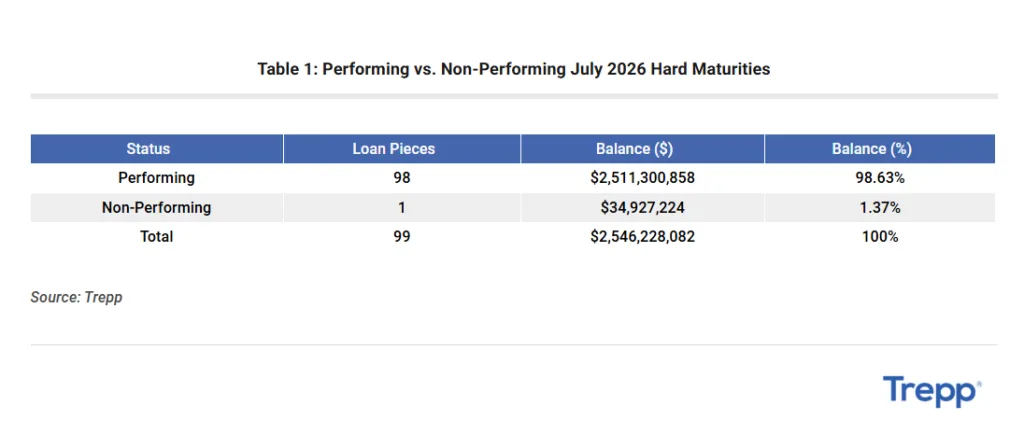

- July 2026 CMBS hard maturities total $2.54B, with retail—especially regional malls—leading exposure.

- 36% of 2026 maturities have an 8% or lower debt yield, amplifying refinancing challenges in office, retail, and multifamily segments.

- High concentration among a few large loans and rising special servicing rates signal growing market stress—particularly for regional malls and office assets.

CMBS Maturities Concentrate Refinancing Pressure

July’s wave of hard CMBS maturities is bringing refinancing pressure for retail and office, according to Trepp’s June 2026 data. Hard maturities—where no extensions remain—require swift payoff or restructuring, and regional malls are among the largest exposures facing that test. The newly delinquent loan list is dominated by non-performing matured balloon loans, with retail at the center of the storm. Among the top five new delinquencies are two major malls, illustrating ongoing friction as these asset types navigate a difficult lending and valuation landscape.

Nearly 40% of the $76.6B in 2026 hard CMBS maturities will come due in Q4, concentrating risk toward year-end. Notably, more than a third of these loans have low debt yields, historically linked to the highest rate of refinancing failure, making this cohort a bellwether for brewing distress in sectors already under strain.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

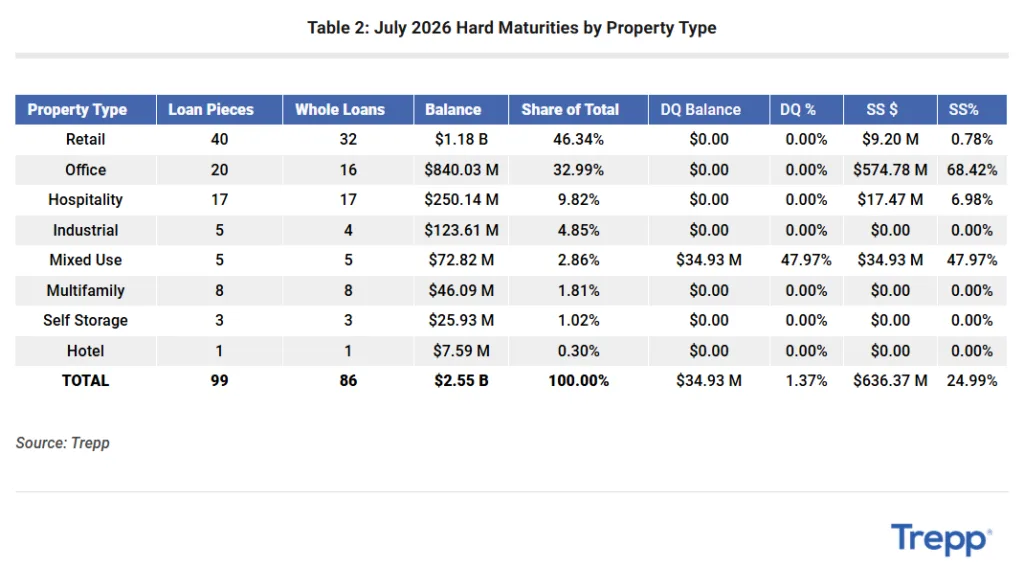

Retail loans represent the largest share of July’s CMBS maturities, totaling $1.18B, or 46.34% of the cohort, per Trepp. Office follows at $840.03M (32.99%), then hospitality at $250.14M (9.82%). Only one loan in the group— a mixed-use property worth $34.93M—was reported delinquent. However, closer scrutiny shows that traditional delinquency doesn’t capture the full risk: 24.99% of the July maturity balance ($636.37M) is already in special servicing. For office, this figure jumps to 68.42% of that subsector’s balance, suggesting lenders and borrowers are negotiating solutions ahead of outright default, particularly where refinances are mostly out of reach.

Concentration Bolsters Top-Heavy Risk

The July maturity pool is highly concentrated, with a few large loans accounting for nearly half the balance. Trepp reports that $1.23B, or 48.37%, sits within this small group of assets. Many are regional malls, super-regional malls, and large office properties.

Distress among these loans can heavily influence overall delinquency figures. July’s special servicing activity suggests lenders are favoring workouts over immediate defaults.

Why It Matters

Hard maturities continue to expose refinancing challenges for retail, office, and multifamily owners. Trepp reports that 36% of 2026 maturities carry debt yields of 8% or less. Regional malls remain especially vulnerable as valuations lag and underwriting standards tighten.

With $76.6B in hard maturities due this year, refinancing pressure is unlikely to ease soon. July’s concentration among a handful of large loans raises the stakes for individual resolutions. Many borrowers may need fresh equity or discounted payoffs to complete refinancing.

What’s Next

Nearly 40% of 2026 hard CMBS maturities are still scheduled for Q4, according to Trepp. Refinancing pressure could intensify if rates remain elevated through year-end. Regional malls and large office towers are likely to remain key stress points.

Lenders are expected to focus closely on debt yields and property performance. More borrowers may face workouts, special servicing, or ownership changes as maturities approach.