- AMER data centers surpassed health care as the most overweight sector in global actively managed REIT funds in Q1 2026, per the tracker.

- APAC diversified and EMEA retail showed notable annual sector gains, but both regions remain underweight in managers’ global allocations.

- Shifts reflect broader investor pivot toward digital infrastructure, while residential sectors, especially in the Americas, saw the largest declines.

Data Centers Outpace Health Care in Manager Portfolios

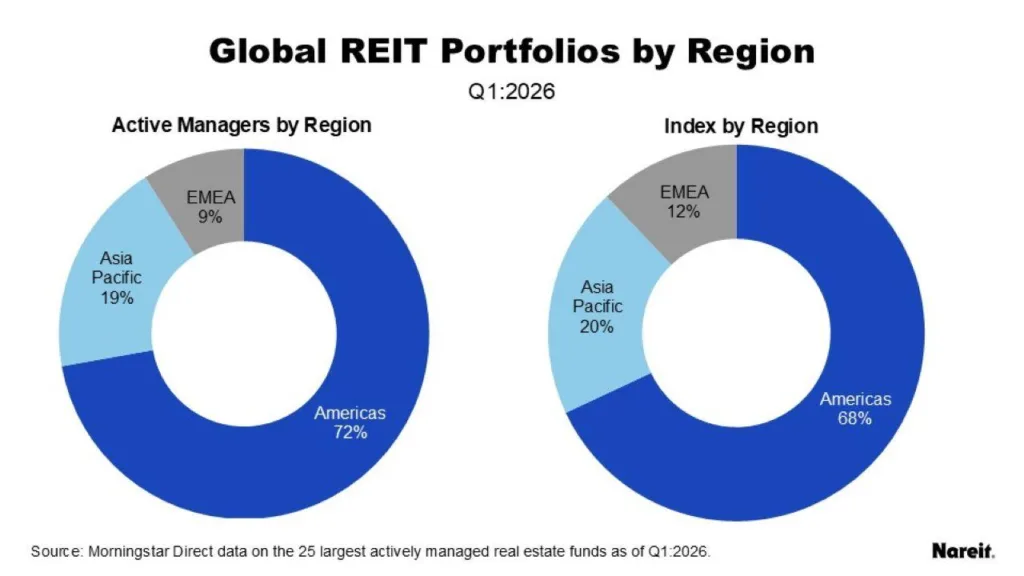

Quarterly findings from the global active manager tracker, reported by industry sources, show that AMER (Americas) data centers have overtaken health care as the top overweight sector among the 25 largest actively managed global REIT funds in Q1 2026. According to the tracker, these funds collectively managed $17B across 35 markets as of March 2026. The collective maintained a geographic tilt: still overweight AMER, primarily the US, and underweight EMEA (Europe, Middle East, Africa) and APAC (Asia Pacific) versus the FTSE/EPRA Nareit Developed Extended Index. The data center sector saw the strongest quarterly gain, climbing 2.2 percentage points to become the dominant overweight—marking a significant sector rotation from health care allocations.

Beyond the top line, sector allocations continue to shift as digital infrastructure and diversified strategies claim growing manager attention amid uneven global performance. Health care in the Americas, while still prominent, was edged out for the largest overweight by the rapid ascent of data centers this quarter, reflecting changing occupier trends and structural tailwinds.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The End of Defensive Dominance in REIT Allocations

Active managers long favored health care and residential sectors in North America during uncertain periods. In APAC, diversified assets held the largest allocation share. However, digital infrastructure is emerging as a core real estate play. Health care’s dominance in benchmark-relative allocations now appears to be fading.

The FTSE/EPRA Nareit Developed Extended Index remains the key benchmark. Still, investors are moving capital quickly toward sectors offering stronger growth and yield.

Across APAC, diversified allocations fell to 14.1% from 15%. Meanwhile, EMEA allocations remain limited. Only diversified, retail, and industrial sectors attract notable fund interest. Regional overweight and underweight positions persist, while sector preferences continue to shift.

The Details

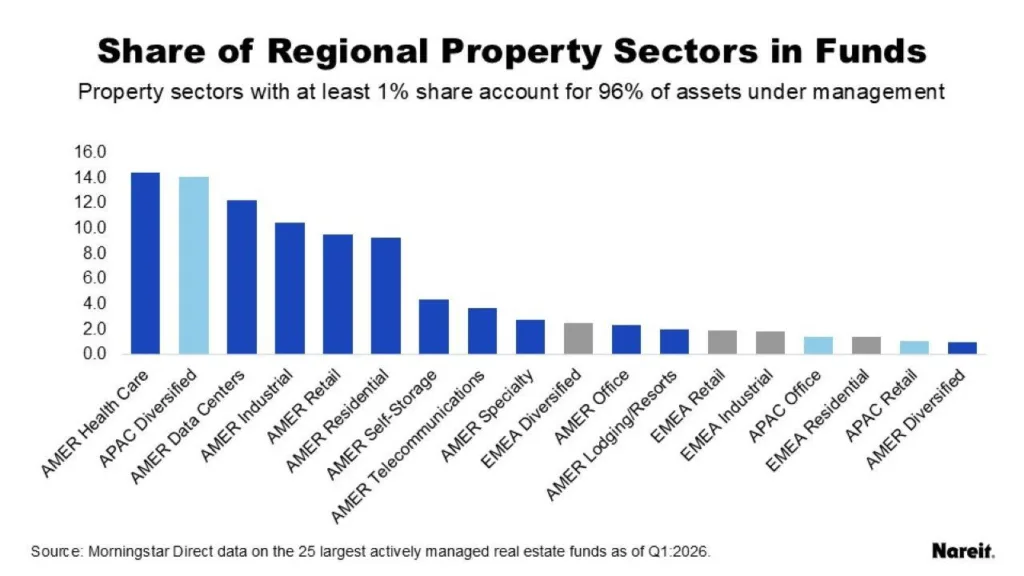

In Q1 2026, AMER data centers made up 12.2% of tracked fund holdings. They surpassed industrial and residential sectors, which dropped to 10.4% and 9.3%.

Data centers are now overweight by 3.2 percentage points versus the benchmark. They represent 135% of their index weighting. Health care remains significant at 14.5% but is overweight by 2.4 points. Seven of 12 AMER sectors remain overweight. Data centers, office REITs at 144% of index, and lodging and resorts at 137% stand out.

APAC diversified ranked as the second-largest sector allocation at 14.1%. However, its weighting declined both quarterly and annually. EMEA’s largest sector allocation is diversified at just 2.5%.

EMEA self-storage remains a notable outlier. It represents 254% of its index share despite its small size. APAC data centers are also overweight at 122% of index. The trend highlights growing global demand for digital infrastructure.

Cross-Regional Rebalancing Accelerates

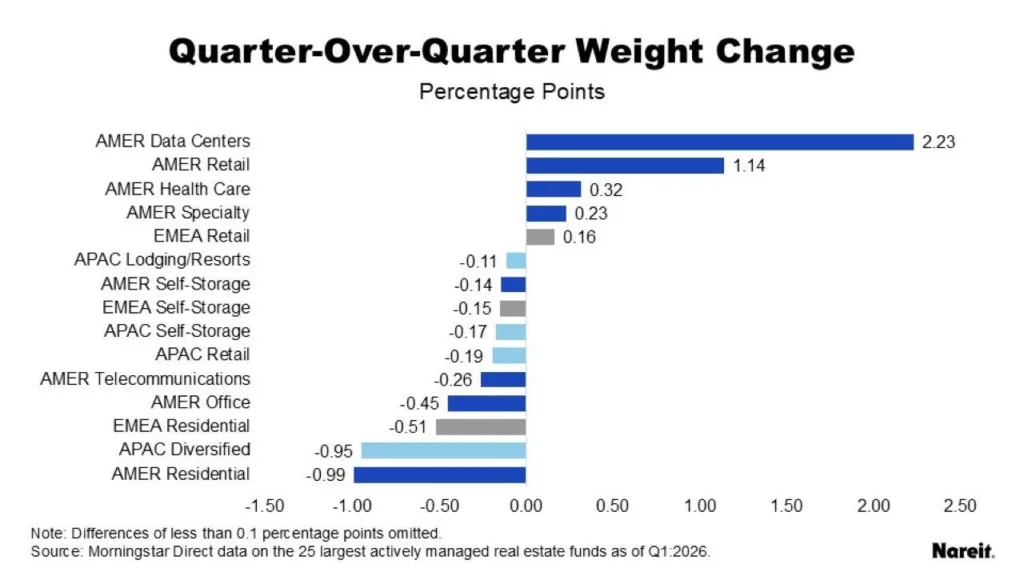

Sector allocations show capital shifting toward stronger fundamentals. Year over year, AMER health care posted the largest gain, rising 2.5 percentage points. Data centers followed with a 2.3-point increase.

Residential sectors in the Americas faced the biggest declines. Allocations fell 1 point quarterly and 4.5 points annually. AMER data centers gained 2.2 points during the quarter. Meanwhile, retail rebounded and added 1.1 points.

EMEA saw smaller and more balanced changes. Diversified was the only sector with meaningful annual growth, rising 0.6 points. Retail posted a modest quarterly increase.

APAC data centers gained 0.1 points during the quarter. Overall, sector changes in Asia Pacific remained limited. APAC overweight sectors include residential at 116%, health care at 106%, and diversified at 104%. Managers appear to favor a balanced approach.

Some sectors remain deeply out of favor. AMER telecommunications stand at 58% of index weight. EMEA office allocations are only 21% of index amid ongoing structural challenges.

Why It Matters

Active REIT managers are shifting toward sectors with long-term growth potential. Data centers are now the most overweight sector in AMER portfolios. Their fund share reached 12.2%, while their overweight climbed to 3.2 percentage points. This preference for specialized sectors mirrors a broader shift toward real assets as investors seek growth amid uncertainty.

Traditional defensive sectors are losing ground. Health care and residential once attracted investors seeking stable income. Today, managers increasingly favor infrastructure-driven growth.

Residential REITs in the Americas recorded their steepest annual decline, falling 4.5 points. APAC and EMEA show more modest changes. Still, investors are showing interest in data centers, diversified assets, and self-storage.

Portfolio construction is becoming more dynamic. The gap between active allocations and index weights continues to widen. Specialized sectors may outperform broad diversification in the next cycle.

Digital infrastructure and niche sectors continue to attract capital. Meanwhile, telecommunications, traditional offices, and timberland need stronger fundamentals to regain investor interest.

What’s Next

Two managers have yet to report Q1 2026 holdings. Their data could refine the picture. Still, the trend is clear. Investors are concentrating capital in high-growth sectors, especially data centers and selected diversified strategies.

Traditional sectors such as residential and telecommunications continue to lose share. Active funds will likely adjust quickly to economic and technology shifts through 2026. Regional differences should persist, but digital infrastructure is poised to remain a major theme in global REIT investing.