- US CLO issuance reached $126.5B across 285 deals in Q2, with activity rebounding sharply after April’s slowdown.

- Tighter AAA spreads supported stronger new issuance and refinancing activity in both the US and Europe, according to Trepp and KopenTech.

- The quarter suggests CLO markets remain resilient despite geopolitical volatility, with credit fundamentals continuing to support issuance.

Commercial real estate credit markets regained momentum during the second quarter as the US CLO market rebounded from a cautious April, per Trepp.

Issuance accelerated through May and June as AAA spreads tightened and investor confidence improved. Europe followed a similar path, with new issuance overtaking refinancing and reset activity for the first time this year, signaling stronger demand for fresh transactions.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Geopolitical Volatility Tested Credit Markets

April’s slowdown reflected broader uncertainty across leveraged finance markets as geopolitical tensions and policy headlines weighed on investor sentiment. That caution proved temporary. As volatility eased, issuers returned to the market and financing conditions improved. According to Trepp and KopenTech, the recovery highlighted the CLO market’s ability to withstand external shocks without a meaningful deterioration in underlying credit conditions. Instead of credit quality, macro headlines became the primary driver of quarterly issuance patterns.

The Details

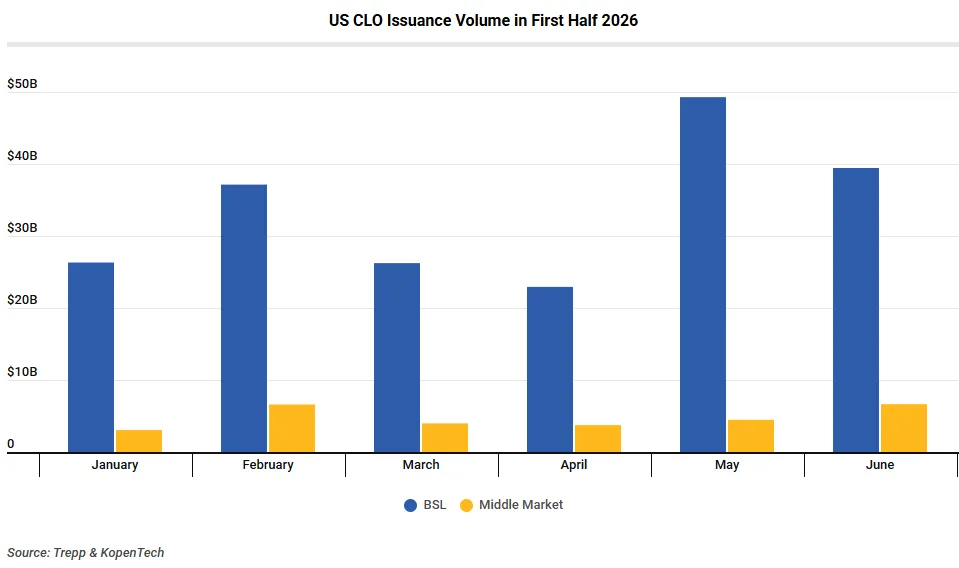

The US CLO market generated $126.5B of issuance across 285 transactions during the second quarter, according to Trepp and KopenTech. Broadly syndicated loan (BSL) CLOs accounted for $111.7B, while middle-market CLO issuance totaled $14.9B.

Issuance built steadily throughout the quarter. April produced $26.7B across 64 deals before activity accelerated to $53.8B across 119 transactions in May, the strongest month of the quarter. June followed with another healthy $46.1B across 102 deals, showing that momentum remained intact even after May’s surge.

Refinancing and reset activity followed a similar pattern. Volume nearly doubled from $19.8B across 49 deals in April to $38.4B across 87 deals in May before easing modestly to $35.3B across 79 transactions in June. Even with the slight decline, refinancing remained well above April levels as issuers took advantage of improved pricing.

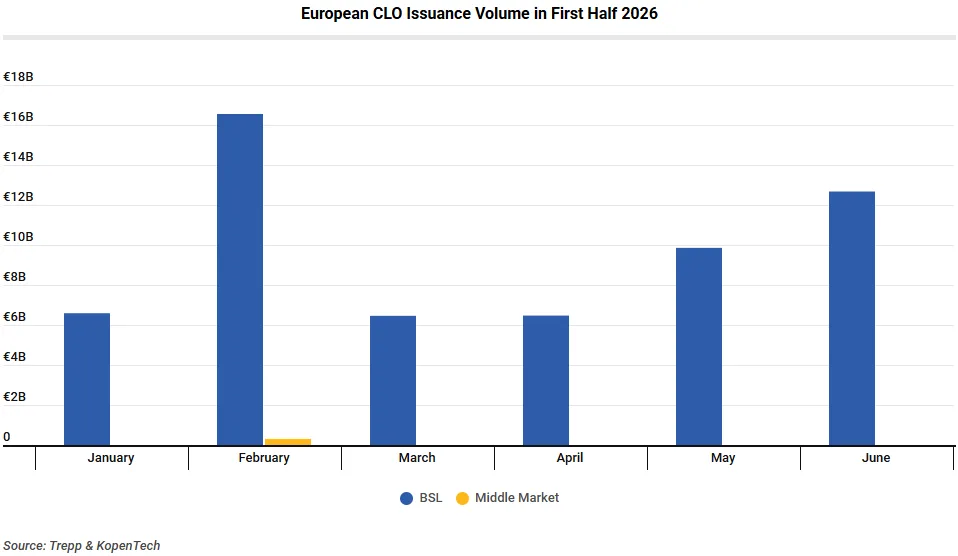

Europe experienced a more gradual recovery. Total issuance climbed from approximately €6.5B in April to €9.9B in May before reaching €12.7B in June, the strongest monthly total of the quarter.

Unlike the US, Europe recorded no middle-market CLO issuance during the period. The market remained focused on broadly syndicated transactions as improving financing conditions encouraged new issuance.

Tighter AAA Spreads Support Issuance

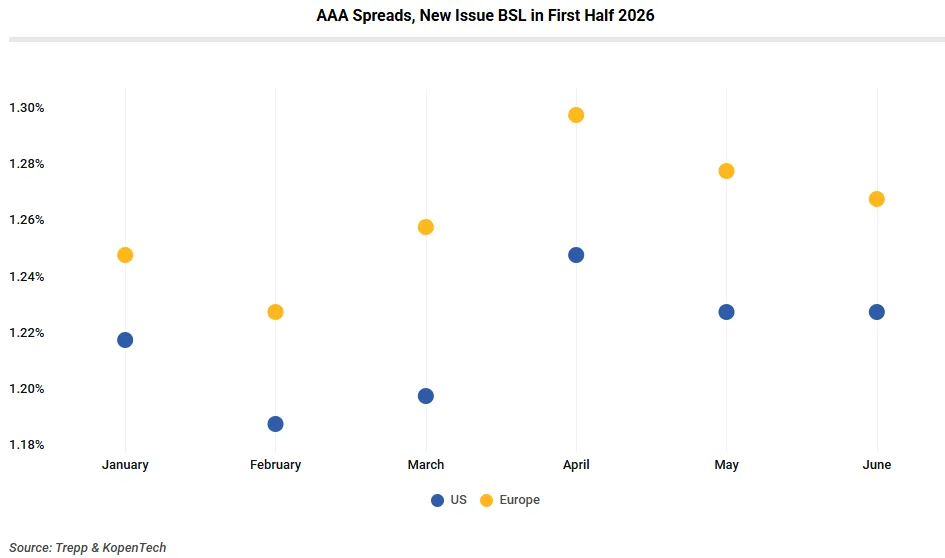

Improving pricing helped sustain the market’s recovery. Average AAA spreads on new US broadly syndicated CLOs narrowed from 1.25% in April to 1.23% in June. European AAA spreads also tightened, falling from 1.30% to 1.27% over the same period.

Structural terms remained relatively stable. US new issue non-call periods held near two years throughout the quarter, while European deals averaged roughly 1.5 years. Reinvestment periods changed little across both markets, although US refinancing transactions gradually extended their reinvestment periods through June. Europe also saw new issuance exceed refinancing and reset activity for the quarter overall, reversing the first-quarter trend.

Why It Matters

The second quarter reinforced the CLO market’s ability to recover quickly after periods of volatility. Rather than weakening credit performance, geopolitical developments and broader market uncertainty proved to be the primary factors behind April’s slowdown.

That distinction matters for commercial real estate lenders and institutional investors. CLOs remain a major funding source for leveraged loans, making issuance trends an important indicator of overall credit market health. Stable deal structures, tightening AAA spreads, and sustained refinancing activity suggest investors continued to view structured credit favorably as market conditions improved.

The results also demonstrate that demand remained strong enough to absorb new supply once pricing stabilized, providing issuers with greater flexibility to access capital.

What’s Next

The second half of 2026 will likely depend on whether financing conditions remain supportive. Continued stability in AAA spreads could encourage additional refinancing activity while supporting another wave of new issuance across both the US and Europe.

Investors will also monitor geopolitical developments and monetary policy for signs of renewed volatility. Those factors drove much of the quarter’s early slowdown and remain the largest external risks to issuance.

If credit fundamentals remain intact and spreads continue to tighten, the CLO market appears positioned to sustain its recovery through the remainder of 2026. For commercial real estate investors and leveraged credit participants, Q2 showed that structured finance markets continue to absorb macro uncertainty without losing access to capital.