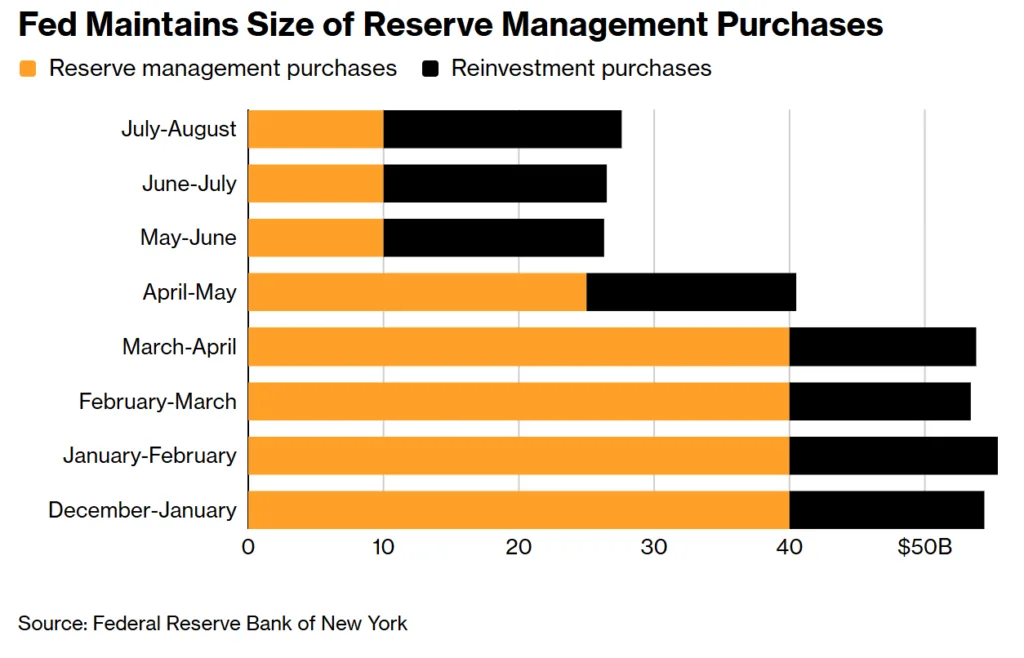

- The Fed will maintain reserve management purchases at $10B through August 13, per the New York Fed.

- This amount is unchanged from the previous two cycles, despite rising Treasury bill issuance and planned cash balance growth.

- Continued caution reflects concerns about system liquidity and funding market stability as reserves fluctuate.

Fed’s Balance Sheet Pivot Sets the Stage

According to Bloomberg, the Federal Reserve is leaving the size of its reserve management purchases (RMPs) unchanged this cycle, opting to buy about $10B in Treasury bills for the period ending August 13. These ongoing purchases follow the central bank’s abrupt halt of its balance sheet runoff (quantitative tightening) at the end of 2025 and its renewed focus on injecting reserves via short-term government securities.

This latest move underscores the Fed’s ongoing shift from draining to replenishing banking sector liquidity amid risks of future reserve declines tied to the Treasury’s borrowing strategy.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

The New York Fed’s open markets desk will conduct $10B in RMPs and plans to execute roughly $17.6B in reinvestment purchases over the same period. Bank reserves reached $3.14T as of July 8, up significantly from $2.85T at the end of 2025.

The Fed started aggressively adding bills to its holdings in December 2025—peaking at $40B monthly—but then cut back sharply to $25B in April, and again to $10B in May, a pace that surprised some investors. The central bank has made clear that these purchase levels are not fixed and can adjust in response to money market conditions.

Pressures on Liquidity and Funding Costs

The Treasury expects to ramp up bill issuance this quarter, aiming to boost its cash balance above $1T—moves that tend to drain system reserves as they pull cash out of the banking sector. Historically, such reserve drains can push up funding costs and squeeze money market liquidity. Higher financing costs can also weigh on acquisition activity, especially as investors already show greater caution in deploying capital this year.

Despite higher reserves, the last month saw soft funding conditions as excess cash flowed into money-market funds, with repo investments rising ahead of the Fed’s next policy meeting. The secured overnight financing rate (SOFR), which tracks the cost of borrowing against Treasuries, has been consistently below the Fed’s interest on reserve balances (IORB) rate and recently hit a six-week low.

Why It Matters

With reserves sitting at $3.14T and Treasury bill supply set to climb, the Fed faces a delicate balancing act to maintain liquidity while avoiding market disruptions. The central bank’s explicit willingness to pause or adjust RMPs as needed (updated in last month’s policy statement) signals its focus on being nimble as risks to funding market stability evolve. History shows that past missteps in draining reserves too quickly led to funding market volatility, and policymakers are clearly wary of repeating those errors despite confidence in market functioning.

The broader implication is that ongoing Treasury supply growth—and the associated cash draw from the system—forces the Fed into a closely monitored, data-driven approach to liquidity management. Investors and CRE stakeholders should watch for changes in repo rates and Fed signaling, as shifts in these “plumbing” details can have outsized effects on financial conditions. According to Bloomberg’s analysis, funding softness could persist until the Treasury’s cash buildup stabilizes and the Fed’s pace of reserve additions aligns with market needs.

What’s Next

The Fed is expected to reassess its reserve purchase schedule after the August 13 cycle. Short-term, policymakers will monitor money market softness and the SOFR-IOBR spread—potential indicators of liquidity strain. The New York Fed reiterated last week that RMPs remain flexible, with future increases or pauses possible depending on Treasury activity and market sentiment.

Commercial real estate investors should stay alert: funding pressure episodes in the coming weeks could ripple out to lending rates and deal financing costs, especially if reserve drains accelerate or volatility returns to short-term rates.