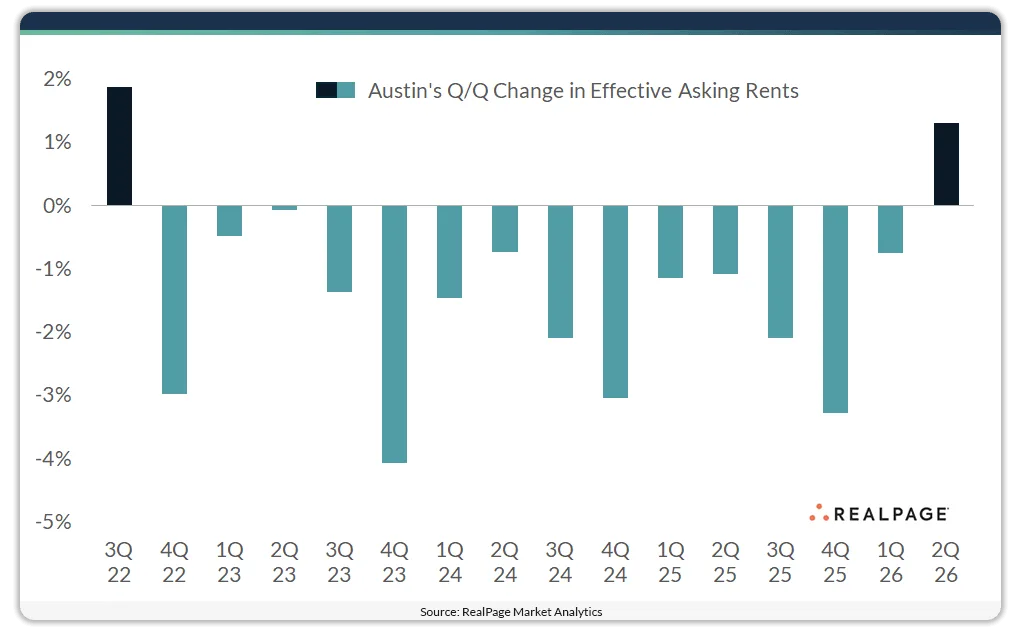

- Rents for Austin’s market-rate apartments climbed 1.3% in Q2 2026, the first quarterly gain since fall 2022.

- Nearly 97,000 units have delivered since 2020, making up almost 40% of Austin’s current inventory.

- Despite the uptick, average rents remain just $120 above 2019 figures, with Class C product still facing sharp declines.

Wave of Deliveries Redefined the Market

Austin’s reputation as the poster child for US apartment oversupply has been well earned. RealPage Analytics reports that since the start of 2020, nearly 97,000 new units have come online—representing close to 40% of all inventory in the metro.

That influx alone would make for a top 60 apartment market by size if it were a standalone city. The relentless new supply has put enormous pressure on operations, forcing rents down for years and challenging landlords’ ability to balance occupancy and pricing.

Get Smarter About What Matters in Texas

Subscribe to our free newsletter covering the biggest commercial real estate stories across Texas — delivered in just 5 minutes.

The Details

In Q2 2026, Austin’s market-rate apartment rents increased 1.3%, marking the first quarterly gain since fall 2022, per RealPage Analytics.

However, the recovery remains uneven across property classes. Class A properties posted a 0.8% year-over-year rent decline.

Meanwhile, Class B rents dropped 3.9%, while Class C rents plunged 11.6% from a year earlier.

The average effective rent now stands at $1,425 per month. That figure sits just $120 above the same point in 2019.

Even with this modest rebound, asking rents remain roughly $400 below their 2022 highs. The market continues digesting years of rent cuts.

Persistent Headwinds Despite a Turnaround

The surge in new construction continues to challenge property performance, particularly among older and mid-tier assets.

In recent years, Austin’s rent declines outpaced much of the nation. Excess deliveries severely affected both lease-up properties and stabilized assets.

Austin needs stronger absorption before property owners can expect consistent year-over-year rental growth.

For now, the positive quarterly movement offers cautious optimism. However, pockets of weakness persist, especially among Class C assets.

Why It Matters

The modest rent increase suggests Austin’s apartment sector could be moving beyond the worst of its supply-driven correction. However, recovery will take time. Austin’s experience reflects a broader pattern, as cities adding significant housing supply have faced slower rent growth.

According to RealPage Analytics, the metro’s inventory growth since 2020 rivals the entire multifamily stock in Hartford or Omaha.

That unprecedented expansion forced a harsh reset in property valuations and rent expectations.

Despite employment and population growth, the supply surge consistently outweighed demand. Owners responded with concessions and rent cuts to maintain stable occupancy.

Importantly, this rare Q2 rent increase marks an early step toward stabilization after several years of sizable annual declines.

However, current average rents of $1,425 per month remain only marginally above pre-pandemic levels.

Class B and C owners continue digging out from deep annual losses. Class C properties face particularly severe pressure from double-digit rent declines.

Lingering occupancy challenges also weigh on performance. As a result, the market’s underlying fundamentals remain far from robust.

Still, RealPage suggests the difficult effort to absorb Austin’s enormous supply wave may finally be approaching its end.

Operators and investors will closely watch the next few quarters for signs of sustained improvement.

What’s Next

With inventory growth finally cooling and demand slowly rebounding, Austin’s multifamily market could see steadier rent performance through late 2026.

RealPage Analytics suggests meaningful year-over-year rent growth will remain elusive until occupancy strengthens.

Multifamily stakeholders will closely track new lease absorption. They will also watch rental performance across lower-tier properties.

Improving rents or occupancy among Class B and C assets would provide the clearest evidence of broader stabilization.

Those gains could signal that Austin has finally reached supply-demand equilibrium. They could also mark the metro’s next rental cycle phase.