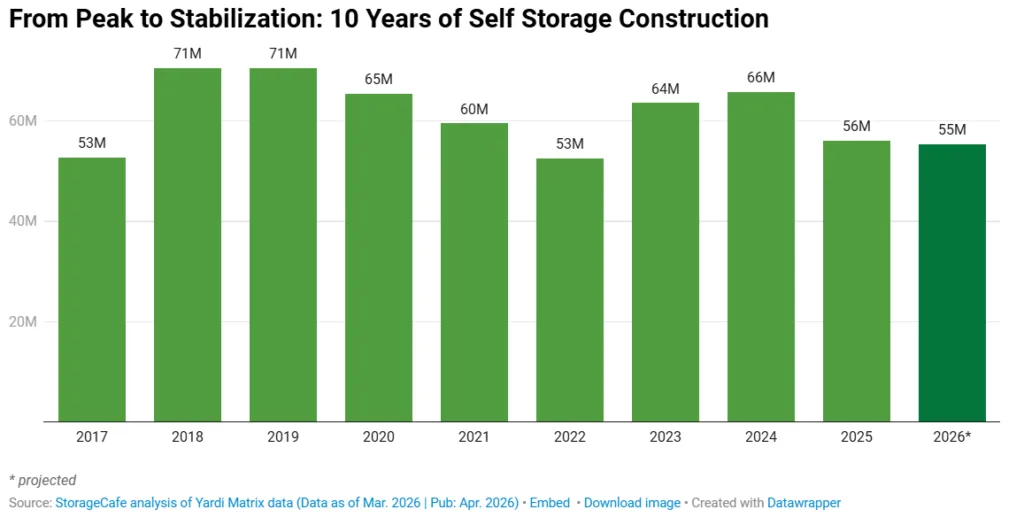

- Self storage supply will grow by 55.4M SF in 2026—2.6% of US inventory.

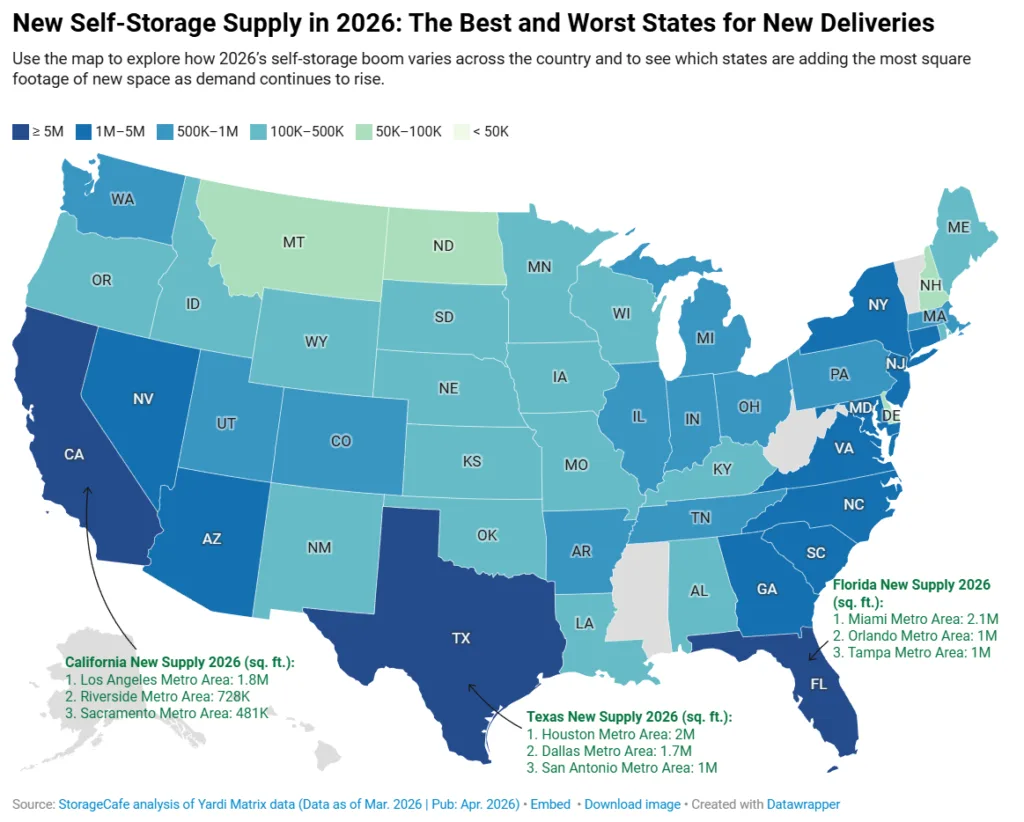

- Florida leads with 10.3M SF delivered, followed by Texas and California.

- Rents are falling or flat in most major metros, with New York as a key exception.

- Lumberton, NC leads small markets with a 58% increase in self storage inventory.

Steady National Self Storage Expansion

Self storage expansion continues nationwide in 2026, with 55.4M SF of new space slated for delivery—about 2.6% of total inventory, reports StorageCafe. The largest gains are concentrated in Southern and Western states, notably Florida, Texas, and California. This signals an industry adapting to post-surge demand with moderated, regionally targeted growth.

Development activity remains robust in major metros, with 15 markets expecting over 1M SF in new deliveries this year. Notably, New York and Phoenix each project nearly 3M SF, reflecting long-standing demand resilience. In smaller and secondary markets, the pace can be even sharper—such as Lumberton, NC, where inventory is set to jump 58%.

Florida Outpaces All States

Florida dominates self storage expansion in 2026, delivering 10.3M SF—6% of its local inventory. Sustained migration, retiree demand, and a dynamic housing market are main contributors. Multiple Florida metros rank in the nation’s top 20 by new supply, reinforcing long-term demand confidence. However, the surge has put downward pressure on rents; statewide, rates fell 2.8% year over year. This pressure reflects a broader pattern, where rising supply continues to weigh on pricing across several major markets.

Texas follows with 6.9M SF (3% growth), benefitting from its vast, diversified metro footprint, which helps avoid steep rent declines. California, though facing entitlement and land cost challenges, will add over 5M SF but maintains the highest average street rates among major states due to persistent under-supply.

Regional Trends and Rent Impact

Self storage supply is also rising in Georgia, North Carolina, and the Northeast. Georgia’s Savannah stands out with a 17.5% projected inventory jump linked to its port and industrial base. North Carolina’s 1.7M SF in planned supply is more broadly distributed, tracking state-wide household and employment growth.

Notably, the New York and New Jersey metros are growing inventory by about 4%, addressing historic undersupply. These markets still see rent resilience, as demand quickly absorbs new units. In contrast, in Sun Belt cities with oversupplied conditions (e.g., Houston, Dallas–Fort Worth, Jacksonville), rent declines are now the norm.

Metros and Small Market Standouts

New York leads total deliveries among the top 10 metros, with 3.2M SF. However, it remains the most undersupplied. This imbalance supports modest rent growth. Phoenix follows with a 2.9M SF pipeline. Its growth reflects strong in-migration and sustained expansion. Meanwhile, Miami and Los Angeles continue to command high street rents. This holds true despite ongoing new deliveries. In smaller markets, growth appears more pronounced. Lumberton, NC posted a 58% increase, driven by regional investment. Similarly, Savannah continues to expand, reinforcing investor focus on port-adjacent cities.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

What’s Next

Self storage expansion in 2026 marks a transition from the previous decade’s rapid pace to a measured, demand-aligned cycle. The market remains competitive, particularly in the South and West. Rent corrections continue in well-supplied regions, while historically tight markets still see upward price movement. Operators and investors are expected to maintain a targeted approach, focusing on absorption rates and micro-market dynamics to guide future delivery pipelines.