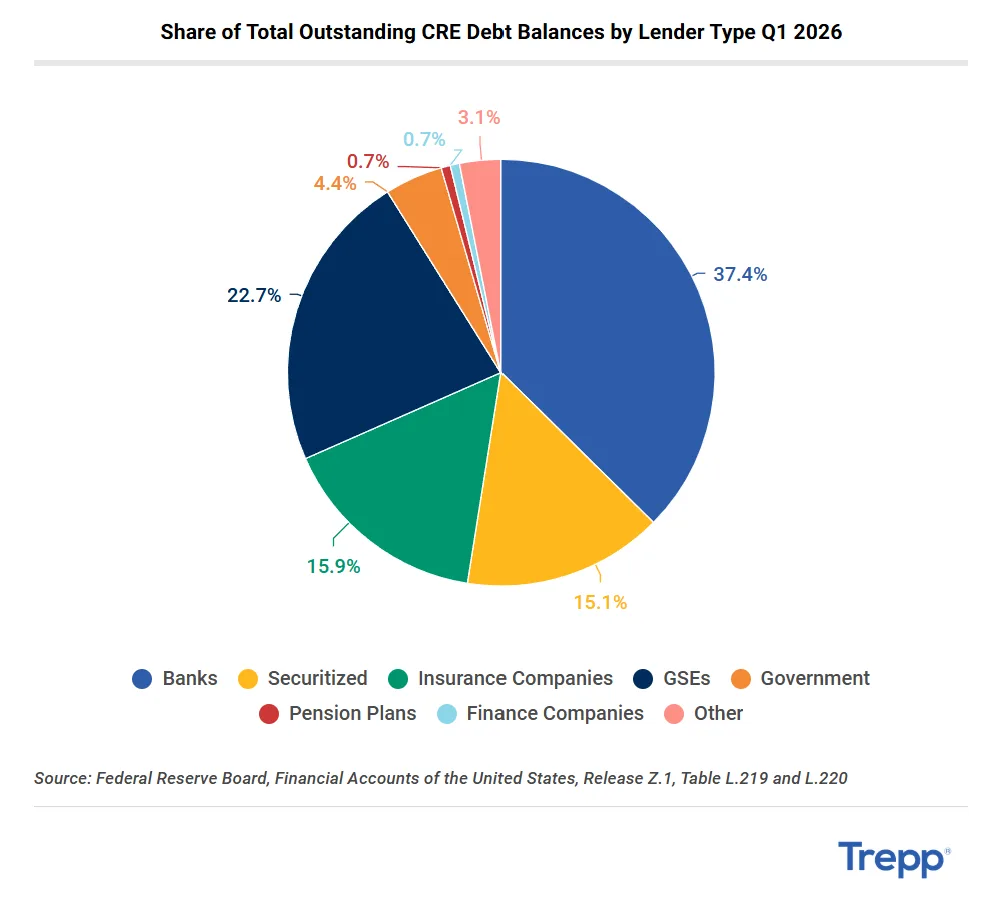

- Total US commercial real estate debt reached $5.1T in Q1 2026, according to Trepp.

- Banks hold the largest market share with $1.91T in income-producing loans and continued steady growth.

- Near-term maturity risks are concentrated in banks and securitized lenders, while most debt still matures after 2031.

Debt Market Stability Amid Global Uncertainty

Total US commercial real estate debt climbed to $5.1T through the first quarter of 2026, per Trepp’s latest CRE Debt Universe report. Banks remain the leading player, controlling $1.91T, or 37.4% of income-producing loans. The remainder is divided among government-sponsored enterprises (GSEs) at $1.16T, insurance companies at $808B, and securitized lenders with $771B. The overall lender composition has held steady, indicating recent growth hasn’t created structural shifts in who holds CRE risk.

Trepp’s report draws on Federal Reserve Z.1 data and highlights how most lender balance sheets saw modest expansion even as monetary policy, rate cuts, and global tensions complicated the credit outlook. This adds context for sponsors, investors, and capital markets firms evaluating where risk and opportunity cluster in the current cycle.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Bank Credit: The Reliable Anchor

Banks expanded steadily in Q1 2026 despite earlier rate swings and tighter credit. They grew income-producing loan portfolios 4.1% year over year and 1.0% from Q4 2025.

Banks held $1.91T in income-producing loans. They also carried $454B in construction debt and $704B in owner-occupied loans. Their exposure spans stabilized assets and new projects, although lenders remain selective.

Meanwhile, GSEs and insurers maintained their positions. Their long-term loans create later maturity schedules and help cushion refinancing pressure.

Securitized Growth, Maturity Buildup, and Market Comparisons

Securitized lending regained momentum in Q1 2026. Balances rose 2.1% from Q4 and 8.6% year over year after a slow fourth quarter.

Investors continue to support structured CRE credit despite growing economic and geopolitical concerns. Banks and securitized lenders face most near-term refinancing risk. About $311B in bank loans and $186B in securitized debt mature by the end of 2026.

By comparison, roughly $1.7T in CRE debt will not mature until 2031 or later. GSEs and insurers hold most of that debt, giving them more flexibility. This maturity gap remains a key distinction as market conditions evolve.

Why It Matters

The $5.1T CRE debt market creates refinancing challenges for operators and investors. According to Trepp, banks and securitized lenders face the biggest hurdle. Together, they account for $497B in maturities through 2026.

GSEs and insurers hold most longer-dated debt. Their conservative approach may reduce systemic risk, but it can limit capital availability. Multifamily loans continue to make up a large share of GSE portfolios, which helps explain their longer maturity schedules.

Geopolitical tensions and an uncertain rate outlook add pressure. Sponsors should monitor lender composition closely. Banks continue to expand steadily, which offers stability. However, any market shock would affect a concentrated group of lenders.

Securitized issuance still reflects investor confidence. Yet sentiment could change quickly if conditions weaken. Overall, debt structure and maturity timing remain critical issues for US CRE participants.

What’s Next

All eyes remain on the Federal Reserve as the market gauges further monetary easing in 2026. If rates remain constrained, banks and securitized lenders could see continued modest growth, but refinancing bottlenecks won’t disappear. According to Trepp, lenders will likely focus on repricing risk and managing maturity spikes. For sponsors, proactive negotiations and careful lender selection will be pivotal, especially for properties facing near-term maturities. As geopolitical events and domestic policy continue to inject volatility, flexibility in capital structures and strong lender relationships will be more important than ever for navigating the evolving CRE debt landscape.