- Construction input costs rose 9.6% year over year in May, the fastest pace since the pandemic, per AGC and ABC data.

- Fuel, steel, and copper prices drove the increases, while contractor bid prices lagged behind cost escalation.

- The persistent cost pressure is squeezing margins and potentially impacting future project pipelines.

Post-Pandemic Inflation Hits Construction Input Costs

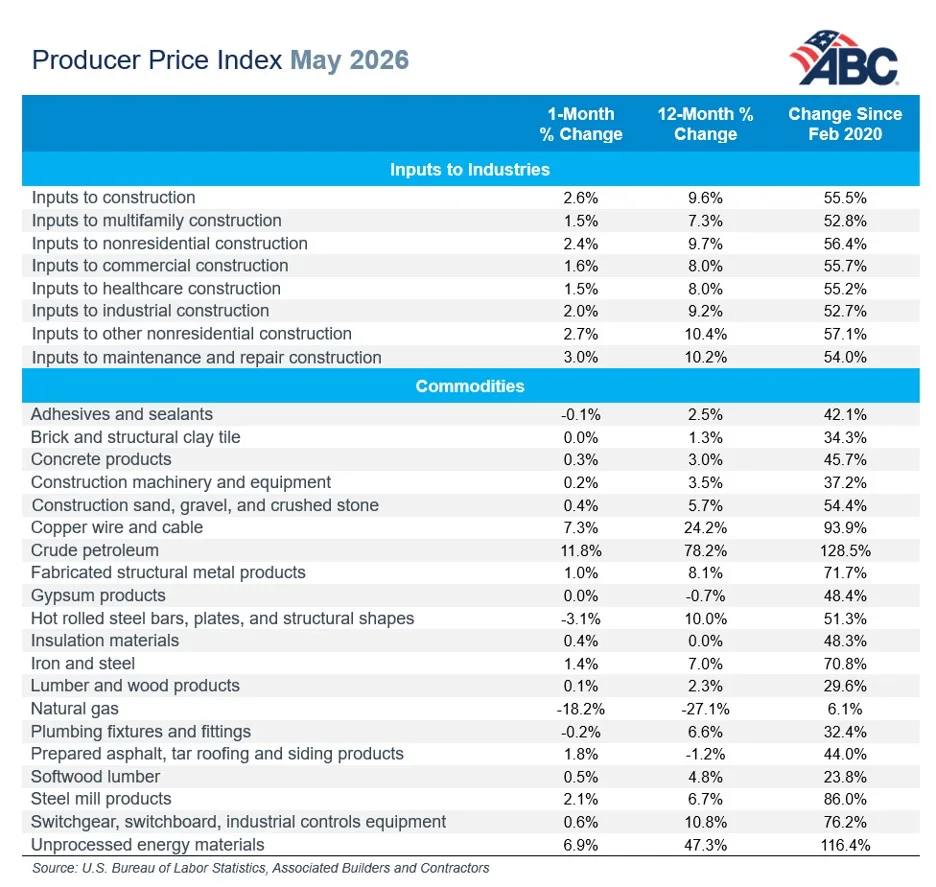

Construction input costs surged in May, with Associated General Contractors (AGC) and Associated Builders and Contractors (ABC) reporting the highest annual increase since the pandemic first disrupted supply chains. According to Multifamily Dive, the 9.6% year-over-year jump is double the growth rate of the broader US consumer price index, signaling a new round of inflationary pressure across the sector. The report shows that contractors are facing faster-rising input costs every month in 2026, a reversal from trends seen during the previous year, when costs had briefly stabilized.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Overall, construction materials prices climbed 2.6% month over month in May, bringing the annual gain to 9.6% compared to the previous May, according to ABC’s analysis of federal data. The cost escalation was most pronounced in fuel and metals, with copper wire and cable costs jumping 7.3% month over month and 24.2% year over year. Iron and steel prices increased 1.4% from April and are up 7% from last year. Rising oil prices—linked to geopolitical tension in Iran—also contributed to higher input costs. Despite higher expenses, contractors were unable to pass along equivalent increases to project owners, with bid price growth lagging behind input inflation.

Contractor Margins Squeezed by Materials Inflation

Builders are caught between rising input prices and slower growth in what they can charge, said AGC’s Ken Simonson. According to AGC, construction costs now rise more than twice as fast as overall consumer inflation. That trend had already surfaced in April, when construction materials costs jumped 6.2% and signaled renewed pressure.

Tariff-sensitive materials like steel and copper remain volatile amid global pressure and supply disruption. Since January, every month has brought cost increases, eroding contractors’ margin expectations. Economists said persistent input inflation and high borrowing costs could eventually weaken profitability. Still, contractors remain guardedly optimistic about medium-term performance.

Why It Matters

For CRE developers and general contractors, the rapid escalation in materials costs complicates budgeting and bidding for new projects. CBRE and other industry consultants note that volatility in inputs like steel, copper, and fuel tends to push up both direct construction costs and contingency reserves, especially on large commercial and infrastructure projects. According to the ABC, copper’s 24.2% annual leap reflects both global supply constraints and tariff pressures—an environment where price certainty is almost impossible to achieve. As Ken Simonson (AGC) notes, contractors are experiencing a “double whammy” where cost inflation outpaces compensation, compelling many firms to trim margins or delay commitments. With consumer inflation running at 4.2%, construction’s 9.6% input inflation signals unique vulnerabilities in the sector, especially for project types with long build cycles or heavy commodity exposure.

The current cost spike follows a brief period of relief in late 2025 that saw steel and lumber prices stabilize. But as geopolitical risks around oil markets resurfaced and tariffs remained in place, input costs rebounded sharply into 2026. Most economists agree that if input costs continue to rise faster than bid prices, contractors’ willingness and ability to take on new projects could diminish, potentially cooling construction activity later in the year.

What’s Next

Construction firms will likely face continued margin pressure through the second half of 2026 as materials inflation shows no sign of abating, per AGC and ABC. The consensus among economists is that further cost escalations—especially in metals and energy—may trigger more selective bidding and could reduce project starts, especially in highly competitive commercial sectors. Some contractors remain optimistic, hoping for relief in commodity markets or a pullback in borrowing costs, but many are bracing for tighter profit margins and more risk-sharing in contracts. For project owners, higher input costs may translate to costlier bids, longer timelines, and greater pricing uncertainty heading into 2027.