- Industrial vacancy rates reached 9.7% in November 2025, up 220 bps year-over-year.

- National average rents grew 5.7% to $8.76 PSF, while lease spreads narrowed.

- Year-to-date industrial sales hit $68.4B, with Phoenix and Dallas leading transactions.

- Data centers and niche assets saw record investor interest alongside manufacturing growth.

Transitional Year for the Industrial Report

The CommercialCafe reports that the 2025 industrial report highlights a year of transition driven by persistent oversupply and significant changes in trade policy. Despite a historic influx of new inventory, the market experienced moderating rent growth and rising vacancy rates. Notably, sectors like manufacturing and data centers continued to expand, buoyed by evolving technology, automation, and reshoring trends.

While investors and occupiers adapted to shifting policy and economic uncertainty, formerly niche industrial assets such as outdoor storage began drawing attention amid efforts to optimize supply chains.

Impact of Supply Surge and Trade Policy

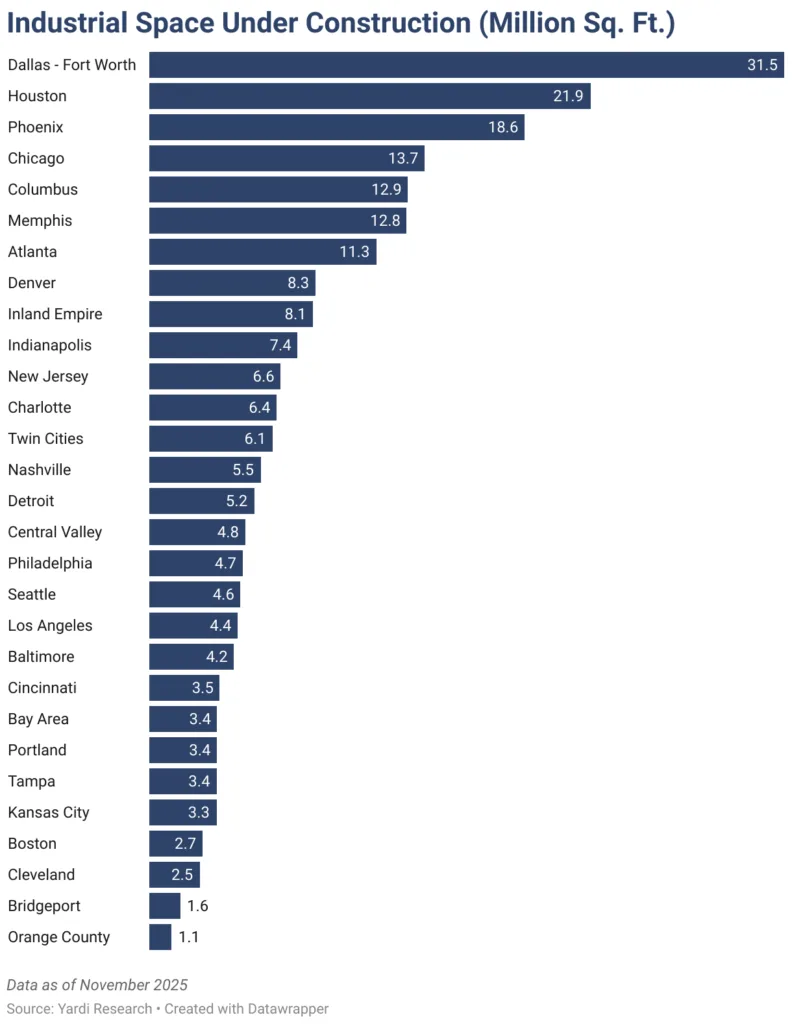

The industrial report points to a supply glut as the primary factor behind higher vacancies across most regions. From 2020 to 2024, more than 2.5B KSF of industrial space was built nationwide, leading to an average vacancy rate of 9.7% by late 2025. Construction volume in 2025 reached nearly 383M KSF underway, with 265.7M KSF completed year-to-date.

Trade policy volatility—marked by new tariffs and the elimination of some green tax credits—added further uncertainty, slowing lease decisions as companies waited for clarity. These disruptions continued to ripple through development pipelines and leasing strategies, as shifting trade dynamics altered project feasibility in key logistics hubs. Despite these challenges, manufacturing activity held steady, supported by efforts to build supply chain resilience and accommodate higher production costs through automation and reshoring.

Rents, Occupancy, and Market Divides

National in-place industrial rents averaged $8.76 PSF, a 5.7% year-over-year increase. Higher rent growth was observed in Atlanta (9.7%) and Miami (8.6%). The spread between new leases and in-place rents narrowed to $1.31 PSF, down from $2.14 PSF a year earlier. Vacancy rates grew in most regions but remained tightest in the Midwest—Kansas City held vacancies near 5%, while Bridgeport, Conn., posted 5.5%.

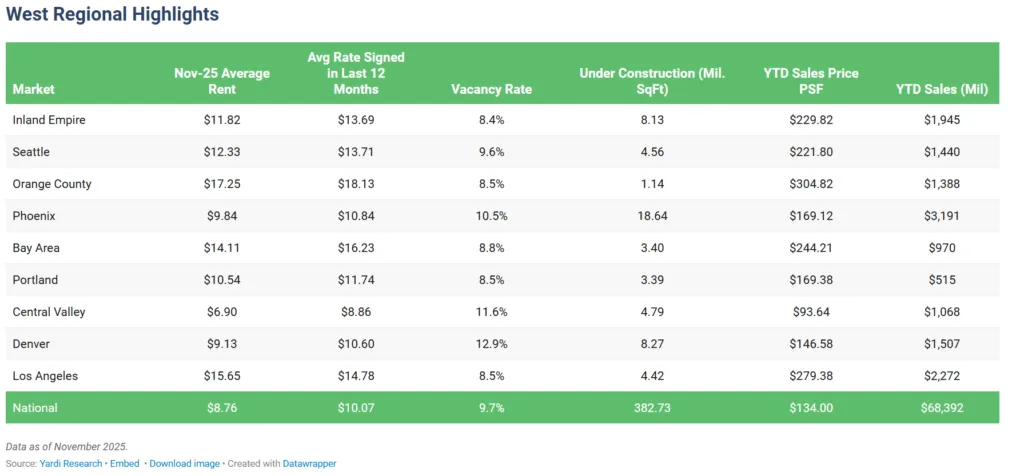

Houston remained resilient with 5.5% rent growth, a 6.2% vacancy rate, and significant port-driven demand despite recent heavy deliveries. Western markets showed softening rents and lease spreads, especially in Southern California and Phoenix, contributing to more tenant-favorable conditions.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Regional Performance and Investment Trends

According to the industrial report, Dallas-Fort Worth saw the nation’s highest year-to-date sale volume at $5.6B, while Phoenix retained strong investment appetite despite record construction and softening rents. Western US markets—including Seattle and Los Angeles—recorded declining sales prices and elevated vacancy rates. In the Midwest, affordability drove construction rebounds in Chicago and Columbus.

Southern markets like Atlanta led in rent growth, while Charlotte and Memphis faced widening vacancies and subdued lease premiums. In the Northeast, new lease spreads remained elevated in Boston and Bridgeport, reflecting continued supply-demand imbalance, despite limited construction.

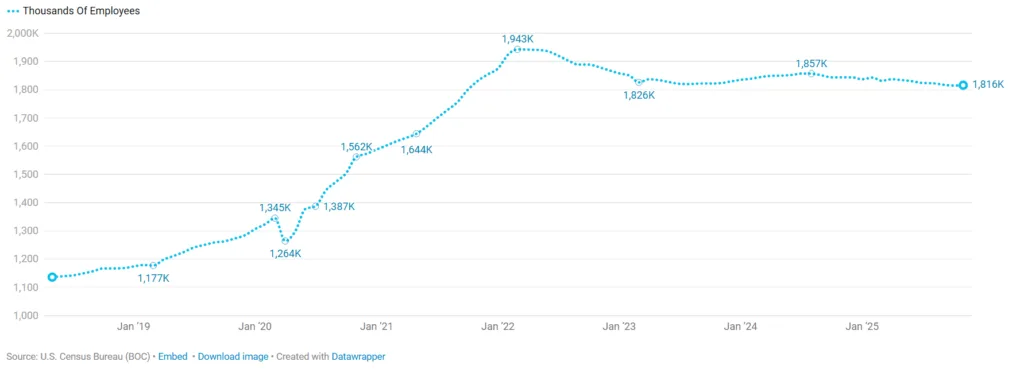

Labor Market and Sector Outlook

Warehouse and storage sector employment declined 1.5% year-over-year, marking a four-year low. Continued adoption of automation and robotics contributed to this trend, even as core retail sales and exports rose.

The industrial report concludes that supply surges and shifting policy created uncertainty in 2025. Still, strong fundamentals in data centers, manufacturing, and logistics continue to attract investor interest. Looking ahead, moderation and flexibility will remain key as markets absorb new supply and adapt to changing demand drivers.