- Every major self-storage REIT reported positive or flat year-over-year same-store revenue growth in Q1 2026, marking the strongest sector-wide performance since 2024.

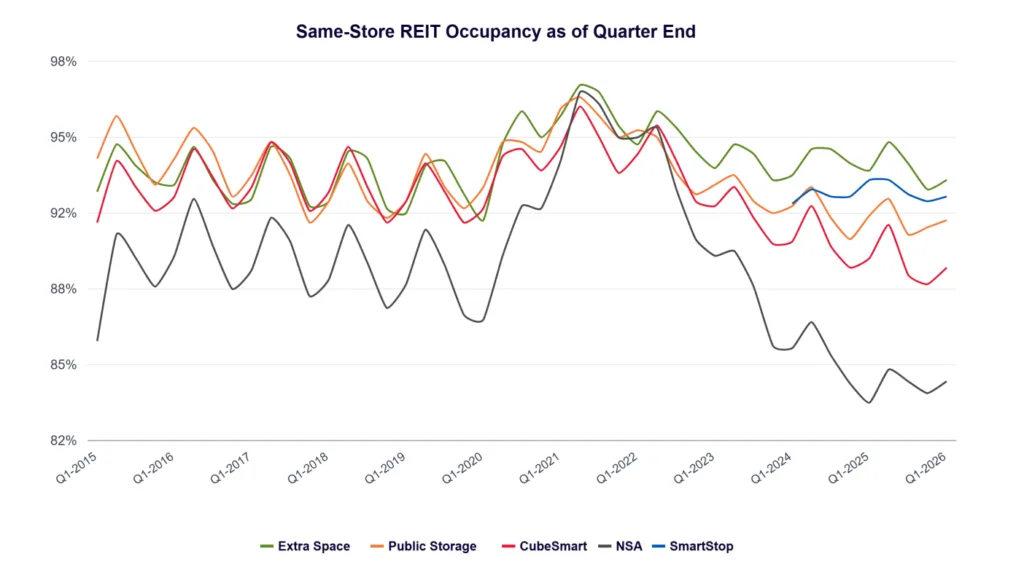

- Occupancy remained stable at 90.9%, while operators continued relying on in-place rent increases as street rates lagged achieved rents by a record-wide margin.

- The sector appears to be moving from correction to stabilization, though elevated supply in key Sun Belt markets continues to pressure rents and lease-up performance.

Self-storage may have reached a turning point. According to TractIQ’s Q1 2026 Self-Storage REIT Report, every publicly traded self-storage REIT posted positive or flat same-store revenue growth year over year, the first time that has happened since the firm began tracking the metric in 2024. Occupancy remained steady, move-in trends improved, and several operators reported their strongest leasing signals in years.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Long-Awaited Recovery for Self-Storage REITs

The industry has spent much of the past two years working through the aftermath of the pandemic-era demand surge and a wave of new development. Revenue growth slowed, occupancy fell from record highs, and operators leaned heavily on existing customer rent increases to maintain performance.

Q1 2026 suggests that reset phase may be ending. TractIQ reported same-store revenue growth of 1.7% for Extra Space Storage, 1.5% for SmartStop, 0.6% for CubeSmart, 0.2% for National Storage Affiliates (NSA), and flat performance for Public Storage. More importantly, every major REIT landed in positive or neutral territory during the quarter.

The Details

Sector-wide same-store occupancy finished Q1 at 90.9%, down just 0.2 percentage points from a year earlier. While still roughly 5.1 percentage points below the 2021 peak, the relatively small year-over-year change suggests occupancy has stabilized rather than continuing to decline, according to TractIQ. The performance aligns with broader occupancy stabilization trends that emerged across the self-storage sector during 2025.

Extra Space led the sector with 93.0% occupancy, followed by SmartStop at 92.3% and Public Storage at 91.3%. NSA was the only REIT to post meaningful occupancy gains, increasing 0.9 percentage points year over year to 84.5%.

The quarter also featured one of the industry’s biggest strategic announcements. Public Storage revealed plans to acquire NSA in an all-stock transaction valued at approximately $10.5B. The deal would add more than 1,000 wholly owned NSA properties to Public Storage’s platform and significantly expand its presence in secondary and tertiary markets, with closing expected in Q3 2026.

Street Rates Still Tell a Different Story

While operating fundamentals improved, pricing remains uneven.

TractIQ found that REITs achieved an average rent of $20.66 PSF, while average street rates across REIT portfolios sat at just $16.52 PSF. That 25% premium widened from 19.2% a year earlier and highlights how dependent operators remain on existing-customer rent increases rather than stronger pricing for new tenants.

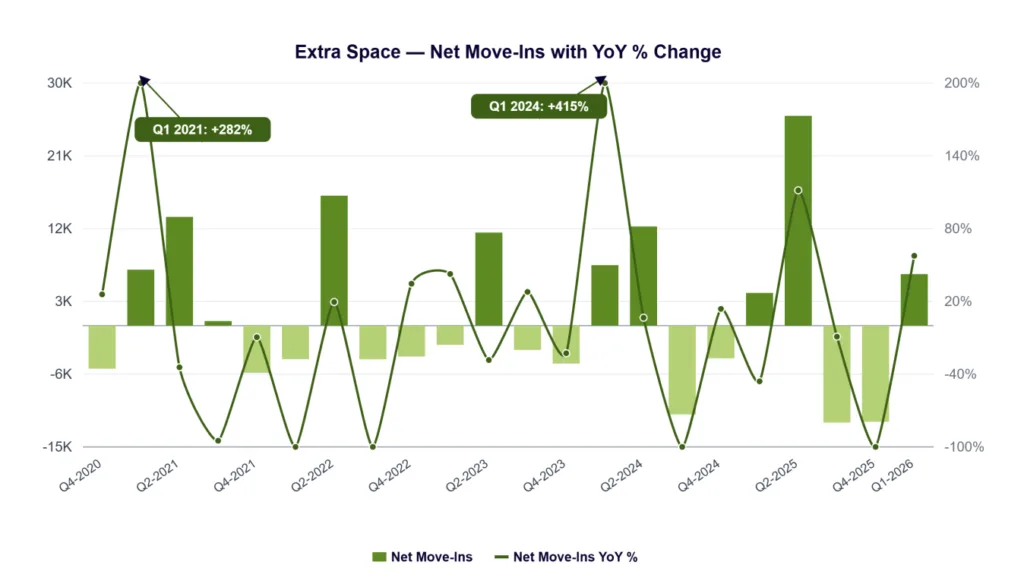

Move-in data offered a more encouraging signal. Extra Space reported a 58% year-over-year increase in net move-ins, while CubeSmart posted its largest move-in gain since 2023. TractIQ noted that Extra Space’s move-in rates turned positive year over year for the first time since the company began reporting the metric, while Public Storage recorded its smallest move-in rate decline since 2020.

Those trends suggest demand may finally be improving after several years of softening.

Supply Pressures Remain Concentrated

Market-level performance continues to split along geographic lines.

Coastal and Northeast metros generally produced the strongest rent growth. Markets including Boston, Washington, DC, New York, Chicago, Minneapolis, and San Jose appeared frequently among top performers across REIT portfolios.

Meanwhile, Texas and Florida remain among the sector’s most challenged markets. Austin, Dallas-Fort Worth, San Antonio, Tampa, Cape Coral, and North Port repeatedly ranked among the weakest performers for rent growth or occupancy trends, reflecting the ongoing impact of new supply deliveries.

The data underscores a recurring theme across commercial real estate: markets that experienced the most aggressive development activity during the pandemic boom are taking longer to rebalance.

Why It Matters

The self-storage industry has been searching for evidence that operating fundamentals were stabilizing after a multi-year correction. Q1 2026 delivered some of the clearest signs yet.

Revenue growth has returned, occupancy appears to have found a floor, and leasing activity is improving. At the same time, REIT operators continue to maintain a substantial performance advantage over private operators. TractIQ found REIT occupancy averaged 90.9% versus 79.6% for non-REIT facilities, an 11.3-percentage-point gap driven by scale, branding, digital marketing capabilities, and revenue-management systems.

What’s Next

Investors will be watching whether improving move-in activity translates into stronger revenue growth later this year. The industry’s biggest challenge remains closing the gap between discounted street rates and higher in-place rents without sacrificing occupancy.

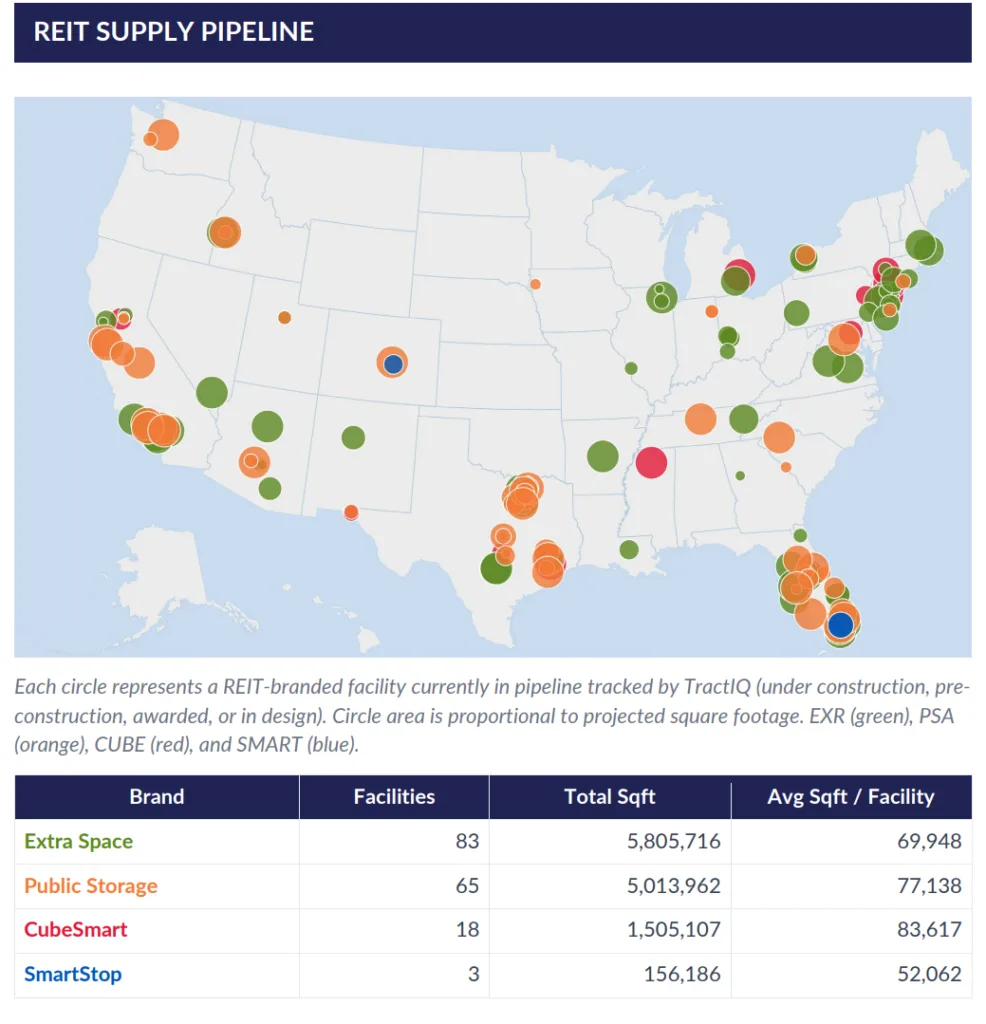

Development also remains active. TractIQ tracks 169 REIT-branded facilities currently in the pipeline totaling approximately 12.5M SF, led by Extra Space with 83 projects and Public Storage with 65. As new supply slows and demand normalizes, operators will be looking for clearer evidence that pricing power is returning.