- AI firms now account for a growing share of active office requirements, with demand concentrated in a small group of major US markets.

- San Francisco, Silicon Valley, and New York dominate AI leasing, while secondary markets such as Seattle and Northern Virginia are gaining momentum.

- The trend suggests investors should evaluate office assets at the submarket level rather than relying on metro-wide vacancy averages.

AI office demand is accelerating, but the gains are far from evenly distributed.

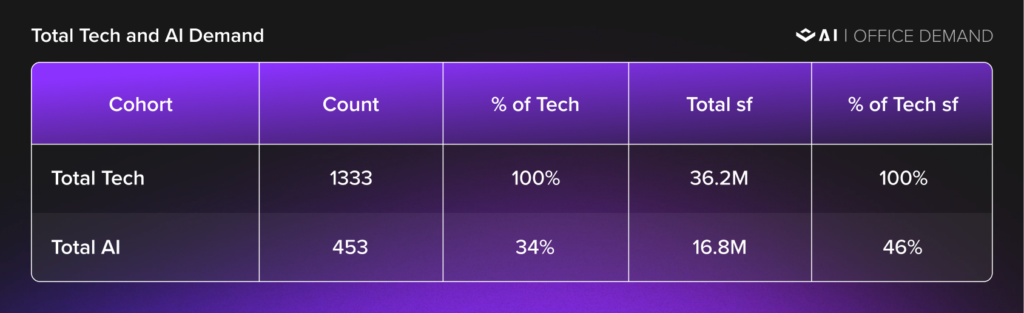

According to a report from VTS, AI-related office requirements climbed 85% year over year nationwide and 179% across the industry’s largest hubs. The data shows AI tenants now represent 34% of active tech leasing requirements tracked by VTS, totaling 16.8M SF. Instead of lifting entire office markets, that demand is concentrating in a handful of neighborhoods where competition for quality space continues to intensify.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

AI Capital Fuels Office Leasing

Office demand is following an unprecedented wave of AI investment. According to CB Insights, US private AI funding reached $206B during Q1 2026, nearly matching the full-year 2025 total of $217B. Global AI funding climbed to $226B during the quarter, the highest on record.

Source: VTS

Much of that capital flowed into a small number of companies. OpenAI alone raised $122B, while Anthropic and xAI secured another $37.5B combined. Those firms continue hiring highly specialized engineering talent, creating sustained office demand in markets where that workforce already exists.

The Details

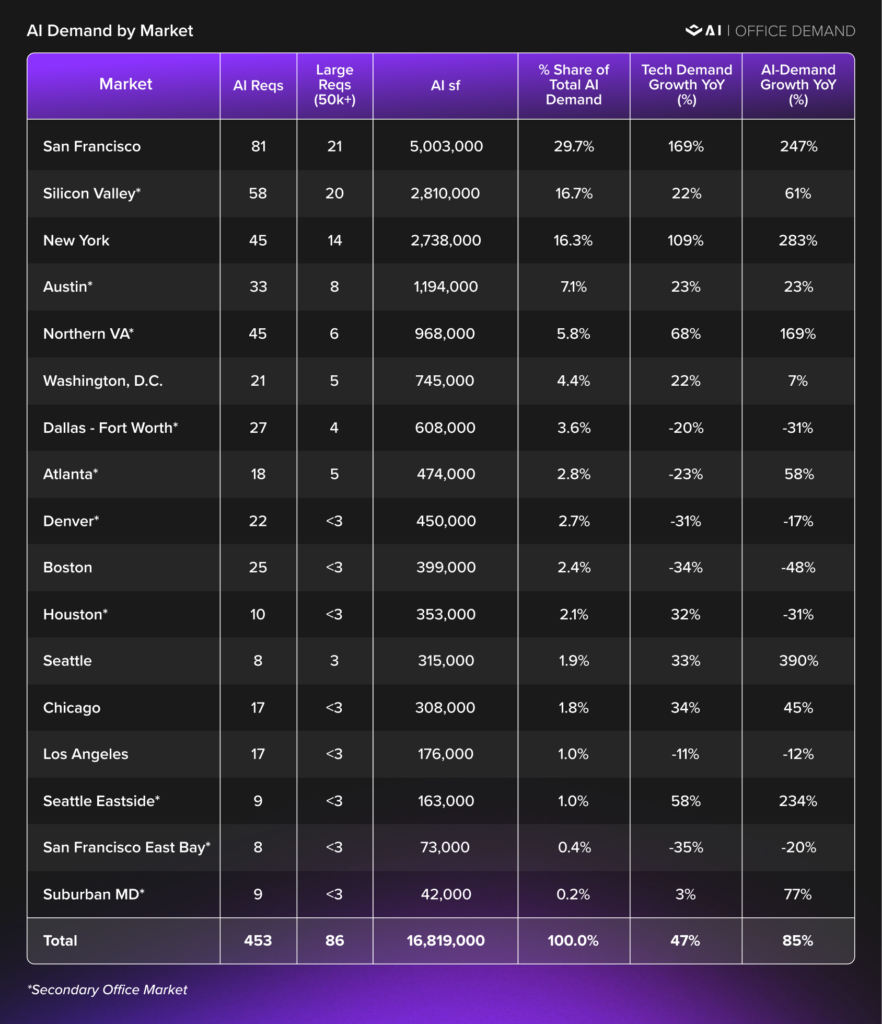

VTS tracks 453 active AI office requirements across 17 US markets. Those tenants account for 16.8M SF, or nearly half of all active tech leasing volume by square footage. AI requirements average 37K SF, compared with 27K SF across the broader tech sector.

Source: VTS

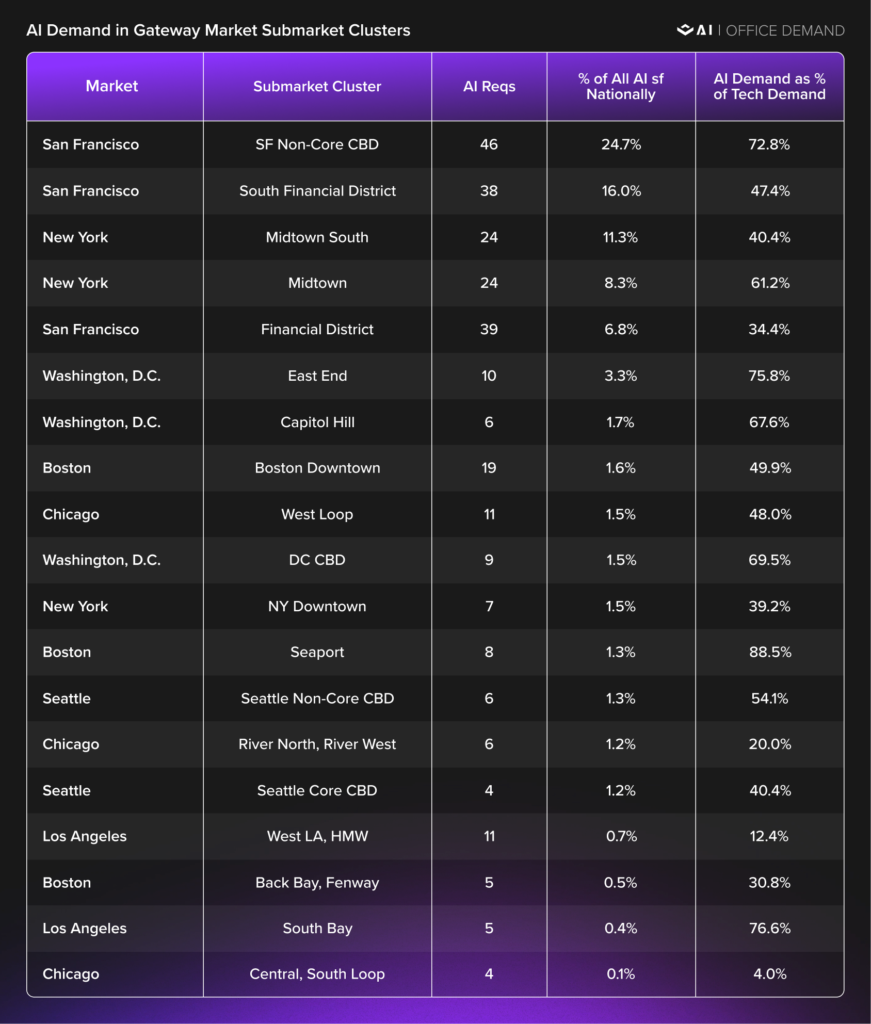

Large transactions are becoming more common. VTS found 91 AI requirements exceed 50K SF, representing 71% of active AI demand. Nearly three-quarters of that large-block activity sits in just six submarkets, including San Francisco’s Non-Core CBD, San Jose, Midtown, Midtown South, San Francisco’s South Financial District, and Austin’s Non-CBD districts.

San Francisco Leads The AI Office Demand Cycle

San Francisco remains the clear leader. The market contains roughly 5M SF of active AI office requirements, almost one-third of the national total tracked by VTS. Silicon Valley follows with 2.8M SF, while New York rounds out the top three. Together, those metros account for 63% of all active AI square footage.

Source: VTS

Secondary markets are also gaining traction. Seattle posted the fastest growth, with AI demand rising 390% year over year. Northern Virginia increased 169%, driven largely by defense-related AI firms. Austin and Atlanta also expanded, though their tenant mix leans more toward established enterprise technology companies than AI-native startups.

Why It Matters

The report reinforces that office performance increasingly depends on neighborhood-level fundamentals rather than metro averages. VTS found one San Francisco submarket alone accounts for 25% of active AI demand nationwide. That concentration is reducing available space in select districts even as many surrounding submarkets continue to struggle with elevated vacancy.

The pattern also mirrors earlier technology expansion cycles. During the post-financial crisis recovery, technology hiring led broader office demand before professional services followed. VTS argues San Francisco may already be entering that next phase, with professional services leasing up 33% over the past year after tech requirements surged 169%.

For landlords, the takeaway is clear. Buildings positioned inside AI clusters could outperform their broader markets, while nearby properties may see little benefit despite sharing the same metro statistics.

What’s Next

VTS expects AI demand to broaden over time, though likely at a slower pace than today’s concentrated growth suggests. High office costs in San Francisco, limited engineering talent, and expanding enterprise AI adoption could encourage companies to grow in markets such as Chicago, Austin, Atlanta, and Seattle.

Still, the report argues the current cycle differs from previous tech booms. Today’s largest AI companies are generating revenue earlier and committing to long-term deployments rather than expanding purely on venture funding. That could make office demand more resilient if funding slows, even if leasing growth moderates. For investors, the next opportunity may depend less on choosing the right city and more on identifying the right submarket before demand spreads further.