- US single-family median rents fell 1.6% year over year in H1 2026, the first major national decline since the pandemic boom.

- Nearly half of analyzed markets saw rents drop, with Sun Belt and large cities suffering most while Bay Area tech hubs posted growth.

- Increasing rental supply, elevated vacancy, and widespread concessions are keeping pricing power with renters, especially in high-growth markets.

Supply Glut Outpaces Historical Spring Boost

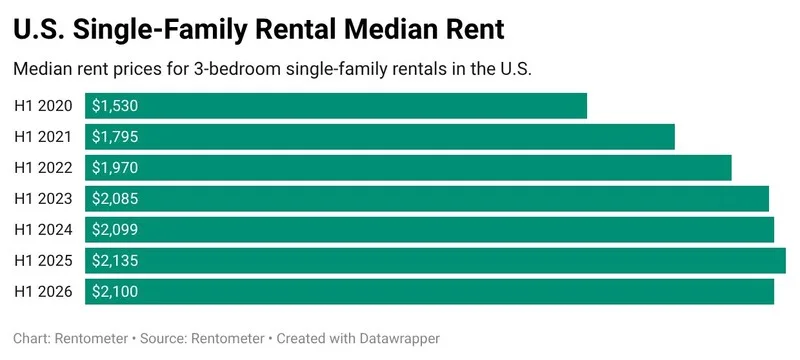

US single-family rental (SFR) markets cooled sharply in the first half of 2026, per Rentometer’s mid-year report. The national median asking rent for 3-bedroom SFRs landed at $2,100, down 1.6% from H1 2025—a reversal from the 1.7% increase recorded a year prior.

For the first time since the post-pandemic boom, the spring and early summer leasing season failed to spark rent growth, with median rents flat between Q1 and Q2. This stagnation reflects broader changes: an abundance of rental supply from new apartments, build-to-rent (BTR) communities, and ‘accidental landlords’ converting homes to rentals is eroding typical landlord leverage during peak leasing periods.

For a sector that houses 41% of US renters, these dynamics signal a recalibrated pricing environment after several years of surging growth.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Rentometer tracks more than 10M new rental records each year across 1,099 US cities. In H1 2026, 49% of local SFR markets posted year-over-year rent declines. Only 37% recorded rent growth of at least 1%.

Larger cities posted the weakest results. About 67% of metros with more than 250,000 residents saw rents decline. That compares with 58% of mid-sized cities and 61% of small towns.

Regionally, the Pacific led declines with rents down 3.2%. The Southeast followed with a 2.9% drop. Meanwhile, the Midwest and Northeast remained flat.

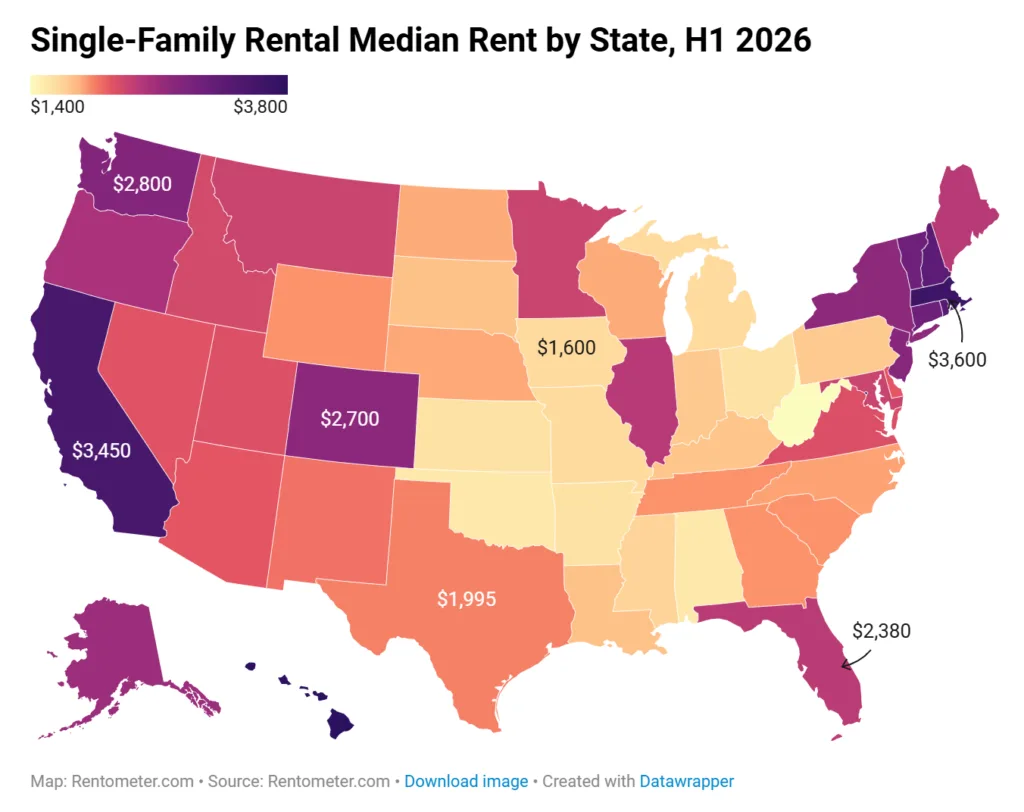

California continued to dominate high-end rent rankings. San Francisco’s median single-family rent reached $5,280. That figure stood more than four times higher than Toledo, Ohio, at $1,248.

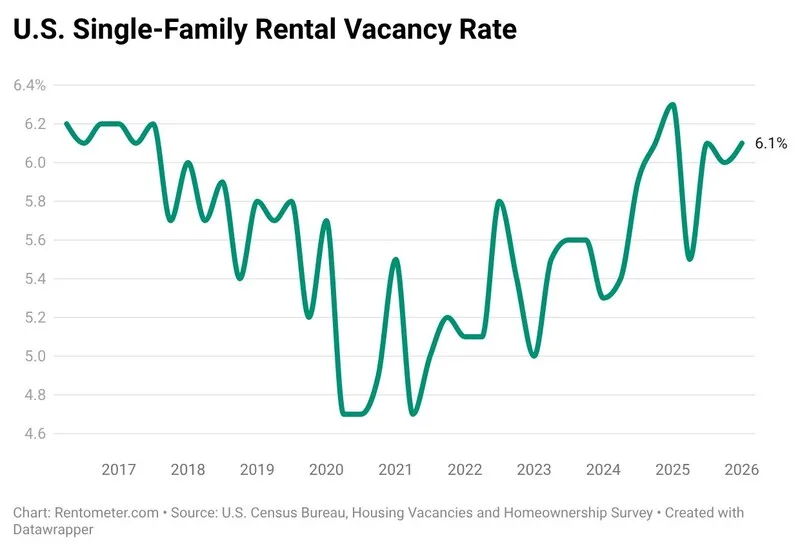

Vacancy rates also moved higher nationwide. The all-rental vacancy rate reached 7.3% in Q1 2026, the highest level since 2017. SFR vacancy climbed to 6.1%.

Concessions and Competitive Pressures Reshape Pricing

Rising supply and aggressive incentives continue to shift pricing power toward renters. RealPage found that 16.9% of US apartment units offered concessions in April 2026.

Zillow reported that nearly 40% of listings featured discounts. That marked the highest level in more than a decade. These incentives targeted both multifamily and SFR renters.

Build-to-rent communities also leaned on free rent offers and discounted move-in packages to accelerate lease-ups. Meanwhile, accidental landlords added more inventory to the market.

These owners often turned to renting after failing to sell their homes. Zillow reported that 2.3% of its SFR listings had recently been for sale.

John Burns Research & Consulting reported slower growth in new SFR listings across select portfolios. Still, oversupply in multifamily housing and pressure in for-sale markets continue to weigh on rents.

As a result, landlords in most markets struggle to raise rents. The pressure remains strongest in markets facing heavy new competition.

Why It Matters

The 1.6% national rent decline marks a major shift for SFR investors and operators. Many had grown accustomed to years of strong rent growth.

Sun Belt markets that led the pandemic boom now face reversals. Miami, Tampa, Phoenix, Nashville, and Dallas all recorded rent declines of 2% or more.

Overbuilding and rapid BTR expansion flooded many Southeast markets with supply. Tenants can now negotiate concessions or compare more options.

At the same time, high mortgage rates continue to limit home sales. That dynamic keeps accidental landlords in the rental market and SFR inventory elevated. Many homes also remain on the market longer before finding buyers, further extending their time in rental pools and adding pressure on asking rents.

Colliers reported that concession spending reached a record $129 per unit in Q1 2026. Yet only one-quarter of listings needed incentives, showing discounts remain targeted rather than universal.

In contrast, Bay Area markets continue to outperform. San Francisco and San Jose posted SFR rent growth of 5.7% and 5.9% in H1.

AI-driven job growth and limited housing supply continue to support demand. Sunnyvale led gains with rents up 11.1%, while Berkeley rose 10%.

Several Peninsula markets also recorded strong performance. However, nearby East Bay cities moved in the opposite direction. Oakland and San Leandro both posted rent declines of 4.4%.

These results highlight the increasingly local nature of rental performance. National trends no longer tell the full story.

Across 41 states, most tracked markets posted flat or declining rents. Colorado, Alabama, Kansas, and Louisiana showed the broadest weakness. At least 80% of cities in those states failed to post rent gains.

This growing divergence makes local expertise increasingly valuable. SFR investors also need greater operational flexibility in today’s market.

What’s Next

Supply pressures are unlikely to ease quickly, even as some large landlords report fewer new listings. Rentometer found no rebound in median asking rents between Q1 and Q2 2026.

That trend suggests landlords may struggle to regain pricing power through year-end. Improvements in the resale market could eventually reduce the number of accidental landlords.

However, apartment completions and concession activity will likely keep rent growth constrained. Most regions still face significant supply pressure.

Operators in supply-constrained or tech-focused markets may continue to raise rents. The Bay Area remains the clearest example.

Elsewhere, competition will likely stay intense. Tenant-friendly conditions should persist through late 2026.