- Value-add plays in 1970s vintage multifamily posted strong gains, but re-securitization data shows pace has slowed after 2022.

- Trepp found median value increases of 63% and NOI growth of 39%—but cap rate compression, not just operations, drove much of this upside.

- CRE CLO transitions now show less room for another major valuation reset, signaling value growth must come more from true operational improvements.

Cap Rate Compression Powered Past Value-Add Gains

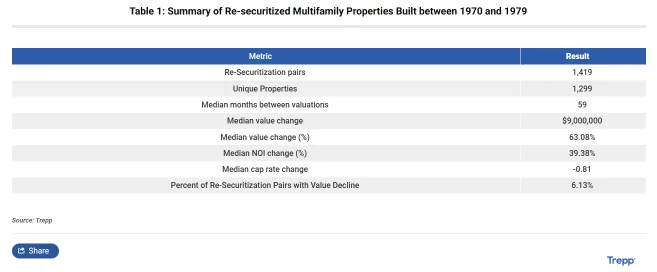

For several years following the pandemic, 1970s-era multifamily buildings became ground zero for value-add strategies. Operators renovated units, hiked rents, and rode strong market demand to boost NOI. According to Trepp’s new analysis of over 1,400 re-securitization pairs involving multifamily assets built between 1970 and 1979, these properties saw a median $9M, or 63%, value increase between sequential securitizations, over a median 59-month period.

Median NOI rose 39%, yet the report points out that cap rate compression accounted for much of the valuation jump, with cap rates falling 81 basis points. Only 6% of pairs showed a value decline—evidence that investor demand and low rates, as much as operational improvements, fueled the run-up.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Trepp analyzed 1,419 pairs across 1,299 unique 1970s-vintage multifamily properties that were re-securitized between 2021 and May 2026. The largest valuation jumps came when properties moved out of conduit loans and into new CRE CLO or agency CMBS executions, posting median value increases of 313% and 193%, respectively, over long holding periods (17–20 years).

Cap rate drops for these transitions were dramatic: conduit-to-CRE CLO transitions registered a median decrease of 290 basis points, and conduit-to-agency CMBS saw a drop of 258 basis points. In contrast, when a loan was already in a CRE CLO, the subsequent increase was limited—just 14% for CRE CLO-to-agency pairs and 27% for CRE CLO-to-CRE CLO—reflecting that the low-hanging fruit in value appreciation had already been picked during the initial transition.

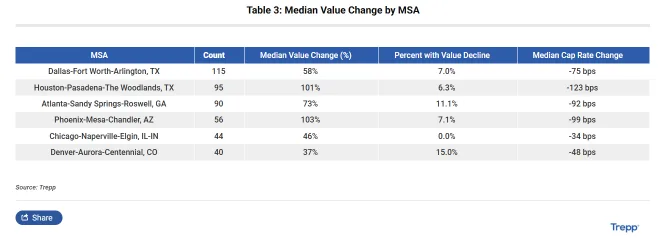

Sun Belt Markets Led Through the Boom

Sun Belt MSAs like Houston and Phoenix capitalized most on this trend, per Trepp’s findings. Houston’s median value increase hit 101% with cap rates falling 123 basis points; Phoenix rose 103% with a 99-basis-point drop. Atlanta and Dallas-Fort Worth also saw outsize gains, at 73% and 58%, respectively, both posting notable compressions.

In contrast, mature gateway markets like Chicago and Denver posted more muted results, with Chicago at 46% and Denver at 37% for median value increases, and both showing far less cap rate compression. The data illustrates the regional variances underpinning the vintage multifamily value-add boom.

Why It Matters

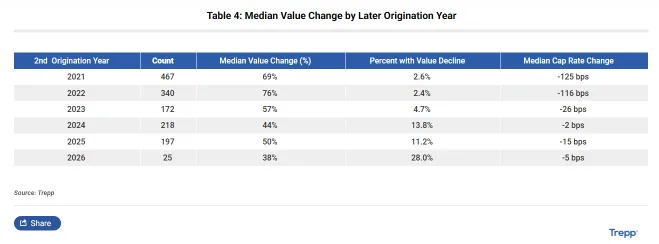

The real story is the shift in wind direction. Trepp’s breakdown by year shows how the catalyst of cap rate compression started to fade after 2022. Recent underwriting trends also suggest multifamily pricing assumptions are becoming less aggressive as investors adjust to higher borrowing costs. Median value increases reached 69% in 2021 and 76% in 2022, alongside the largest drops in cap rates. But that momentum slowed sharply: in 2023 through 2026, the median value increase fell as low as 38% and cap rate compression dwindled, even turning slightly negative. The risk of value declines rose—jumping to nearly 14% of pairs in 2024 and a striking 28% in early 2026, albeit on a small sample.

The implication for investors and lenders is clear: the age of easy value-add wins for 1970s assets, fueled by ever-compressing cap rates, may have closed. CRE CLO and re-securitization data highlight that future appreciation will need to come from genuine NOI improvements—better expense control, rent growth, and renovations that deliver durable value—rather than broader market multiple expansion.

Given that 1970s-vintage properties often present deferred maintenance and higher operating risk, underwriting will need to sharpen, especially when refinancing out of a previously aggressive valuation basis. The market’s focus is shifting from financial engineering to operations and market selection. As capital costs remain higher, lenders must scrutinize the real uplift embedded in each value-add plan.

What’s Next

Looking ahead, CRE professionals eye a tougher environment for generating multifamily value-add upside, especially in the aging 1970s stock. Without the leverage of falling cap rates, borrowers and lenders will need a sharper focus on real NOI growth, cost control, and realistic renovation underwriting. Sun Belt metros may still offer opportunities but with greater execution risk. For anyone refinancing or buying into these assets using the CRE CLO structure, market discipline will be key, as cap rate tailwinds are largely spent and the next phase of returns must be earned, not presumed.