- Manhattan led all US markets in office investment, rental rates, and flex space footprint in the first four months of 2026, according to Yardi Matrix.

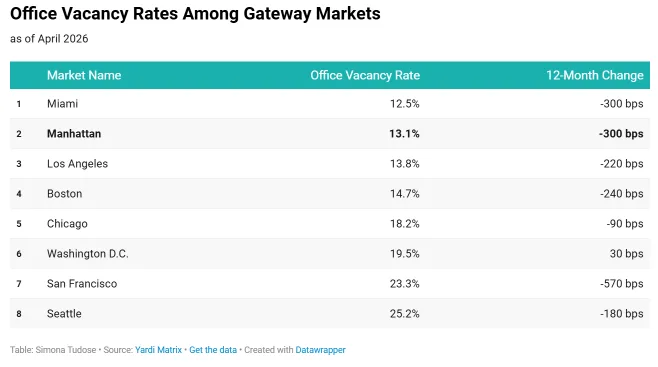

- Vacancy dipped to 13.1%, trailing only Miami among major metros, while new construction and leasing volume remain strong despite broader sector headwinds.

- High pricing and dense development confirm Manhattan’s resilience, but inventory and investor activity also reinforce its status as the primary US gateway office market.

Manhattan Defies National Office Slowdown

The Commercial Property Executive reports that Manhattan’s office market is showing surprising resilience in a year when many peers are grappling with sluggish leasing and elevated vacancies. According to Yardi Matrix, the borough claimed the top spot nationally for office investment volume, average rents, and coworking density between January and April 2026. Despite persistent sector-wide pressures—higher interest rates, widespread remote work, and softening tenant demand—investment and development pipelines in Manhattan remain robust, bucking national trends. The office vacancy rate dropped 300 basis points year-over-year to 13.1%, one of the lowest across major US metros, and Manhattan sustained the country’s most expensive leasing environment, with average asking rents of $69.29 PSF in April.

This competitive position stands out in a national office sector where the average vacancy is 17.6% and asking rents measure $32.91 PSF. Manhattan’s fundamentals are all the stronger when weighed against severe softness in cities like Seattle and San Francisco, where vacancies exceed 23% and sales activity has slowed significantly.

Get Smarter About What Matters in New York

Subscribe to our free newsletter covering the biggest commercial real estate stories across the five boroughs — delivered in just 5 minutes.

The Details

From January through April 2026, Manhattan notched just under $3B in total office sales, far outpacing San Francisco ($1.6B) and Dallas ($1.1B). Average sales prices reached $712 PSF, more than three times the national average of $214 PSF, and narrowly higher than San Francisco’s $686 PSF. The most prominent deal year-to-date: SL Green’s $730M acquisition of Park Avenue Tower, a 36-story LEED Gold building in the Plaza District. On the leasing front, Optiver expanded its presence at 360 Park Ave. S. to 115,000 SF, while Starr Insurance committed to a 275,000 SF, 20-year lease at BXP’s 343 Madison Ave.—currently the city’s second-largest office development, set to open in 2029.

New construction is also holding up. Manhattan tracked 3.3M SF underway across nine projects, equal to 0.7% of local inventory and second only to Boston among US gateway markets. The largest single project is Related Cos.’ 70 Hudson Yards, a 1.4M-SF tower slated for completion in late 2028, with Deloitte already committed for 800,000 SF as its future North American HQ.

Investment Metrics and Vacancy Stand Out Nationally

By April, Manhattan’s tight 13.1% vacancy rate ranked only behind Miami (12.5%) among major US cities, per Yardi Matrix. The borough recorded a 300 basis point drop in vacancy over the prior twelve months, matching Miami and outpacing improving but still-soft markets such as Denver and San Francisco. At the other end, Seattle’s office vacancy hit 25.2%, and San Francisco followed at 23.3%—indicative of slower recoveries in several traditionally strong gateways.

This relative strength comes as office visitation data from Placer.ai shows nationwide traffic to office buildings in April 2026 remains 29.1% below April 2019 levels. In contrast, New York City’s decline, at just 10.4%, is the mildest in any major market. Average rents in Manhattan lead the nation at $69.29 PSF, substantially above San Francisco ($62.03 PSF) and Miami ($58.41 PSF), and more than double Chicago ($28.02 PSF) or Detroit ($20.81 PSF).

Why It Matters

Manhattan has confirmed its resilience as a premium office market, even as the wider US sector grapples with disruptions. Investors and institutional owners continue to bet heavily on core Manhattan assets, with nearly $3B in sales tallied through April 2026—well above other top-tier cities. That’s despite growing scrutiny of return-to-office patterns and long-term tenant demand.

Yardi Matrix data highlights that prime central business district locations—backed by large, long-term tenants and best-in-class amenities—are absorbing the brunt of market turbulence and still commanding premium rents. This is illustrated by active leasing: major renewals and expansions from firms like Optiver, Starr, and Deloitte at landmark towers have set a tone of confidence, while SL Green’s $730M acquisition puts another vote of faith in trophy assets’ value retention.

Manhattan’s 3.3M SF construction pipeline, led by the ambitious 70 Hudson Yards, also signals ongoing commitment to new office supply at a moment when most cities are pulling back. That momentum aligns with broader gains in flexible workspace, as operators continue adding locations in leading office hubs. With flex office space totaling 12.8M SF across 309 sites, Manhattan’s coworking market is more than a hedge: it’s central to the local ecosystem, outpacing even high-demand markets like Los Angeles and Washington, D.C.

Compared to other US gateway markets, Manhattan’s sharper recovery in vacancy, combined with its rent premium, flags it as a relative safe haven for occupiers and investors seeking stability in a shifting office landscape.

What’s Next

New York’s office market will be closely watched as new supply—including the $1.4B 70 Hudson Yards tower—delivers through 2028. Large preleases, such as Deloitte’s 800,000 SF commitment, hint at sustained demand for best-located, amenitized properties. The flex office sector is likely to remain a key growth segment as tenants pursue agility. While national office visitation lags, Manhattan’s momentum on leasing, pricing, and investment will test whether the borough can continue to outpace the rest of the country or if macro headwinds eventually decelerate activity. Investors and developers are betting Manhattan still sets the benchmark for the US office sector in the years ahead.