- The US industrial market is stabilizing after a sharp post-pandemic correction, with national quality-adjusted rents remaining nearly 70% above 2019 levels.

- CompStak data shows bulk industrial rents turned positive year-over-year in Q1 2026, while New Jersey and Philadelphia lead upcoming renewal upside.

- Higher e-commerce penetration, leaner inventories, and slower construction point toward tighter warehouse conditions ahead.

US Industrial Market Shows Signs Of Stabilization In 2026

The US industrial market is entering a more balanced phase after several years of rapid rent growth, new supply, and shifting tenant demand.

According to CompStak’s 2026 Biannual Industrial Market Overview, national industrial rents have largely plateaued, while leasing activity is showing early signs of stabilization across major markets.

The report analyzed eight major industrial markets through Q1 2026, including Los Angeles, Atlanta, Phoenix, Chicago, New Jersey, Philadelphia, Houston, and Dallas-Fort Worth. The data points to a market where pricing has reset in some regions but remains elevated compared with pre-pandemic levels.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Industrial Market Shifts After Post-Pandemic Expansion

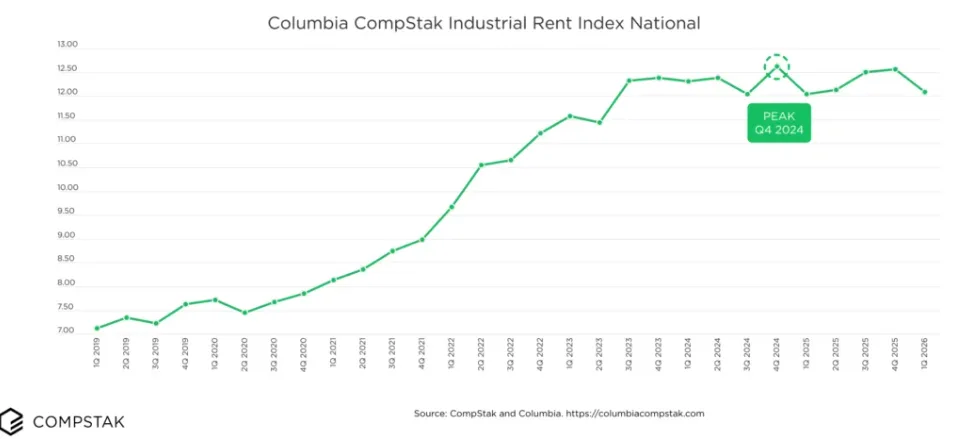

The industrial sector has moved beyond the explosive growth period that defined 2020 through 2022. CompStak’s Columbia CompStak Rent Index (CCRI) shows national quality-adjusted industrial rents have remained within a narrow range for eight consecutive quarters.

The index reached 12.61 in Q4 2024 before declining to 12.08 in Q1 2026. That represents only a 4.2% decline from the peak. Since Q1 2019, industrial rents remain 69.7% higher, indicating that much of the pandemic-era pricing growth has held.

Market performance has varied widely by geography. West Coast markets have experienced the steepest corrections. The Inland Empire CCRI has fallen 31.1% from its peak, while Los Angeles has declined 25.7%. Meanwhile, Chicago remains at a cycle high, and Dallas-Fort Worth is down just 0.4% after five quarters of declines.

The Details

CompStak found that bulk industrial properties are showing early signs of recovery. Average adjusted effective rents for bulk transactions of 200,000 SF or more reached $10.66 PSF in Q1 2026, marking a 0.9% year-over-year increase.

Non-bulk industrial rents moved in the opposite direction. Those transactions averaged $12.67 PSF in Q1 2026, down 1.7% year-over-year. Both segments remain below their previous peaks, but the gap suggests larger industrial facilities are stabilizing faster.

Lease economics continue to favor tenants compared with pre-pandemic conditions. Free rent reached cycle highs across both segments, with non-bulk concessions reaching 4.5% of lease term in Q1 2026. Bulk free rent eased slightly to 4.8% after reaching 4.9% in Q4 2025.

The report also found renewal pricing is diverging by asset size. Lease renewals for industrial properties larger than 500,000 SF increased 83.7% above previous lease rates in Q1 2026, nearly doubling from 49.2% in Q2 2025. Smaller transactions continued to see more limited rent growth.

E-Commerce Growth Supports Warehouse Demand

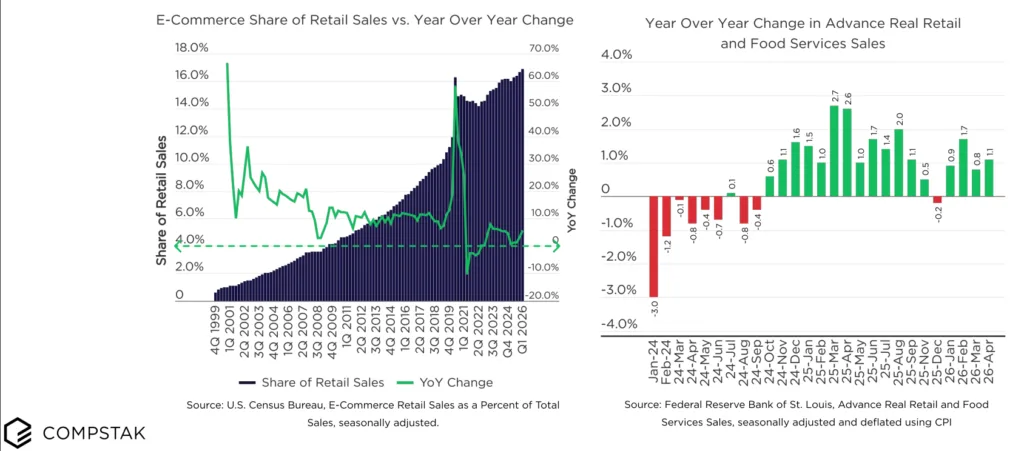

The long-term demand drivers behind industrial real estate remain intact. According to the US Census Bureau, e-commerce accounted for 16.9% of retail sales in Q1 2026, surpassing the previous pandemic-era peak of 16.3% in Q2 2020.

The shift toward online shopping has continued despite tariff uncertainty and changing consumer behavior. After stabilizing around 14% to 15% between 2021 and 2022, e-commerce penetration crossed 16% in Q2 2024 and continued climbing.

Inventory trends also point toward potential warehouse demand. The US Census Bureau reported the retail inventories-to-sales ratio declined to 1.26 in March 2026 from a peak of 1.33 in August 2024. Leaner inventories could create additional demand for distribution capacity if retailers begin rebuilding stock levels.

Supply Growth Slows Across Industrial Markets

Industrial construction activity is cooling after reaching historic highs. Commercial construction spending, including warehouse and distribution facilities, peaked at $155.4B in September 2023 and declined approximately 21% to $122.3B by April 2026, according to the US Census Bureau.

The slowdown could reduce future supply pressure in major logistics hubs. Developers delivered significant warehouse space during the post-pandemic expansion, but a slower construction pipeline may help markets absorb existing inventory.

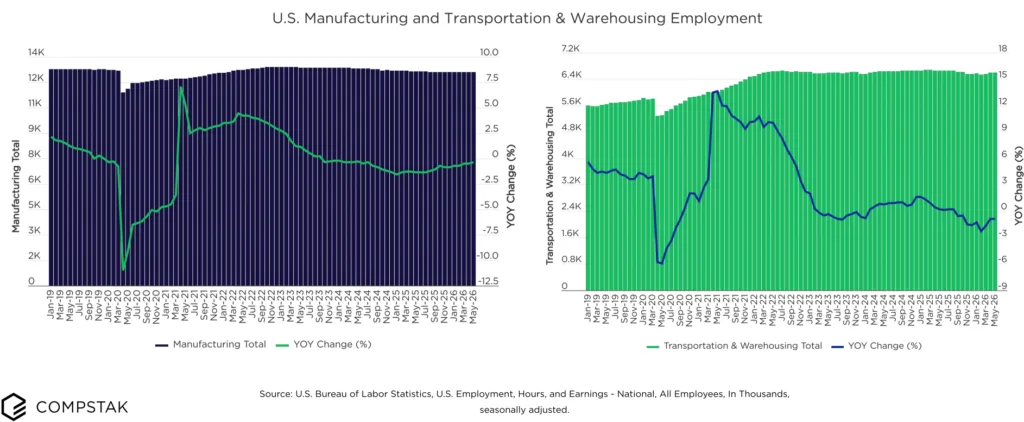

Labor trends remain mixed. Manufacturing employment stabilized in early 2026 after falling 2.5% between January 2023 and December 2025. Transportation and warehousing employment, however, remained down 0.9% year-over-year through May 2026, according to the US Bureau of Labor Statistics.

Renewal Markets Create New Opportunities

Lease expirations will create different outcomes depending on geography. CompStak estimates roughly 31% of leased industrial SF across major markets will expire between Q3 2026 and Q2 2028.

New Jersey has the strongest potential for rent resets, with current market rents running 35% to 42% above in-place rents for expiring leases. Philadelphia follows closely, with spreads reaching 32% to 36%.

Los Angeles faces the opposite challenge. The market accounts for more than one-third of upcoming expiration volume, but current rents are approximately 2% below existing in-place rents, creating limited upside for landlords.

Why It Matters

The industrial market is no longer driven by broad-based rent increases. Instead, performance is becoming increasingly dependent on market location, building size, and tenant demand.

The stabilization of bulk rents suggests larger distribution facilities may be regaining leverage as occupiers prioritize logistics efficiency. At the same time, elevated concessions and uneven renewal trends show tenants still hold negotiating power in many segments.

For investors and operators, the next phase will likely depend less on rent growth and more on asset quality, supply discipline, and regional fundamentals.

What’s Next

Industrial owners will be watching lease expirations through 2028 closely, especially in markets with large spreads between current and in-place rents. New Jersey, Philadelphia, Dallas-Fort Worth, and Atlanta appear positioned for stronger mark-to-market opportunities.

Meanwhile, slower construction activity and continued e-commerce adoption could support tighter conditions over time. The sector’s next cycle will likely be defined by selective growth rather than the broad expansion seen after the pandemic.