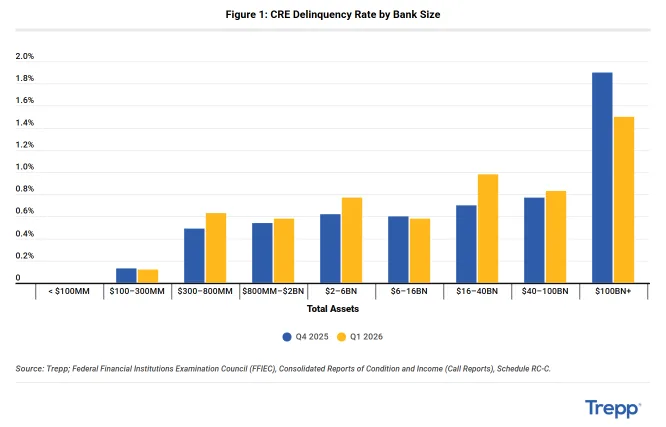

- CRE delinquency rates at US banks with $100B+ in assets fell from 1.9% to 1.5% in Q1 2026, per Q1 Call Reports.

- Regional and community banks saw modest increases in delinquency, particularly for banks with $16B–$40B in assets.

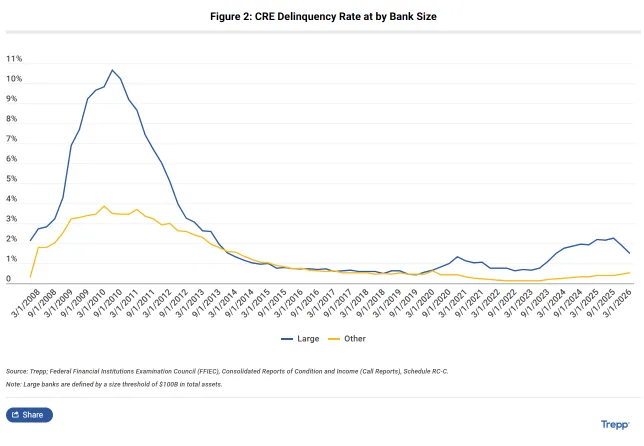

- The divergence echoes post-GFC trends, but this cycle appears less severe and more tied to loan portfolio composition.

Legacy Office Loan Resolutions Lead a New Cycle Phase

According to new Q1 2026 Call Report data, CRE delinquency rates diverged along familiar lines—only this time, the largest US banks are leading the improvement. Trepp notes that megabanks with over $100B in assets posted the only meaningful decline, while mid-tier and smaller institutions saw their delinquency rates edge higher. This marks the first clear inflection since the sector’s recent stress cycle gained traction, as legacy office loans get resolved at the top tier.

Context matters for CRE lenders in all asset categories. The largest banks historically carry less CRE as a share of their overall portfolio, but concentrated office exposures made them outliers for delinquency in recent quarters. Q1’s numbers show that as distressed office loans get restructured or sold, headline delinquency at these institutions drops quickly. For everyone else, rising rates and stubborn vacancies are combining for a slower, broader uptick in late payments.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The End of ‘Extend and Pretend’

The notable improvement among banks in the $100B+ assets category (from roughly 1.9% to 1.5% delinquency rates) can be traced to portfolio actions like loan workout, restructuring, or moving troubled assets off balance sheets. For most mid-sized and smaller banks—those with $16B–$40B in assets—the trend reversed, with delinquency rates ticking up. Buckets ranging from $300M to $6B in assets saw smaller, but still mostly positive, gains.

These moves aren’t seismic in absolute terms. Median delinquency rates for regional and community banks are still broadly within the post-GFC range, but the uptick is consistent enough to confirm a trend. A separate analysis found bank CRE delinquencies recently reached their highest level in a decade, underscoring how uneven stress remains across lenders. Researchers Glancy and Kurtzman (2024) found that roughly three-quarters of delinquency differentials between big and small banks can be explained by differences in loan size, property type, and geography. Smaller banks’ lower exposure to large, troubled office assets accounts for about half the gap on its own.

Divergence From the Global Financial Crisis

Comparing today’s delinquency trajectories to the GFC, another pattern emerges. Back then, the largest banks peaked above 10% delinquency, dragging the rest of the sector up with them to almost 4%. In the current episode, according to Call Report data, the largest banks never exceeded 2%, and regional/community banks have stayed below 1%.

The similarity is in the shape of the cycle: Larger institutions saw a sharper run-up and a quicker resolution. During the GFC, as the dust settled, delinquency rates across all bank sizes converged at lower levels. If history is any guide, this suggests today’s top-tier banks are largely past their moment of peak stress, while the rest may see a slower rise before things settle out.

Why It Matters

For CRE pros, these trends reveal which sectors and lenders face the toughest choices. Only the largest banks improved meaningfully, mainly by resolving legacy office loans. That points to targeted distress rather than a broad market problem. Portfolio mix also matters. A 2024 study by Glancy and Kurtzman found that office exposure, especially large urban assets, explains much of the delinquency gap between big and small banks.

Headline risks at megabanks are easing, which could limit forced sales and calm institutional lenders. However, mid-sized and community banks still face rising stress. Their smaller and more diverse portfolios may keep lending standards tight. Regulators also remain focused on CRE concentration, especially if rates stay high or property income weakens.

This downturn remains far smaller than the GFC. Call Report data shows top-tier delinquencies peaked at only one-fifth of 2009 levels. Sector-wide stress also remains limited. The recent improvement does not signal a crisis. Still, lenders will likely stay cautious through late 2026 and beyond.

What’s Next

The next few quarters will be critical. If past cycles hold, large banks may have already passed the worst. Delinquency rates could soon align with regional peers. The bigger question is how higher rates and weaker cash flow affect regional and community lenders. Many still hold outsized exposure to struggling property types.

Regulators will continue watching concentration risk. Yet delinquency rates outside the largest banks remain historically normal. CRE investors should monitor smaller bank portfolios. They may reveal whether stress worsens or follows past patterns by Q4 2026.