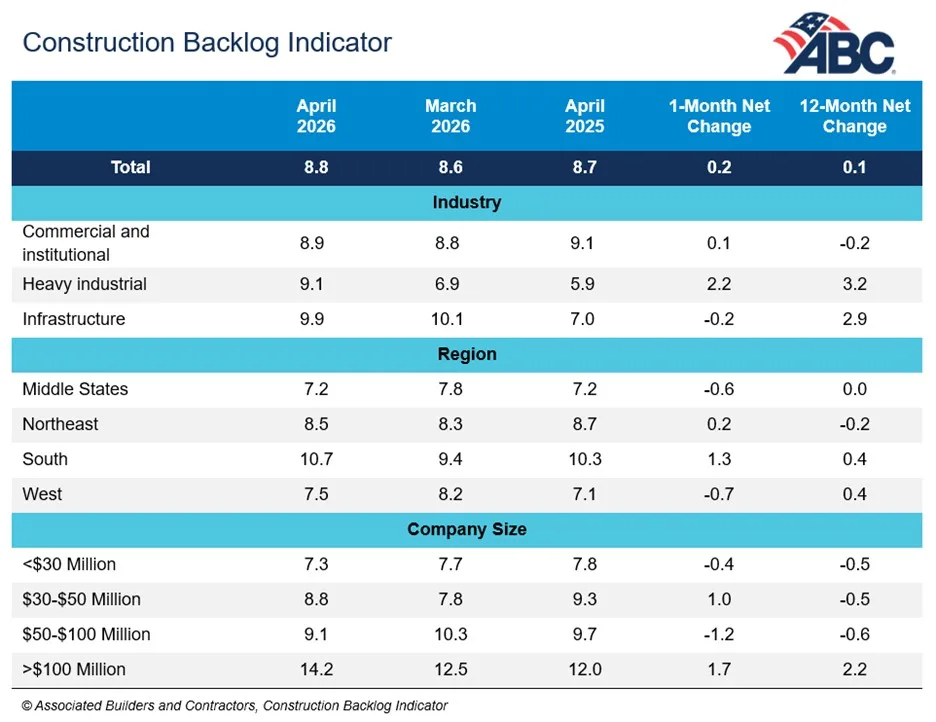

- ABC’s Construction Backlog Indicator rose to 8.8 months in April, marking the highest reading in 10 months as data center projects drove demand.

- Contractors with more than $100M in annual revenue posted significantly stronger backlog growth, with 42% tied to data center work versus just 7% of smaller contractors.

- The widening gap highlights how AI and cloud infrastructure spending is reshaping construction activity and concentrating opportunity among larger firms.

Contractor backlog climbed again in April as data center construction continued to dominate the nonresidential building pipeline. According to Associated Builders and Contractors’ May 2026 Construction Backlog Indicator report, backlog rose to 8.8 months, up 0.2 months from March and slightly above April 2025 levels.

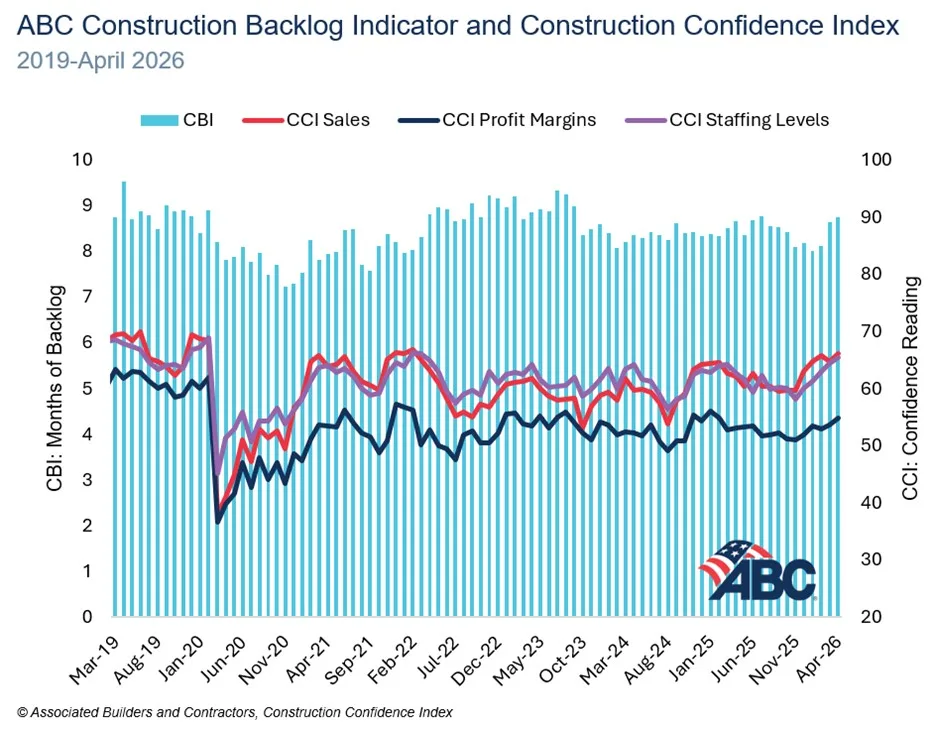

The gains came despite softer construction spending data and growing concerns around material costs and fuel prices. ABC’s Construction Confidence Index also improved across sales, staffing, and profit margin expectations, signaling that contractors still expect growth through the second half of 2026.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Data Centers Widen the Contractor Divide

The strongest gains remain concentrated among the industry’s largest firms. Contractors generating more than $100M in annual revenue reported backlog growth that was 2.2 months higher than a year earlier, while smaller contractor categories posted year-over-year declines.

According to ABC Chief Economist Anirban Basu, the surge is closely tied to the ongoing data center construction wave. ABC found that 42% of contractors with more than $100M in annual revenue are currently working on data center projects, compared to just 7% of firms below that threshold.

The backlog gap is even more pronounced when comparing firms directly exposed to data center work. Contractors with active data center contracts reported an average backlog of 12.2 months, versus 8.3 months for those without exposure to the sector.

The Details

ABC collected survey data between April 20 and May 4, capturing contractor sentiment during a period of elevated uncertainty around tariffs, energy prices, and broader economic growth. Even so, confidence metrics improved across the board.

ABC’s Construction Confidence Index readings for sales, staffing, and profit margins all remained above 50, the threshold indicating expected expansion over the next six months. Just 20% of contractors expect profit margins to shrink during that period, the lowest share since January 2025.

The results suggest contractors believe project demand will remain resilient even as financing costs and operating expenses stay elevated. The data also reinforces how hyperscale data center development continues to outpace most other commercial property sectors.

AI Infrastructure Reshapes Construction Demand

The construction industry’s growing dependence on data center work mirrors broader capital flows across commercial real estate. Cloud computing, AI adoption, and digital infrastructure investment have triggered a multiyear expansion cycle for hyperscale campuses nationwide. That surge is also intensifying demand for electricians, HVAC specialists, and other skilled trades as contractors race to staff increasingly complex data center projects.

Major tech companies including Amazon, Microsoft, Google, and Meta continue to ramp up spending on AI infrastructure, creating sustained demand for specialized contractors, power systems, and industrial-scale construction capabilities. According to CBRE’s 2025 North America Data Center Trends report, vacancy rates across primary data center markets remain near record lows as supply struggles to keep pace with demand.

That demand is increasingly favoring larger contractors with the scale, labor force, and technical expertise needed to execute complex power-intensive projects. Smaller contractors, meanwhile, appear to be missing out on one of the industry’s fastest-growing segments.

Why It Matters

The latest backlog figures underscore how uneven the current construction cycle has become. While headline backlog numbers appear healthy, much of the growth is concentrated in a narrow slice of the market tied to AI and digital infrastructure.

That concentration could create broader risks for the industry if data center spending slows or becomes oversupplied. At the same time, firms positioned within the sector are benefiting from unusually long pipelines and stronger pricing power compared to peers focused on traditional office, retail, or multifamily work.

The divergence also highlights how access to large-scale institutional projects increasingly determines contractor performance in today’s market.

What’s Next

Contractors will be watching whether data center development continues to offset weakness in other construction categories through the rest of 2026. Rising material prices, grid constraints, and labor shortages could still pressure margins even as demand remains elevated.

For now, ABC’s data suggests the industry’s optimism remains intact, particularly among firms tied to hyperscale and AI-driven development. If tech companies maintain current infrastructure spending levels, data centers are likely to remain one of commercial construction’s strongest demand drivers heading into 2027.