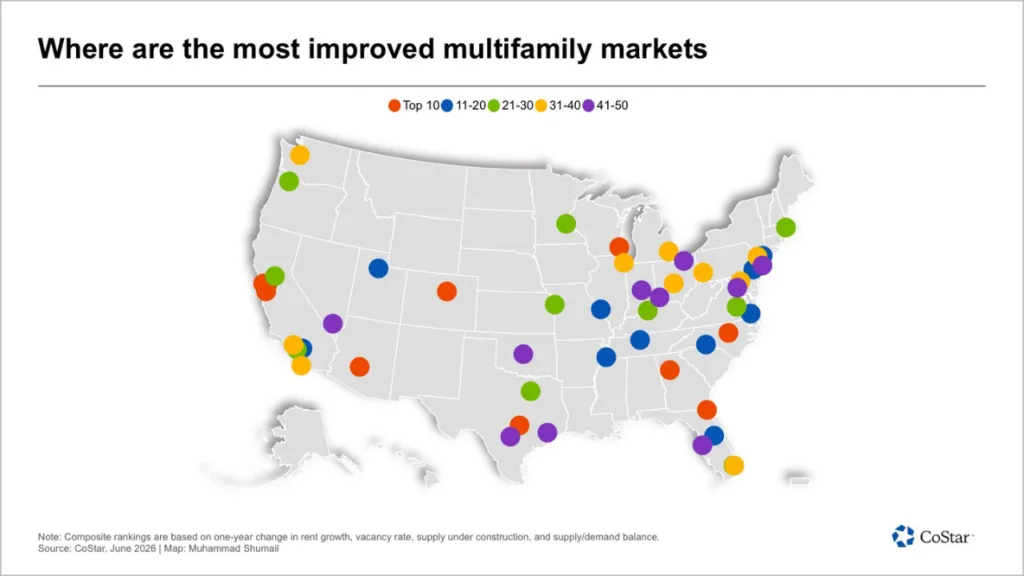

- Austin and San Jose lead Apartments.com and CoStar’s US multifamily market momentum index for year-over-year improvement as of Q2 2026.

- The index spotlights metros where rent declines are slowing, vacancies are tightening, and supply-demand fundamentals are stabilizing.

- Southern and California markets dominate the top 10, signaling a shift as supply pipeline resets and pricing power begins to return.

Localized Recoveries Redefine Momentum

Bussiness Wire reports that Apartments.com and CoStar’s newly refreshed multifamily momentum index spotlights metros where apartment fundamentals are improving fastest, per the report published in Arlington, Virginia. Rather than highlighting the “best” or priciest markets, the index captures which US cities are gaining ground on key metrics like rent growth, occupancy, new supply, and pipeline shifts. While the overall recovery since Q2 2025 remains uneven, the index reveals which local fundamentals are rebounding and why. Four of the top ten markets, including leader Austin, still report annual rent drops, but the pace is moderating, and vacancies are falling as new construction cools.

Market momentum matters as investors and operators seek early signs of where the tide is turning. The index draws on year-over-year improvements to signal which metros are moving from supply overhang toward stabilization, offering early insight into potential recovery cycles. This market-by-market approach helps distinguish genuine improvement from those still caught in a supply glut.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Austin leads the latest momentum index. San Jose, San Francisco, and the East Bay also rank highly. Jacksonville ranks third as occupancy improves and vacancy falls. CoStar says Austin rents remain below prior peaks. However, rent declines have started to slow. Lower construction activity lets demand catch up. San Jose shows a similar trend. Rent growth and vacancy metrics have rebounded from cyclical lows.

Jacksonville posted a roughly 170-basis-point vacancy decline over the past year. Yet rents remain slightly negative year over year. Top momentum markets often limit new supply. Others absorb units faster than expected. CoStar’s multifamily team says momentum varies by region. Each market sits at a different point in the supply-demand cycle.

South and Tech Hubs Lead Reset

The rankings highlight an ongoing trend. Sun Belt and tech-focused markets are regaining momentum after a choppy 2023 through 2025. Many faced oversupply and weaker demand during that period. The Bay Area, including San Jose, San Francisco, and the East Bay, continues to recover from pandemic-era declines. Local job growth also supports stronger fundamentals. Recent investment activity in a San Jose apartment tower suggests buyers are gaining confidence in the market’s recovery. Meanwhile, Jacksonville and other mid-sized Southern cities report occupancy gains as deliveries slow.

This divergence reshapes traditional growth markets. Austin and Jacksonville now improve through slower rent declines and stronger absorption. Meanwhile, supply-constrained markets rank lower on the momentum table. The shift creates new opportunities for multifamily investors and developers. Many remain cautious about excess supply in major metros.

Why It Matters

CoStar released the update as multifamily operators navigate a changing inventory landscape. Pandemic-era building booms and slower post-boom activity continue to shape conditions. The momentum index measures changes rather than absolute rent or vacancy levels. It highlights improving fundamentals instead of market peaks. Many top-10 cities still report negative annual rent growth. Still, falling vacancy and lower future supply suggest a potential turning point.

For investors, the rankings offer a different way to assess risk. They show where fundamentals improve, not just where conditions remain strongest. CoStar’s Grant Montgomery says stronger demand restores pricing power. He also notes that slower construction helps stabilize fundamentals while rents stay negative year over year. Jacksonville’s 170-basis-point vacancy decline reflects this trend. Austin’s slower rent declines and lower vacancy also point toward stabilization.

The momentum-based approach remains useful as national rent growth stays muted. New supply pipelines have also started to shrink. Operators can focus capital on metros where fundamentals may have bottomed. Pricing growth may still sit in its early stages. Market participants should watch these shifts as regional cycles continue to diverge.

What’s Next

Local supply discipline will likely determine which metros maintain momentum. Construction starts continue to slow in Austin, San Jose, and other leading markets. As a result, absorption should outpace supply. That trend could support firmer operating conditions. CoStar expects national averages to remain flat through 2027. However, select metros could post positive rent growth sooner. Strong job markets and limited supply would support that outcome. Improvement, rather than current strength, should remain the key differentiator in the next cycle.