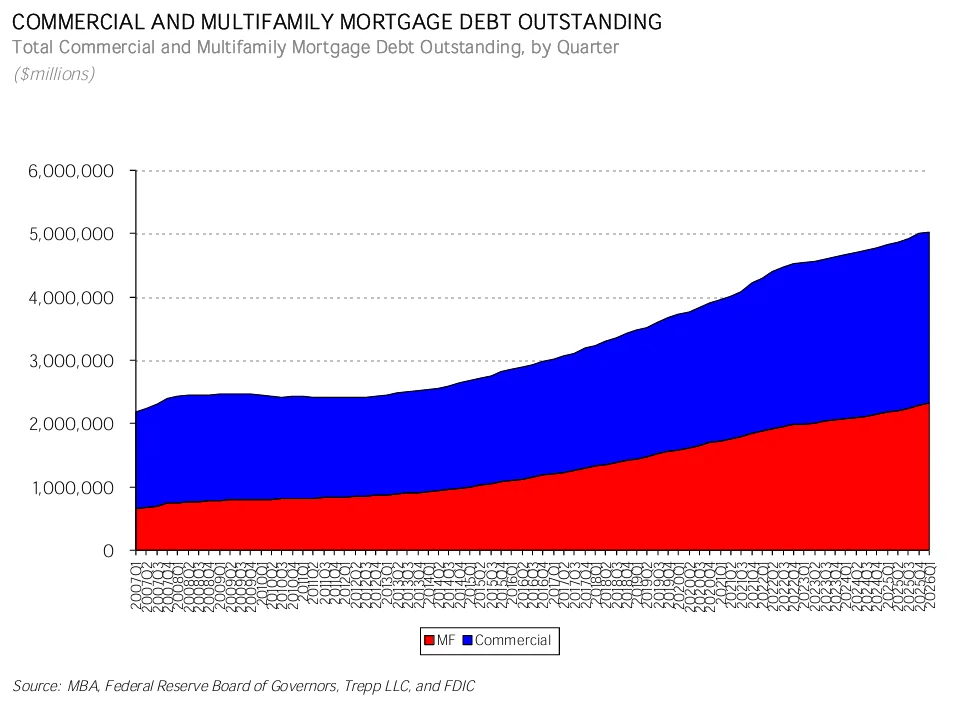

- Commercial and multifamily mortgage debt topped $5T in Q1 2026, per MBA.

- Multifamily accounted for the bulk of growth, rising by $23B to reach $2.32T.

- CMBS balances declined, while banks and agency portfolios expanded their market share.

Multifamily Momentum Powers CRE Debt Expansion

Globe St reports that the US commercial real estate mortgage balances cleared the $5T mark for the first time in the first quarter of 2026, according to the Mortgage Bankers Association. Nearly every dollar of growth was credited to multifamily, which added $23B in outstanding balances—dwarfing gains in other property types. In a market where many asset classes are constrained by rate volatility and uneven demand, multifamily remains the outlier, pushing total commercial and multifamily mortgage debt to $5.02T overall.

This trajectory stands in contrast to the broader CRE lending landscape, which continues to struggle with higher debt costs and tightening standards. The outsized role of multifamily underscores not just a cyclical trend, but a durable shift in how—and where—lenders are choosing to deploy capital.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

According to MBA data, nearly all first-quarter mortgage debt growth came from multifamily, with outstandings rising 1% to $2.32T. Agency and GSE portfolios, including mortgage-backed securities, now represent 49.9% of multifamily balances ($1.16T). Banks and thrifts hold 28.7% ($665.25B) and life insurers account for 11.4% ($264.53B).

Across all commercial and multifamily debt, banks and thrifts are the top holders at $1.88T (37.5% of total), agency/GSE portfolios follow at $1.16T (23%), and life insurers tally $774.58B (15.4%). CMBS, CDO, and similar asset-backed securities currently account for $636.85B (12.7%), but that segment shrank by $9.59B—marking the sharpest pullback among major investor groups during the quarter.

Banks and Agencies Steady, Securitization Slows

While banks and agencies expanded their holdings—banks and thrifts grew by $17.47B, agencies/GSEs by $12.83B—securitized lending continued its retrenchment. CMBS and related securities saw outright declines, as investors remained wary of market volatility and widening credit spreads. Still, securitization remains active in niche sectors, particularly data centers, where large issuance deals continue to attract capital.

The lending environment is increasingly bifurcated: regulated institutions and government-backed capital provide stability and growth, while capital markets execution through securitization faces ongoing headwinds. This pattern leaves multifamily—which benefits from deep agency liquidity—in a distinctly advantaged position compared to office or retail assets reliant on less active lending channels.

Why It Matters

The first quarter’s data cements multifamily as the most financeable sector in US CRE. As agency and GSE lending fills structural gaps left by more risk-averse and retreating capital sources, sponsors in multifamily enjoy a rare stability that office, retail, and even industrial sectors cannot easily replicate. Per MBA, agency-backed portfolios not only represent nearly half of all multifamily debt, but also reliably add liquidity in a credit-constrained environment.

Meanwhile, banks and thrifts, buoyed by regulatory frameworks and stable balance sheets, have remained active, adding $17.47B in new commercial and multifamily loans. This bank-driven growth contrasts sharply with the double-digit decline in CMBS outstandings ($9.59B drop), reinforcing the view that securitization is still facing skepticism from investors wary of duration and credit risk. Only life insurers registered modest expansion, suggesting most other capital channels are content to tread water or shrink exposure.

For CRE players, the upshot is clear: deals with access to agency, GSE, or bank execution can still achieve scale. Those leaning on securitized or alternative lenders should expect tighter terms, more scrutiny, and potential delays.

What’s Next

Looking ahead, market participants should expect further divergence in the capital stack. Agency and bank lending is likely to continue powering overall CRE debt expansion, especially in multifamily. While CMBS market sentiment could improve if volatility and spreads stabilize, most indications from Q1 suggest capital will remain asset- and source-specific. Investors should track how much longer multifamily can outpace the rest of CRE—and whether other property types can regain the confidence of capital markets lenders as fundamentals evolve in 2026.