- The commercial real estate recovery is intact in 2026, but volatility and shifting macro forces are widening performance gaps across sectors and geographies.

- Income growth, not cap rate compression, now drives total returns. Alpha increasingly depends on active property, market, and strategy selection—especially with persistent inflation and selective growth.

- Lending standards are loosening and transactions rising, but global economic and geopolitical risks leave little margin for error, making manager and sector choices crucial for outperforming benchmarks.

A Cycle Defined by Recovery—and Dispersion

Despite a tumultuous geopolitical backdrop and upward pressure on global yields, Principal Asset Management’s mid-2026 outlook, finds the CRE cycle still in recovery—though not equally for all segments. While private valuations are rising and transaction volumes rebounded in the first quarter, the recovery now manifests as decidedly K-shaped. REITs have moved from recovery to expansion, yet distress, while peaking, remains above pre-pandemic averages. Returns are positive for both US and European markets, but the pace, drivers, and risks of that recovery differ sharply across asset types and geographies.

The margin for error in the broader economy is narrowing. Resilient consumer demand and robust AI-driven capex are keeping GDP near potential in the US (2.1% projected for 2026 per Principal Real Estate), but new headwinds—from higher energy costs to unexpected rate hikes—are shifting sentiment and compounding investor selectivity.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Macro Forces Reshape the Playing Field

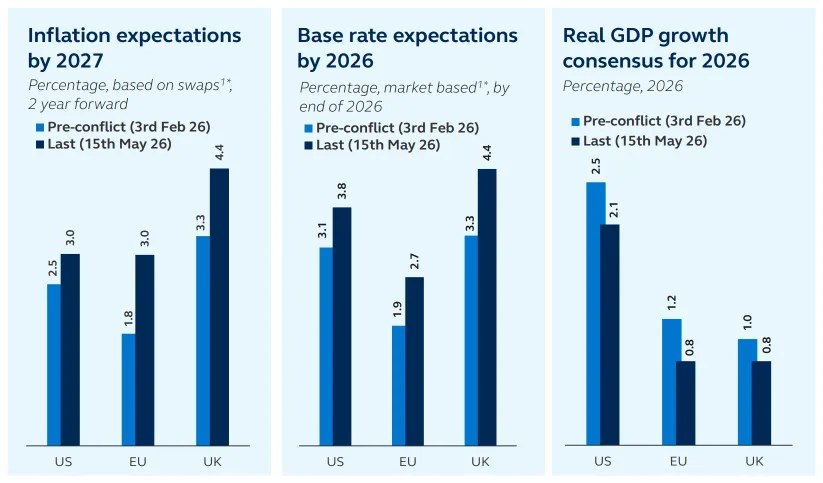

Global capital markets are moving out of sync. War in the Middle East has pressured commodity supply chains and triggered renewed inflation, especially in Europe, where price growth has exceeded central bank targets for three consecutive months. Global yield expectations have reversed, with swaps markets now pricing in more hawkish central banks in the US and abroad by late 2026. The US economy remains technically out of recession, but labor momentum has slowed and policy uncertainty is high. Meanwhile, regions like Spain, Poland, and Norway outpace laggards such as Germany and the UK.

Source: Bloomberg, Principal Real Estate, Q2 2026.

The result: persistent inflation is likely to persist into early 2027, and regional differences will be pronounced, particularly for petroleum importers. Investors are recalibrating for risk; deliberate allocation and constant strategy adjustments are quickly becoming the norm, not the exception.

K-Shaped Recovery and Where the Alpha Is

The post-pandemic CRE correction—one of only two of this magnitude in a generation per Principal Real Estate’s Q1 data—has paved the way for a materially de-risked but not monolithic asset class. Unlevered total returns rose +6.2% YOY in Europe and +5.0% in the US for Q1 2026, yet sector performance remains highly uneven. Senior housing and data centers are posting leading NOI growth (7.3% and 5.9% CAGR projected to 2030), while office and self-storage trail or stagnate. Regional disparities further magnify that dispersion, underscoring the need for selectivity in both sector and market plays.

Source: CoStar, PMA, Principal Real Estate, 1Q 2026.

Income growth has re-emerged as the principal driver of total returns. During the prior cycle, appreciation from cap rate compression dominated, but today, income accounted for 84% of total returns, up from 43%. As a result, CRE’s alpha relies less on broad market beta and more on selection and execution, as underscored by top-to-bottom quartile return spreads exceeding 5% in both the US and Europe. That widening gap mirrors recent trends, as return dispersion across property sectors has reached levels not seen in years.

Why It Matters

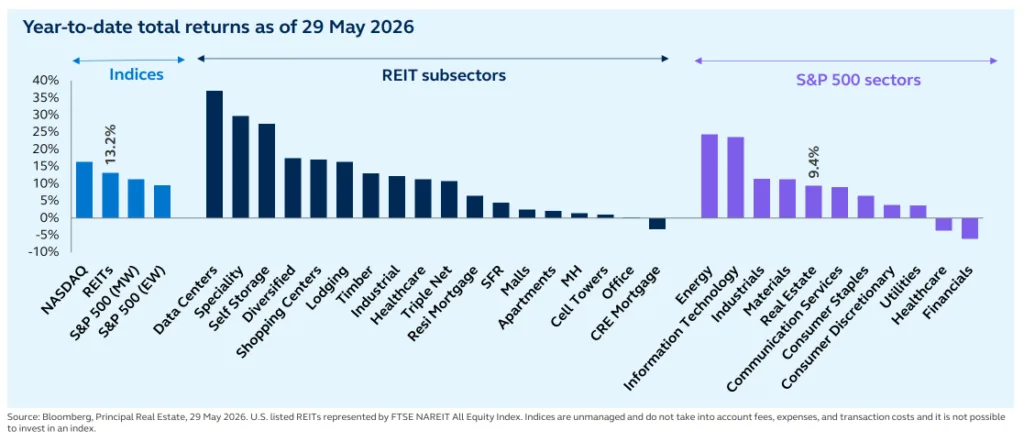

For allocators and operators alike, the CRE cycle is entering its expansion phase—but it is fragmenting. Transaction activity and lending standards have begun to loosen in developed markets: CMBS and private debt flows are projected to exceed last year’s levels, and senior loan officer surveys reveal more favorable lending terms relative to the peak of the cycle. US public REITs, per FTSE NAREIT data, are up 13% year-to-date and have now outperformed most S&P 500 sectors. Private equity, meanwhile, is attracting attention for both core and non-core vintages, while a prolonged distress unwind—distress just now rolling over after 15 quarters—signals further runway in selected market segments.

The cycle’s shape remains uneven. Value-add funds, opportunistic private equity, and select markets show the widest return spreads. They also offer skilled managers the greatest alpha potential. Principal Real Estate found that 10–20% REIT allocations improve Sharpe ratios. They also reduce volatility and add flexibility during rate swings. Meanwhile, private CRE debt offers lower volatility and strong risk-adjusted returns. Investors increasingly view it as a stabilizing force.

Data centers, rental housing, and necessity retail benefit from durable demand drivers. AI, demographics, and limited supply support those sectors. In contrast, office and discretionary retail remain vulnerable. The global opportunity set continues to expand, yet selecting winners grows harder. Investors will generate alpha through conviction in strategies, sectors, and partners.

What’s Next

Looking beyond mid-2026, volatility and macro uncertainty will remain defining market features. Private CRE capital should keep moving globally, favoring top-performing sectors and markets. Investors will generate alpha through property and market selection, manager diligence, and tactical allocations across public and private debt and equity.

Expect lending standards to loosen gradually and transaction volumes to rise. Performance gaps between top and bottom quartiles should also persist. Portfolio construction and active management will prove critical. Investors who adapt to shifting conditions should outperform as the cycle moves into full expansion.