- Top US tech office leases totaled 16.5M SF in the year through Q1 2026, with Silicon Valley and NYC leading activity, per Newmark.

- AI and adjacent firms accounted for nearly half of major expansions, pushing average deal size up 33% year-over-year.

- Premium, long-term leases dominate as tech tenants chase talent and amenities, elevating competition and rents in core markets.

Tech Leasing Consolidates in Core US Talent Hubs

The US tech sector’s approach to office leasing is no accident. According to Newmark’s analysis of the top 100 largest tech leases signed in the 12 months ending Q1 2026, technology occupiers are zeroing in on premium, established talent centers while scaling up their space commitments. Concentration is the key: just two cities—San Francisco Bay Area and New York City—captured the majority of the largest deals, with Silicon Valley eclipsing San Francisco itself in total square footage.

This consolidation signals a strategic shift, as tech occupiers leverage physical presence to lock in workforce advantages and future growth. Despite macroeconomic and geopolitical headwinds and limited new supply, firms are leaning into the office—especially where AI and venture investment density are strongest.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

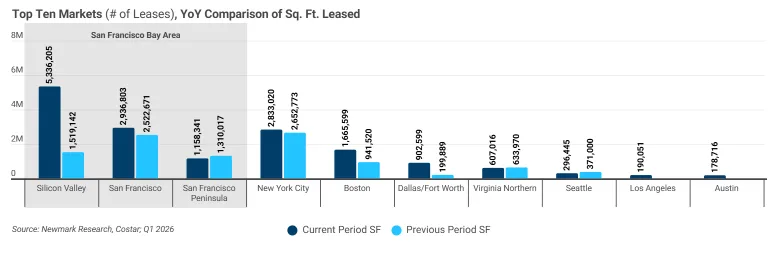

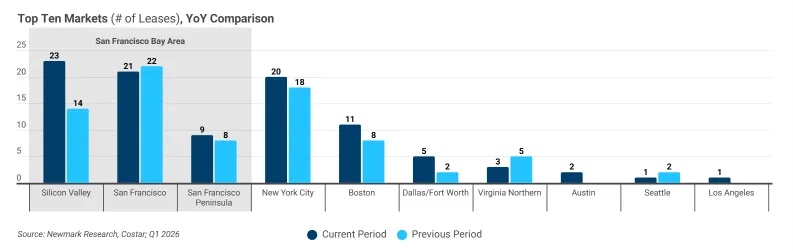

The top 100 leases collectively totaled 16.5M SF across 14 US markets, down from 21 markets in the previous period. The average lease size jumped 33% to 165,000 SF, the highest in recent memory, according to Newmark. Out of these, 53 deals were in the Bay Area and 20 in New York City, as AI-driven demand surged. Boston secured 11 leases, concentrated in robotics and defense tech. Overall, five markets took 85 of the 100 top leases, underlining both a deepening focus on talent hubs and limited expansion elsewhere.

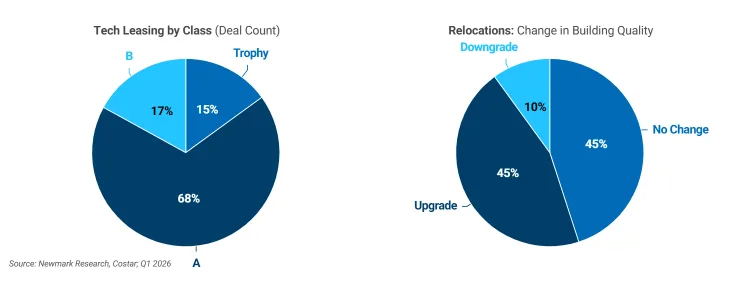

AI-native and infrastructure firms drove much of this growth. Notably, tenants like Anthropic increased their Bay Area footprint from 25,000 SF in 2021 to over 900,000 SF by this year. Renewals accounted for 38% of deals, while expansions made up 42%, and only 20% were relocations. Trophy and Class A assets comprised 83% of the total, reinforcing an industry-wide flight to quality.

AI Surge and the Flight to Quality Accelerate

The data points to a high but evolving concentration among tech leaseholders: just 10 firms took 43% of the top 100 leases, but newer entrants—especially AI firms like OpenAI and Anthropic—are moving up the ranks. Their rapid growth is reshaping major office markets. Among 78 deals that expanded footprints, 49 were tied to AI or AI-adjacent companies, showing just how decisively artificial intelligence is driving space demand in the sector.

The preference for quality space is stark. Class A and trophy properties drew 83% of leases and, per Newmark, nearly half of tenants who upgraded their space also expanded square footage. This preference mirrors a broader shift in office markets, where tenants increasingly favor newer buildings with stronger amenities and locations. With supply in premium buildings tightening and new construction lagging, occupiers are locking in prime spots and fueling rent spikes in core submarkets—especially for the most premium space.

Why It Matters

The shift toward concentrated, top-tier office leasing is more than a real estate story—it’s a tactic for winning talent and ensuring operational continuity. According to Newmark’s Q1 2026 office report, 78% of all US venture capital for AI went to Bay Area companies, making physical presence in these hubs even more valuable for tech occupiers. Expanding in established markets not only secures proximity to skilled labor and investment, but also builds stickiness that gives landlords pricing power and predictability.

Longer-term commitments are also back in vogue. Direct new deals averaged 120 months, renewals 101 months—both up substantially from 2019, even as tenants negotiate for greater flexibility. This supports larger tenant improvement allowances, which remain critical given rising buildout costs. The market’s ‘quality divide’ will likely widen as premium locations increasingly command a significant pricing premium and drive up competition among would-be anchor tenants.

Finally, tech’s expansion-first mindset—especially from high-growth AI firms—puts upward pressure on rent and limits leverage for tenants in the best-located space. With 60% of leases in urban cores and relocations rarely moving across urban-suburban lines, the established cluster pattern is self-reinforcing. These trends suggest that while macro headwinds persist, tech firms’ faith in the office as a competitive asset is only intensifying—especially for those at the AI frontier.

What’s Next

Expect competition for prime US office space in tech hubs to escalate as AI companies scale and the supply of trophy and Class A properties remains tight. The concentration dynamic is unlikely to reverse, especially since tenant geography and workforce patterns have proven sticky—offering landlords in top markets sustained pricing power. Watch for further expansion by AI-heavy hitters and ongoing quality flight, with the next wave of VC-fueled entrants likely to reinforce, rather than dilute, office demand in core US tech markets through 2026 and beyond.