- Developers had roughly 61,700 build-to-rent units under construction nationwide as of May 2026, according to RealPage Market Analytics.

- The South leads activity with more than 37,400 units underway, while Phoenix, Dallas, Atlanta, Houston, and Charlotte remain the sector’s biggest metros.

- Elevated mortgage rates, limited for-sale inventory, and affordability pressures continue pushing renters toward professionally managed single-family housing options.

Build-to-rent development remains heavily concentrated in the Sun Belt as renters stay in the leasing market longer and homeownership affordability remains strained. According to RealPage Market Analytics, developers had about 61,700 BTR units under construction nationwide in early May 2026, with projects expected to deliver through the first half of 2029.

RealPage defines build-to-rent housing as detached and attached single-family rental product, including townhomes, duplexes, row houses, and quadruplexes built specifically for renters. The sector continues gaining traction as elevated home prices and mortgage rates above 6% keep many households from transitioning into ownership.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Bold Sun Belt Pipeline

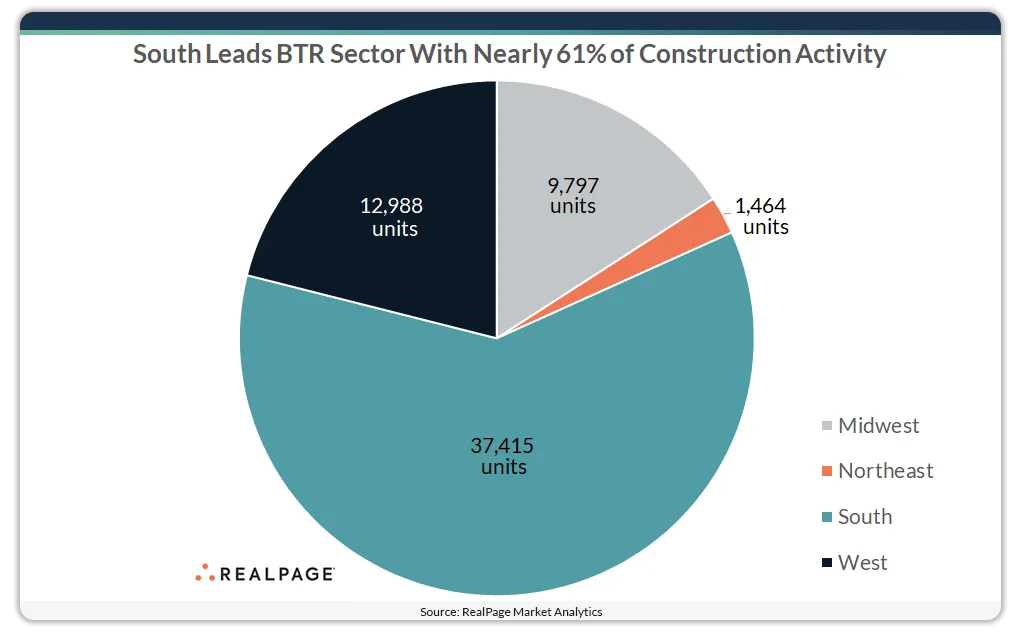

The South alone accounted for more than 37,400 BTR units underway as of May 2026, or roughly 61% of the national pipeline, per RealPage. The West added another 13,000 units, meaning the two regions together controlled nearly 82% of all BTR construction activity nationwide.

The Midwest represented nearly 9,800 units, or about 16% of the pipeline, while the Northeast accounted for just 1,500 units, or roughly 2%. RealPage noted that BTR growth continues tracking population migration trends and demand in suburban markets shaped by remote and hybrid work patterns.

The Details

Phoenix maintained its position as the nation’s largest BTR market with nearly 7,300 units under construction, representing about 12% of all projects underway nationally. Dallas followed with roughly 3,700 units, while Atlanta ranked close behind with approximately 3,500 units in progress.

Houston and Charlotte rounded out the top five with about 3,000 and 2,900 units underway, respectively. Other active metros included Nashville (2,800 units), Raleigh/Durham (2,300 units), Tampa (2,100 units), Austin (1,700 units), San Antonio (1,700 units), and Indianapolis (1,500 units).

Beyond the major metros, RealPage tracked another 20 apartment markets with between 500 and 1,000 BTR units underway. Kansas City, North Port, Florida, and Columbus each had about 1,400 units under construction, while Huntsville and Orlando also crossed the 1,000-unit mark.

Suburban Growth Drives Demand

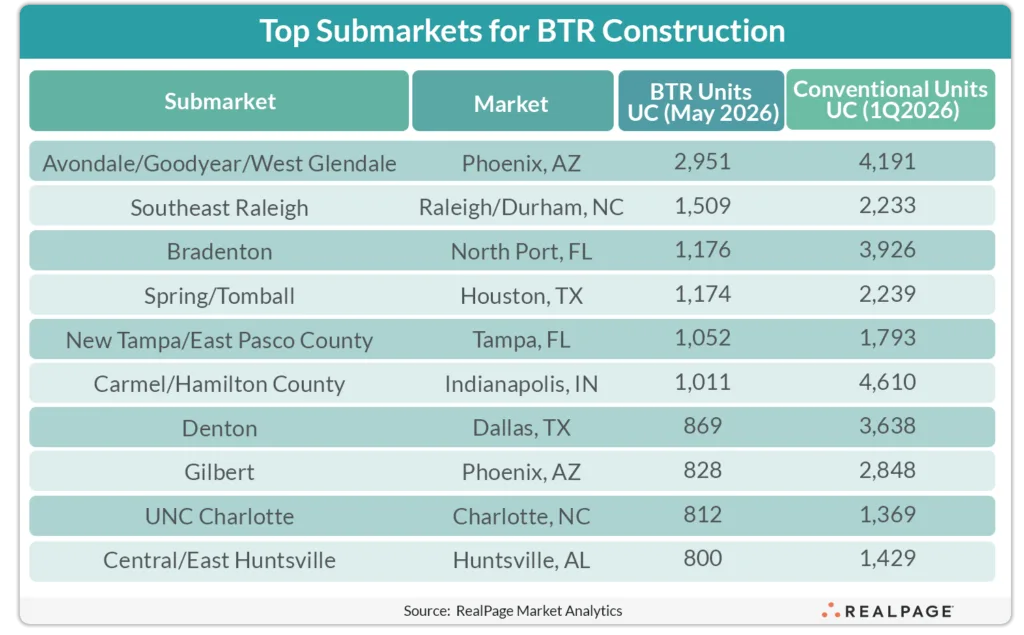

Submarket activity remained concentrated in suburban Sun Belt nodes, particularly across Arizona, Texas, North Carolina, and Florida. Phoenix’s Avondale/Goodyear/West Glendale submarket led nationally with nearly 3,000 units underway.

Southeast Raleigh followed with more than 1,500 units in development, while Bradenton, Florida, had approximately 1,200 units in the pipeline. Other high-activity submarkets included Spring/Tomball near Houston, New Tampa/East Pasco County, Denton, Gilbert, and the UNC Charlotte area.

Why It Matters

The BTR sector continues filling a gap between apartment renting and homeownership as affordability pressures persist across the housing market. According to Freddie Mac’s April 2026 mortgage market data, 30-year fixed mortgage rates remained above 6%, limiting purchasing power for many households.

That backdrop has strengthened demand for rental housing with private yards, garages, and larger floor plans. Developers are also concentrating activity in high-growth Sun Belt metros as broader construction pipelines begin moderating nationwide.

What’s Next

RealPage is also tracking more than 6,700 planned BTR units nationwide beyond projects already under construction, signaling developers still see long-term runway for the asset class despite broader economic uncertainty.

Markets with strong population growth, constrained for-sale housing inventory, and relative affordability advantages are likely to remain focal points for future BTR investment. Sun Belt metros, particularly Phoenix, Dallas, Atlanta, and Raleigh, appear positioned to continue leading development activity through the next several years.