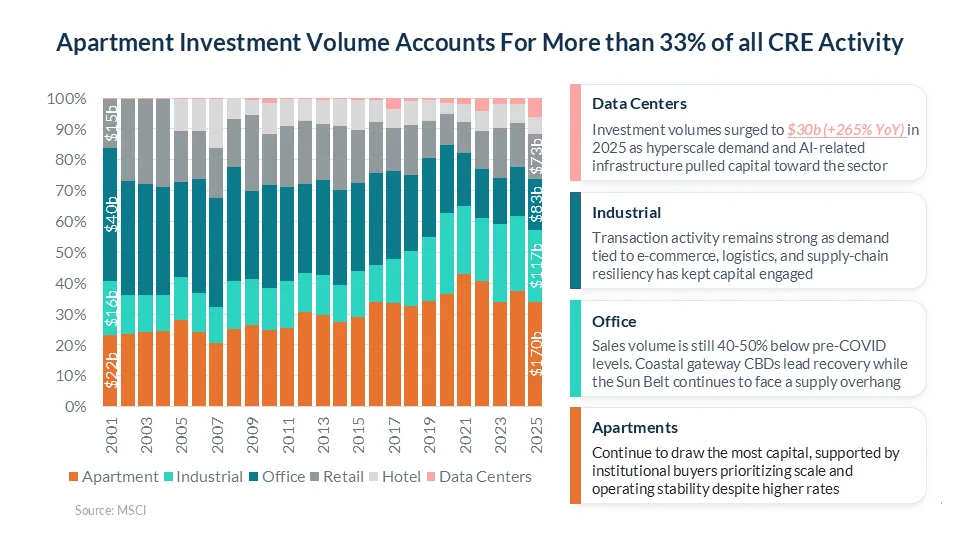

- Multifamily investment soared to $170B in 2025, now representing over a third of total US CRE transaction volume.

- Institutional capital remains focused on apartments, even as sectors like data centers and industrial attract fresh inflows.

- Capital flows reveal shifting appetites, with Sun Belt and select urban markets outperforming while others face supply headwinds.

Multifamily Outpaces the Field as Capital Flows Shift

US multifamily has cemented itself as the most resilient major CRE sector, according to RealPage Analytics. Annual investment volume surged from $22B in 2001 to about $170B in 2025. This jump has pushed apartments from roughly 25% of total commercial real estate activity to more than 33% nationwide, reflecting the sector’s growing dominance even through disruptive cycles like the Global Financial Crisis and 2020’s market upheaval.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Other Property Types See Mixed Results

Industrial assets have gained significant ground, hitting $117B in 2025 as e-commerce and supply chain realignment reshape demand. Data centers, once a niche, now draw increasing allocations fueled by demand for AI and hyperscale infrastructure. By contrast, office investment remains severely depressed — at 40% to 50% below pre-pandemic levels — highlighting persistent uncertainty over long-term workspace requirements, per RealPage Analytics’ recent data.

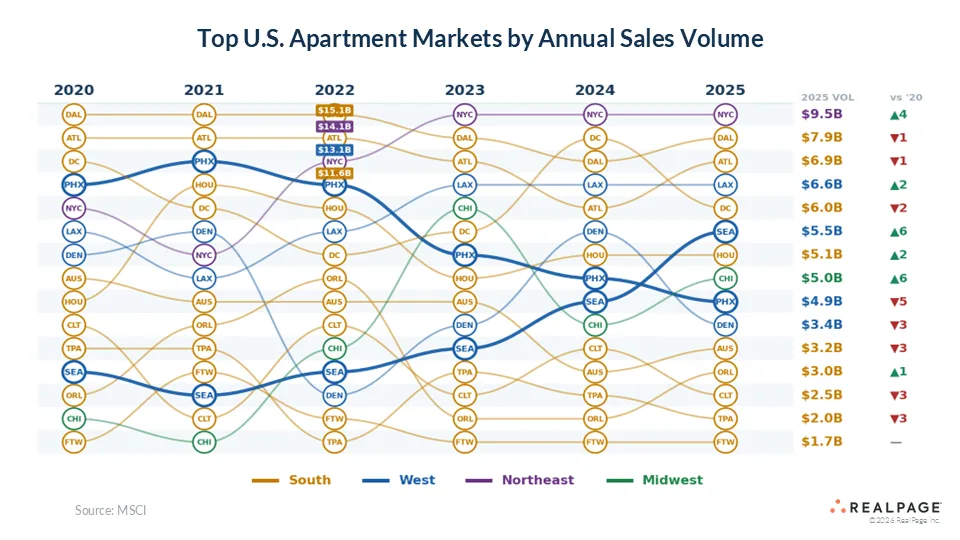

Sun Belt Remains a Magnet, but Recent Winners Shift

Sun Belt markets still attract apartment investors. Nine of the top 15 markets are in the region. Population growth and migration continue to support demand.

However, performance varies across markets. Phoenix saw annual transaction volume fall from over $10B to under $5B. New supply has reduced investor demand. Meanwhile, Seattle rebounded to $5.5B in annual volume. The recovery signals renewed institutional interest. Denver and Chicago highlight the market’s volatility. Both cities have moved up and down the rankings. Inventory levels and local fundamentals continue to drive those shifts.

Why It Matters

Apartments remain resilient despite growing interest in data centers and logistics assets. Strong housing demand and steady rent growth continue to attract capital. Occupancy recently climbed above 95%, reinforcing confidence in the sector’s income stability and long-term fundamentals. Moreover, multifamily remains a preferred allocation for institutional investors. Office and retail sectors still face cyclical and structural challenges. According to RealPage Analytics, investors are becoming more selective. They are focusing on sectors and markets with proven long-term demand drivers.

What’s Next

Investors should watch for continued bifurcation within CRE, as sectors aligned with demographic growth and stable income streams (like Sun Belt multifamily) sustain interest while more cyclical and underperforming markets see reduced transaction activity. With total capital flows still robust but increasingly targeted, expect sharper disparities in asset pricing and liquidity across the next cycle, especially as new-economy sectors evolve and compete for allocation.