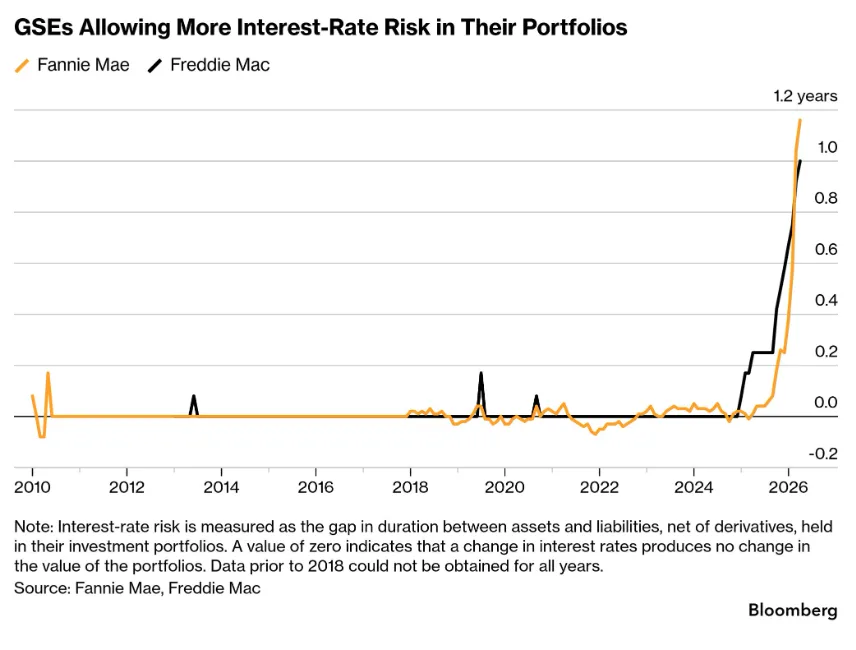

- Fannie Mae and Freddie Mac’s duration gaps have expanded to one year, exposing portfolios to multi-billion dollar losses from rate hikes.

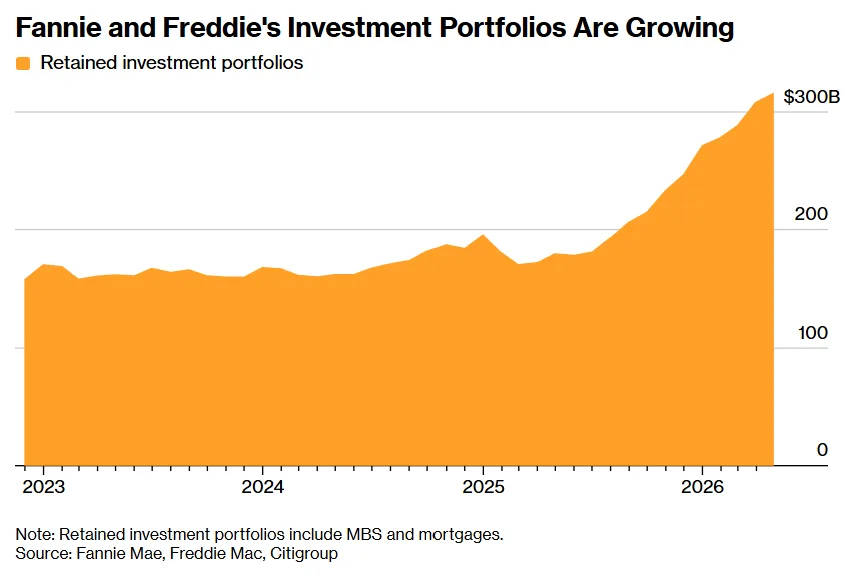

- The agencies have added over $135B to retained portfolios in a push to support lower mortgage rates, but are leaving more rate risk unhedged.

- This policy-driven risk-taking aims to aid home affordability but revives concerns reminiscent of early-2000s Wall Street shocks.

Risk Appetite Returns to Agency Mortgages

Fannie Mae and Freddie Mac have ramped up their interest-rate exposure to a level that hasn’t been seen since the early 2000s, Bloomberg reports. Duration gaps at both entities have widened sharply this year, meaning their assets are less well-matched to their liabilities and hedges—raising the risk of significant losses if interest rates move against them. This development coincides with a political push to make home loans more affordable by expanding the agencies’ portfolio holdings.

According to agency disclosures cited by Bloomberg, both Fannie and Freddie have duration gaps around one year—a move away from the tight hedging that defined their post-crisis operations. With over $135B added to their portfolios in the past year, they’re taking a calculated risk to influence mortgage rates, even as the tradeoff means greater sensitivity to future rate moves.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The End of Post-Crisis Stringency

Until recently, the government-sponsored enterprises (GSEs) were tightly restricted following the 2008 financial crisis, with a clear policy emphasis on minimizing risk at all costs. That era of conservatorship ‘lockdown’ led to stringent risk management and modest investment activity. But as the focus has shifted to housing affordability, so too has the agencies’ mandate: they’re now deploying capital into longer-term mortgage-backed securities (MBS), even if that means less hedging and higher duration mismatch. Veteran strategists recall that in the early 2000s, a similar risk imbalance shook both markets and regulators, underlining the stakes in the current expansion.

The Details

Recent regulatory filings put the agencies’ duration gaps at approximately one year. A 50 basis-point rate increase would knock $1.2B off Fannie’s portfolio value and $1.6B off Freddie’s, compared to negligible effects a year ago. This exposure is a direct result of the agencies adding over $135B to their retained portfolios in 2025-26, per Bloomberg.

The move aims to shrink the available supply of agency MBS, reducing yields and helping tamp down mortgage rates. But by opting to hedge less, Fannie and Freddie mitigate the pressure of Treasury trades that otherwise could push home-loan rates higher—a policy calculation with clear political implications ahead of US midterm elections.

Portfolio Growth and Past Parallels

Comparisons abound between today’s risk-taking and past incidents. In 2002, Fannie Mae’s duration gap hit minus 14 months as borrowers refinanced unexpectedly en masse, cutting asset life and panicking investors. This time, however, the direction is positive—assets are now longer duration, extending risk if rates rise. Despite echoes of old warnings, today’s context is markedly different: Fannie and Freddie’s current holdings represent just 2% of the $8.5T US agency MBS market, a significant decline from their one-third share before the Great Financial Crisis. Market watchers like Walt Schmidt of FHN Financial argue that the risk is proportional to the smaller portfolios, but acknowledge the potential for substantial losses if recent rate volatility continues.

Why It Matters

The GSEs’ expanding duration gaps highlight the tension between policy ambitions and risk management. By filling their portfolios with longer-term MBS and limiting hedging, the agencies support lower mortgage rates—an explicit policy priority for the Trump administration ahead of the elections. Their growing role in housing finance also mirrors a broader resurgence in agency-backed lending, which recently helped push apartment loan volumes to record levels. However, these choices expose them to significant mark-to-market losses: Freddie’s filings indicate that a one percentage point rate move could cost $3.4B, with $1.6B at risk from just a half-point shift. This marks the largest exposure at either agency since the postcrisis clampdown began.

Though the agencies’ relative market footprint has diminished, their newfound willingness to accept greater balance sheet risk revives old anxieties about moral hazard and taxpayer exposure. As Scott Buchta of Brean Capital notes, the portfolios are still growing and ‘the risk exposure is expanding,’ leaving open questions about long-term oversight and resilience should conditions deteriorate. The current approach also means that volatility in Treasury and mortgage markets may be amplified if rapid rate moves force portfolio rebalancing.

Given housing affordability’s political centrality, the GSEs are now being used more transparently as policy instruments—even if that means revisiting exposures that once rattled Wall Street. With market observers split on whether these risks remain manageable, the sector is watching closely for signals of further expansion or regulatory intervention.

What’s Next

Many strategists expect Fannie Mae and Freddie Mac to keep expanding their retained holdings, with potential for their portfolios to grow by another $100B or more if existing policy priorities persist. This could push duration mismatches wider and raise the stakes for both the agencies and the broader MBS market. Should the Trump administration continue emphasizing lower borrowing costs, further intervention—including new buying mandates—remains very much on the table. Market participants will be monitoring not only headline duration gaps but also how regulatory agencies and Congress respond to a familiar but not forgotten form of systemic risk.