- The USMCA trade agreement’s missed renewal deadline increases uncertainty for North American manufacturing and logistics networks.

- Rent growth for US industrial properties slowed to 5.2% year-over-year, as vacancy reached 8.8% and new lease premiums narrowed across markets.

- Investor appetite is softening in core industrial markets, with prices down—most notably in the Inland Empire—even as long-term fundamentals remain strong.

Trade Policy Uncertainty Clouds Industrial Outlook

The future of the US-Mexico-Canada Agreement (USMCA) is now in question, as the tri-national deal failed to secure an automatic 16-year renewal before the July 1, 2026 deadline, according to Yardi Matrix’s June industrial report. The agreement, which governs about $2 trillion in annual cross-border trade and over a quarter of US trade activity, is foundational for supply chains across North America, especially as Mexico and Canada account for nearly 30% of total US trade, dwarfing China’s waning share at just over 6% this year.

Instead of automatic renewal, the USMCA now enters a period of rolling annual reviews, opening the door to prolonged negotiations and the possibility of major changes by 2029. Canadian officials expect talks could drag on for several years. This added policy risk lands at a time when manufacturers, especially in automotive and advanced sectors, depend on stable tariff-free flows for goods that often cross borders multiple times per production cycle. Supply chain visibility and cost certainty are now on shakier ground.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

Trade risk is weighing on strategic decision-making throughout the US industrial sector. USMCA-compliant goods have so far avoided major tariff battles, but the missed deadline shifts the landscape. Any future overhaul will require approval from Congress and could be shaped by add-ons or protocols rather than wholesale rewriting of the pact. According to the Yardi Matrix report, industrial players are extending planning horizons or delaying investments, prioritizing flexibility over rapid expansion as policy fog persists.

Meanwhile, trade-driven sectors like automotive and advanced manufacturing remain vulnerable. Components in these industries typically cross borders several times before final assembly, making even minor regulatory tweaks potentially disruptive. Prolonged trade uncertainty risks becoming the biggest headwind for industrial players, introducing planning complexity just as leaders seek efficiency and speed-to-market.

Rent Growth Slows as New Lease Premiums Shrink

On the operational side, national in-place industrial rents averaged $9.12 PSF in May—up 4 cents month-over-month and 5.2% year-over-year, per Yardi Matrix. This pace represents a slowdown from the double-digit surges seen in 2022. Vacancy nationally reached 8.8%, a 30 basis point rise over the past 12 months, coinciding with a moderation in new supply after record pipeline deliveries. The in-place rent bump was greatest in the Inland Empire (+8.1%), while Boston posted 6.3% despite above-average vacancy that reflects the challenges of its aging industrial stock, with one-third built before 1970. Markets like Bridgeport, Miami, and Boston saw new lease premiums of about $3 PSF over market averages, but these premiums have compressed overall as supply-demand fundamentals recalibrate. For perspective, leases signed in the last 12 months averaged $10.06 PSF, just 94 cents above average in-place rents—a much narrower spread than past years.

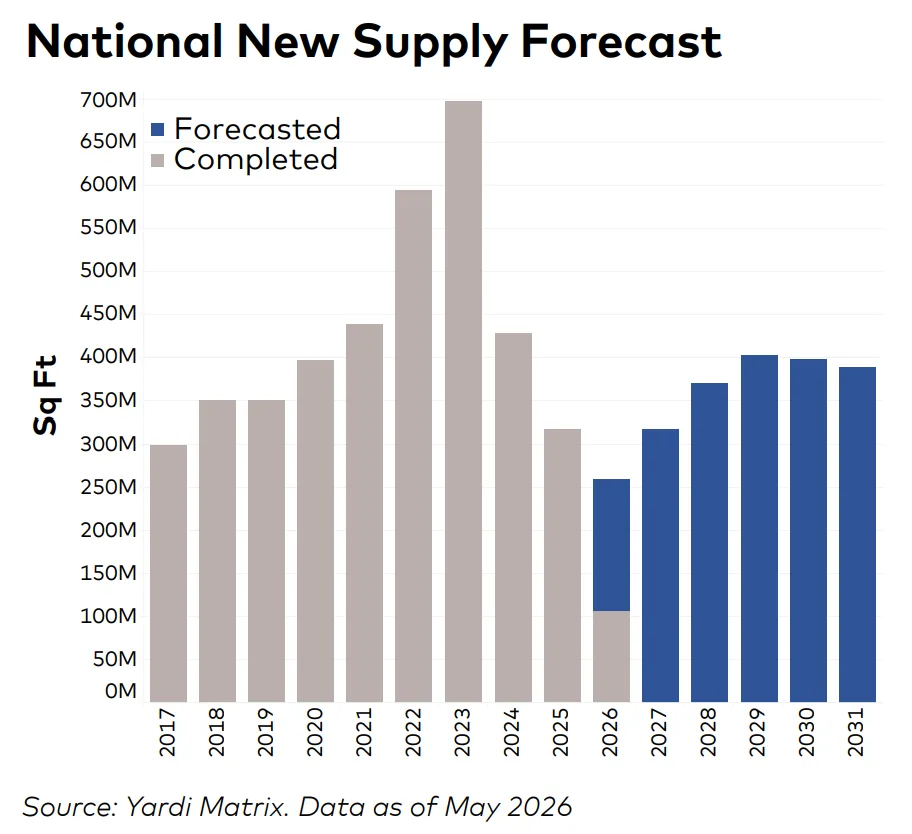

Supply Pipeline Adjusts to Softer Demand

New construction has slowed across many regions. The national pipeline currently totals 383.2M SF, about 1.8% of existing stock. Markets like Phoenix remain active (5.5% of stock under construction), but metros such as Kansas City are cooling after unprecedented growth. Kansas City delivered 54.9M SF (17.6% of its stock) between 2020 and 2025 but now has only 3.5M SF under construction—reflecting a broader pause as demand normalizes.

Notably, Kansas City’s largest recent completion was Panasonic’s 4.7M SF EV battery plant; facing both EV demand shifts and tax credit changes, Panasonic is already pivoting production, a microcosm of how sector demand can swing rapidly. Cooling supply tails off the post-pandemic warehouse boom, while markets with modern, efficient space will continue to attract tenants seeking operational gains.

Why It Matters

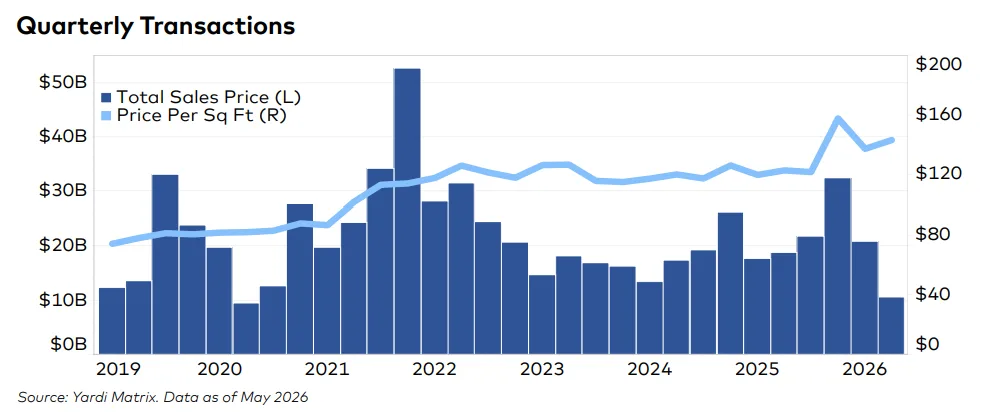

The intersection of softening transaction volumes, moderating rent growth, and trade policy uncertainty leaves industrial players reassessing risk and reward. Sales through May reached $31.5B nationally, with properties trading at $139 PSF. The Inland Empire, long an investor favorite, saw average sale prices fall to $172 PSF, down 23% from 2025 and 40% from the 2022 peak, per Yardi Matrix. These pricing shifts extend the trend of investors becoming more selective as tariff concerns reshape industrial market priorities. Investors that entered the market a decade ago still post strong returns—as in Clarion’s $145M buy of a fully leased Amazon facility in Riverside, yielding an over 80% gain for the seller since 2017.

Amid these shifts, e-commerce remains a steady anchor. US Census Bureau data shows e-commerce sales hit $326.7B in Q1 2026, up 9.8% year-over-year and now accounting for 19.8% of core retail sales. While the surge seen at the pandemic’s peak had plateaued, the past year brought renewed growth. This structural driver is cushioning industrial’s long-term outlook, even as tariffs, energy costs, and policy wrangling create short-term turbulence. Industrial investors and developers will need sharper underwriting and flexible strategies as nearshoring themes compete with cyclical uncertainty.

What’s Next

Looking ahead, the industrial sector is entering a choppier phase as policy risk overlays cyclical cooling. If the USMCA negotiations drag into 2029, vendors and occupiers will likely emphasize supply chain resilience and site selection strategies that minimize border friction. With the new supply pipeline cooling—especially in Midwestern and Coastal legacy markets—rents could stabilize, particularly for modernized assets. Watch for whether e-commerce’s share surpasses its pandemic high this year, providing further stability for logistics remains a multiyear question. Despite the headwinds, strong sector fundamentals should enable patient capital and best-in-class operators to outperform.