- The Harvard JCHS 2026 report warns of a deep affordability crisis squeezing both renters and buyers in the US housing market.

- Housing demand is weakening, vacancy rates are up, and supply is shifting, but low-income households see little relief as most new stock misses their price point.

- Despite softer rents and slower home price growth, broad policy changes and expanded federal support are needed to address persistent inequality and systemic market dysfunctions.

Supply-Demand Imbalances Persist

The latest State of the Nation’s Housing report from Harvard’s Joint Center for Housing Studies paints a challenging 2026 landscape: the US housing market is caught between worsening affordability and faltering demand, according to the JCHS (per The State of the Nation’s Housing 2026). While existing home sales remain near three-decade lows and new construction has slowed, rent growth has slipped and vacancies have drifted upward, but these shifts have not made housing more accessible to lower-income groups. Instead, both renters and would-be buyers are finding fewer affordable options as policymakers and builders struggle to close the gap.

What sets this period apart is that neither the supply nor demand side is providing relief. The report highlights that while 2025 saw vacancy rates rise from historic lows, the supply added has been both insufficient in scale and poorly targeted: most new units — whether apartments or single-family homes — remain far out of reach for households earning below the median. The result is a US housing market with more options in theory, but little practical improvement for those most affected by cost burdens.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Harvard’s JCHS says household growth slowed for a third straight year. Households formed 1.1M new households in 2025. That was nearly half the 2020–2021 pace.

A weaker labor market weighed on demand. Employers added just 116,000 jobs in 2025. That marked the weakest non-recession job growth since 2002. Meanwhile, student loan delinquencies climbed after pandemic relief expired. They rose from under 1% in late 2024 to 10% in 2025.

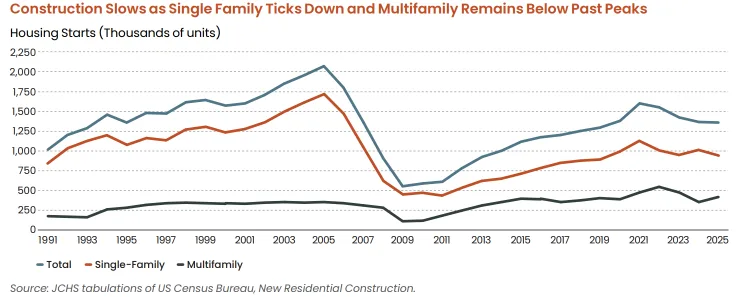

Mobility also hit a record low. Only 11.2% of households moved in 2024. High housing costs, mortgage lock-in, and uncertainty kept people in place. Single-family starts fell 7% to 940,600 units in 2025. Multifamily starts rebounded 17% year over year. However, they remained 24% below their 2022 peak.

Build-to-rent made up 11% of single-family completions. Historically, it averaged about 4%. Housing vacancies edged higher to 1.1% for owners and 7.3% for renters. Still, rates remained below pre-pandemic averages. That points to an ongoing shortage of affordable homes.

New multifamily units posted a median asking rent of $1,900. Meanwhile, the median new single-family home sold for $417,400 in 2025. Those prices exclude many lower-income households from new supply.

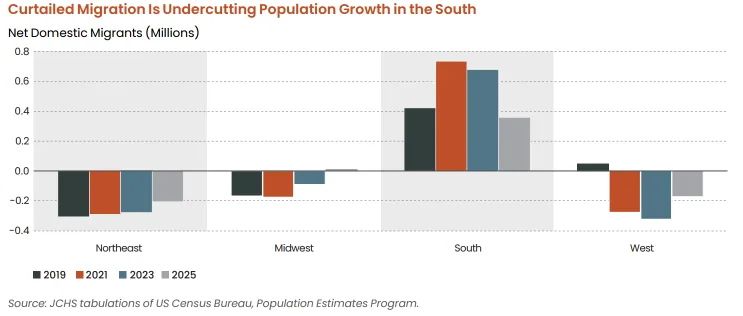

Midwest Sees Shift as Migration Slows

Migration patterns are shifting. Traditional Sun Belt magnets, including Texas and Florida, attracted fewer domestic movers in 2025. Meanwhile, the Midwest recorded net population gains for the first time in two decades.

Net international migration also dropped sharply. It fell by half in 2025. It could decline another 75% in 2026 to 321,000 people. That compares with an annual average near 900,000 from 2001 to 2019.

These trends are reshaping housing demand across major metros. They are also changing development patterns as builders respond to demographic shifts and uneven job growth.

Renter household growth reflects this volatility. It fell 61% between Q2 2025 and Q1 2026. Sun Belt markets with heavy deliveries, such as Austin and Phoenix, saw rents decline. Meanwhile, supply-constrained coastal markets reached new highs.

Developers are responding by expanding build-to-rent projects and smaller homes. They are focusing on regions attracting new households, including the Midwest and parts of the Southeast.

Why It Matters

Harvard’s report confirms a trend many CRE investors already see. Housing affordability keeps worsening despite better supply metrics.

In 2024, 49% of renter households, or 22.7M, were cost burdened. Another 26%, or 12.1M households, faced severe burdens. Among extremely low-income renters, 11M households compete for only 3.8M affordable units. Units renting for under $1,000 per month declined 30% over the last decade.

Homeownership has also become less attainable. The median existing home cost nearly five times median income in 2025. The typical monthly mortgage payment reached $2,420. That figure doubled from late 2020. Only 16% of renter households earned enough to buy a median-priced home.

Homeownership among adults under 35 fell from 39% in 2022 to 37% in 2025. Mobility across all age groups also approached record lows. National rents softened, and home prices eased slightly. However, the market remains deeply divided. Aggregate homeowner equity reached $34T, while renters and first-time buyers face growing barriers.

Federal assistance has not kept pace. Only 5.4M very low-income households received rental aid in 2023. Yet 19.1M households qualified. More than 8M households now face worst-case housing needs. Many renters also struggle to cover food, healthcare, and transportation after paying housing costs. Expiring affordability restrictions and aging public housing add further pressure.

What’s Next

Harvard’s JCHS argues local zoning reforms cannot solve the crisis alone. The report calls for broader federal action. Policymakers must expand subsidies, enforce fair housing rules, and address climate risks. They must also boost supply, especially for the lowest-income households.

Cities and states will likely test new zoning, financing, and social housing models. Still, Harvard says only federal action matches the scale of today’s affordability challenges. CRE professionals should watch federal funding, migration trends, and climate spending. These factors will shape multifamily, single-family rental, and for-sale housing markets nationwide.