- Cushman & Wakefield found that 16 of 35 major US industrial markets shifted toward more neutral or landlord-favorable conditions in 2026.

- Vacancy appears to be stabilizing as absorption improves, with annual absorption up 35% and quarterly leasing topping 170M SF for the fourth straight quarter, according to Cushman & Wakefield.

- The improving outlook contrasts with weaker global industrial fundamentals and suggests US landlords may regain pricing power sooner than many occupiers expected.

The US industrial market is showing signs of a gradual recovery after several quarters of supply-driven softness. According to Bisnow, market conditions are beginning to tilt back toward landlords as developers work through the wave of logistics space delivered during and after the pandemic boom. The shift comes even as trade disruptions, geopolitical tensions, and tariff uncertainty continue to weigh on occupier decision-making.

A changing balance of power

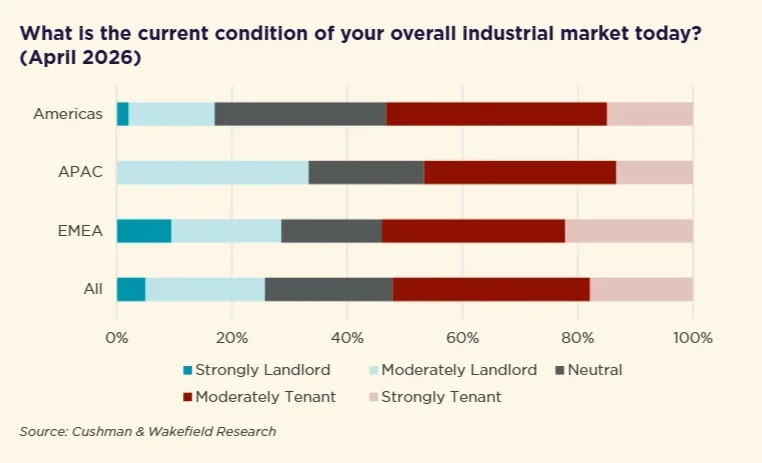

Cushman & Wakefield found that 16 of the 35 major U.S. industrial markets it tracks shifted market conditions over the past year. Most moved away from tenant-friendly territory and toward either balanced conditions or environments that increasingly favor landlords. The change marks a notable reversal from the past several years, when a surge of new supply gave occupiers greater negotiating leverage across many logistics markets.

The report also highlights a widening gap between the US and global industrial sectors. While American markets are trending toward landlord-friendly conditions, many international markets continue to favor tenants as economic uncertainty dampens demand.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The details

Stronger absorption and stabilizing vacancy rates are driving the improving outlook.

Cushman & Wakefield reported that US industrial vacancy fell by 10 basis points during the first quarter of 2026 after reaching a late-2025 high of 7.0%.

Demand metrics are also strengthening. Total absorption rose 35% year over year during the 12 months ending in March 2026. First-quarter leasing activity topped 170M SF for the fourth consecutive quarter.

Rent growth is expected to follow. Cushman & Wakefield projects rents will increase in 55% of markets across the Americas, including major logistics hubs such as the Inland Empire and Atlanta. Vacancy in the Inland Empire reached 7.8% in Q1 2026, yet landlords there are still expected to regain pricing momentum as supply pressures ease.

A global market moving the other direction

The US recovery stands out against a softer international backdrop. Cushman & Wakefield’s survey of 135 industrial markets worldwide found that only 8% are currently shifting toward landlord-favorable conditions. Meanwhile, 23% are moving further toward tenants and another 13% are becoming more balanced.

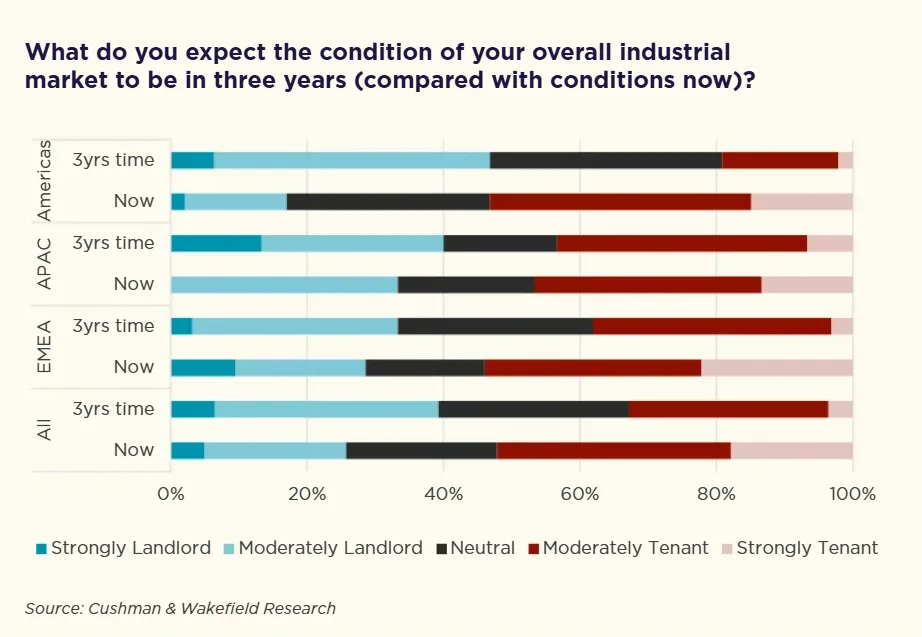

Today, 52% of global industrial markets favor tenants, according to the 2026 report. However, that dynamic may not last. Cushman & Wakefield forecasts that by 2029 only one-third of global markets will remain tenant-favorable, suggesting the current softness may represent a cyclical pause rather than a structural shift.

The Americas are expected to lead that recovery. The share of landlord-favorable markets across the region is projected to rise from 17% today to 46% within the next three years.

Why it matters

Industrial real estate has spent the past two years digesting one of the largest construction waves in modern logistics history. For landlords, the latest data suggests the sector may be moving beyond its correction phase and back toward a more balanced supply-demand environment.

That shift matters because industrial remains one of the largest and most institutionally owned property sectors in the US As vacancy stabilizes and rent growth returns, owners could see stronger operating performance and improved pricing leverage. At the same time, tenants may find fewer opportunities to secure the aggressive concessions that became common during the recent softening cycle.

The recovery is not without risks. More than 60% of US respondents surveyed by Cushman & Wakefield said tariffs or the threat of tariffs have delayed leasing decisions, while more than half cited geopolitical events and rising energy costs as factors influencing real estate strategy.

What’s next

The key question for the remainder of 2026 is whether demand can continue outpacing new supply deliveries. Cushman & Wakefield expects vacancy to decline further throughout the year, a trend that would strengthen landlords’ negotiating position and support additional rent growth.

Investors and operators will also be watching trade policy closely. While logistics demand remains healthy, prolonged tariff uncertainty or escalating geopolitical disruptions could slow leasing velocity and delay expansion plans. For now, however, the industrial sector appears to be emerging from its cyclical trough with stronger fundamentals than many global counterparts.