- Owners of Hilton-branded hotels have hit a 16% delinquency rate on CMBS-backed loans, twice the US average, according to KBRA.

- Troubled debt is largely concentrated in major downtown markets, with just two San Francisco Hiltons accounting for $725M of late payments.

- Asset selection risk is rising as economic headwinds challenge hospitality owners’ recovery in slow-growth metros like Chicago and San Francisco.

Delinquencies Rise Among Major Hotel Chains

Hilton owners are facing a mounting debt crisis, outpacing reputational rivals on delinquency. Bisnow reports that nearly 16% of all CMBS loans backed by Hilton-branded US hotels are in default, per a June 2026 KBRA analysis. That’s more than double the average across US hospitality CMBS, signaling a brand-specific challenge. The financial pain is most intense in select urban markets—San Francisco and Chicago, in particular—where recovery from the pandemic remains slow and footage is piling up. This poor debt performance stands in contrast to Marriott (7% delinquency) and Hyatt (2.8%), putting Hilton in the spotlight for lenders watching hospitality exposure.

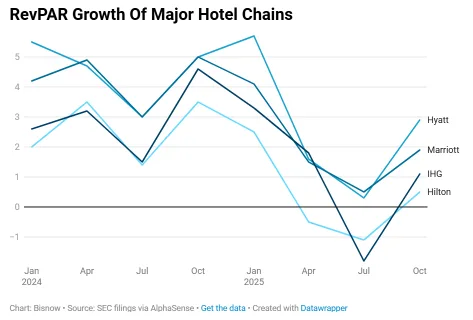

The 724 Hilton-branded US hotels subject to CMBS financing collectively hold $15.9B in outstanding debt, with $2.5B now delinquent. In contrast, Marriott-branded properties have $1.6B in delinquent loans out of a $23.2B CMBS total. The divergence suggests a brand—and market—predisposed to deeper financial stress. Slow revenue growth also spotlights the scale of the challenge: Hilton’s 2025 RevPAR grew just 0.4%, compared to up to 2.9% for Hyatt, emphasizing its operational lag even as it maintains an asset-light, expansion-focused model.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Pandemic Fallout Lingers for Hilton Owners

Hilton’s higher delinquency rate stems from distress at several large legacy properties. These hotels sit in struggling downtown markets. San Francisco alone accounts for nearly $725M in overdue mortgage payments. The debt comes from two major downtown Hilton hotels, according to KBRA and Morningstar. The pandemic hit these assets so hard that Park Hotels & Resorts returned the keys. Lenders later restructured the loans, but they remain in special servicing.

Meanwhile, Chicago’s iconic Palmer House Hilton has faced foreclosure and litigation since 2020. The hotel has operated continuously since 1871. It also remains a favorite piece of CRE trivia. Officials declared its original $330M loan unrecoverable. As a result, debt holders remain stuck despite repeated repossession efforts.

The Details

KBRA data highlights Hilton’s challenges among major hotel brands with CMBS exposure. Hilton’s 16% delinquency rate exceeds IHG’s 12.5%. It also far surpasses Hyatt’s rate below 3%. The Palmer House’s troubled $330M loan and San Francisco’s $725M default show how concentrated distress can become.

A total of 724 Hilton-branded US properties carry $15.9B in loans. That means about one in every six loan dollars now faces risk. Even so, Hilton stayed asset-light and earned nearly $1.5B in net profits during 2025. However, lenders and owners still grapple with poorly timed pre-pandemic urban hotel deals.

Urban Hotel Recovery Trails in Key Markets

The greatest stress appears in slow-recovery cities such as Chicago and San Francisco. Lodging Analytics Research & Consulting expects both markets to rank in the bottom quartile for RevPAR growth. The forecast covers the next five years across the 64 largest US hotel markets.

Pandemic aftershocks continue to weigh on performance. Challenging business conditions, high operating costs, and weak international travel also hurt demand. Consequently, full-service flagships struggle to recover like limited-service hotels or Sun Belt peers. By the numbers, San Francisco’s two recently traded Hilton hotels supplied 8% of the city’s hotel rooms. That figure shows how much legacy assets can influence local markets.

Why It Matters

Distress among Hilton-branded hotels warns CMBS lenders and hotel investors. Recovery prospects differ widely by brand and location. KBRA estimates the national CMBS hotel delinquency rate at roughly 7%. Hilton’s 16% rate reflects concentrated weakness in urban big-box hotels.

Hilton’s RevPAR rose only 0.4% year over year in 2025. Competitors posted gains between 1.5% and 2.9%. Therefore, investors face greater risks when operators cannot adjust to changing market conditions.

In Chicago and San Francisco, hotel CMBS performance closely tracks these troubled assets. The Palmer House Hilton illustrates the problem. Legal disputes, structural issues, and weak demand left its $330M loan unrecoverable. Bondholders lost meaningful repayment options.

Two San Francisco Hiltons sold at steep losses. They fetched $408M against an $874M loan balance. Their modified debt also remains in special servicing. This outcome shows how legacy assets can drag down portfolios and limit workout gains. Ultimately, lenders, investors, and operators must weigh concentration risks more carefully. They should also scrutinize urban full-service hotels as energy costs and other headwinds persist.

What’s Next

Persistent economic uncertainty will likely pressure troubled hospitality borrowers. Recovery-challenged and secondary markets appear especially vulnerable. Although the sector started 2026 strongly, global instability and rising costs weakened momentum. Hotel operators also face fresh uncertainty as geopolitical tensions threaten international travel demand and corporate bookings. As a result, default and workout risks have increased.

KBRA researchers expect gaps between brands and cities to widen in coming quarters. Asset selection and market analysis will become even more important. Elevated delinquencies in Hilton-heavy markets also keep bondholders seeking resolutions. Urban hotels will depend on stronger demand, better capital deployment, and improved operating leverage. However, meaningful progress before 2027 appears unlikely.