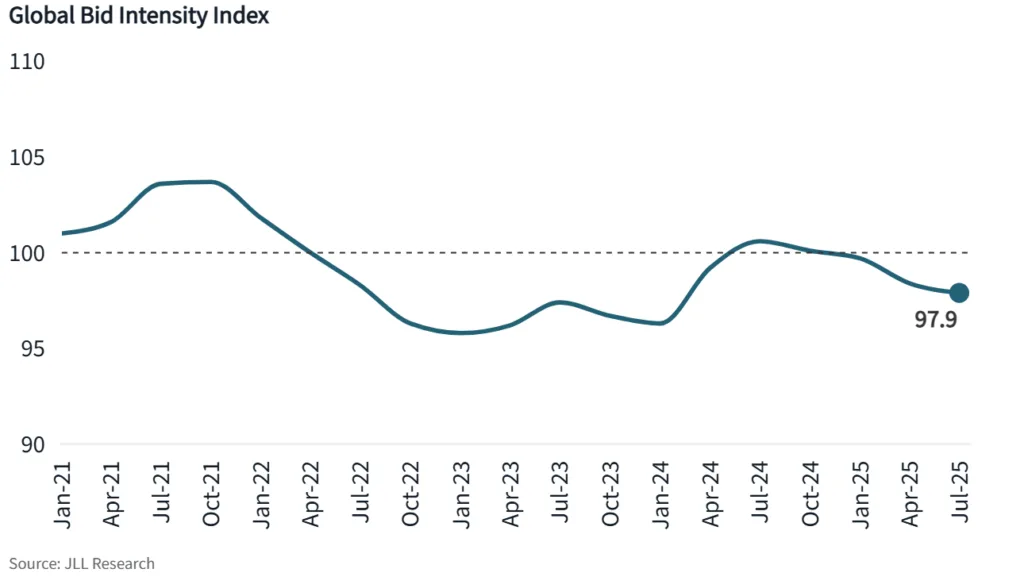

- JLL’s Global Bid Intensity Index, based on proprietary bid data, improved in July 2025 for the first time since late 2024.

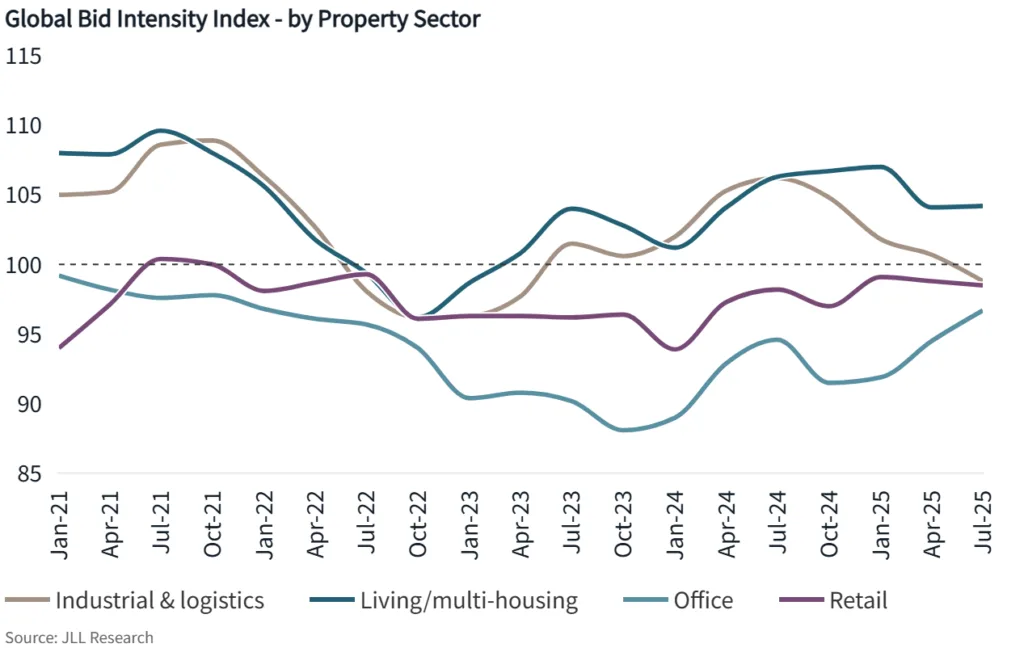

- Living and multi-housing lead all sectors in competitiveness, while retail and office are gaining strength.

- Industrial and logistics face weaker demand as supply chain concerns weigh on investors.

- Strong lending conditions and a shift toward “risk-on” strategies should drive more capital into real estate this year.

A Turning Point for Bidding Activity

JLL’s Global Bid Intensity Index peaked in late summer 2024 when investors expected interest rate cuts. In early 2025, volatility in bond markets and trade uncertainty hurt investor confidence.

By July 2025, the index posted its first month-over-month increase since December 2024. That rise signals that investor appetite is returning and bidding activity is becoming more competitive.

Sector-Specific Dynamics

- Living / Multi-Housing: Remains the strongest sector. Housing shortages and abundant investor capital keep bidding fierce.

- Industrial & Logistics: Trails other sectors as slowing leasing and supply chain issues reduce momentum.

- Retail: Shows steady recovery. Balanced supply and demand, along with resilient consumer spending, strengthen bidding.

- Office: Attracts more bidders and lenders than earlier this year, lifting sentiment and deal activity.

Capital Flows Outlook

The future path of JLL’s Bid Intensity Index depends on the economy, global trade, and political risks. Still, investors are shifting toward “risk-on” strategies. Paired with strong lending conditions, this shift points to more capital entering the market through the rest of 2025.

Why It Matters

The Bid Intensity Index acts as an early signal of capital market trends. It often shows where momentum is building before transaction volumes confirm the shift.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes