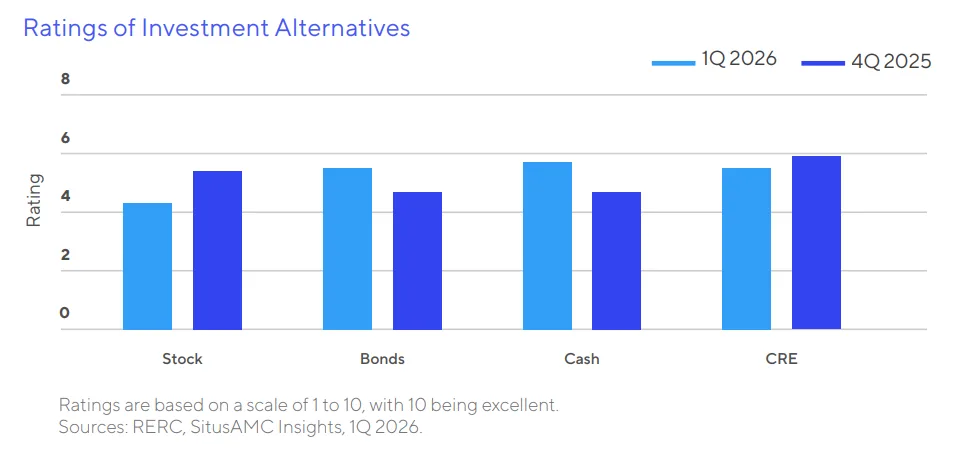

- Commercial real estate fell from the top spot among preferred asset classes in Q1 2026, tying with bonds while cash emerged as investors’ favorite allocation.

- Investors increased their preference to hold assets rather than buy or sell, while tighter underwriting and reduced capital availability weighed on transaction activity.

- Multifamily sentiment surged to a one-year high, while office showed signs of stabilization and hotel sentiment collapsed to its weakest reading in more than two years.

Globe St reports that commercial real estate investors are becoming more cautious after a brief burst of optimism late last year. New data from SitusAMC’s Q1 2026 ValTrends Report shows cash has overtaken CRE as investors’ preferred asset class, reflecting concerns that interest rates could remain elevated longer than expected and that the sector’s recovery is progressing more slowly than many anticipated.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Cash Takes the Lead

After leading investor preference rankings for three consecutive quarters, CRE slipped into a tie with bonds for second place, while cash moved into the top spot.

According to SitusAMC’s quarterly investor survey, investors cited slower recovery prospects, modest returns, and uncertainty surrounding inflation and interest rates as key reasons for the shift.

The report’s broader theme, “Recovery Interruptus,” highlights how repeated macroeconomic shocks continue to derail expectations for a sustained CRE rebound. This year, geopolitical tensions and rising energy costs have reignited inflation concerns, keeping pressure on borrowing costs and delaying hopes for lower commercial mortgage rates.

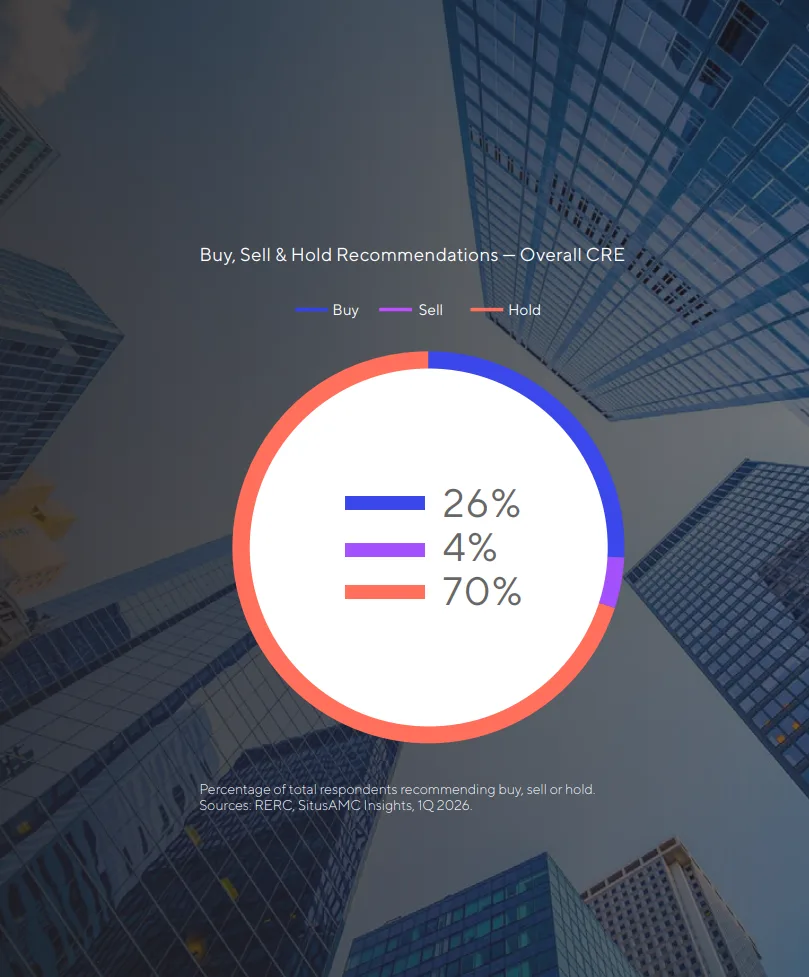

The Details

Investor positioning became noticeably more defensive during the first quarter. The share of respondents recommending a hold strategy jumped from 63% to 70%, while buy recommendations fell from 30% to 26%. Sell recommendations also declined, dropping from 7% to 4%, suggesting investors are opting to wait rather than actively reposition portfolios.

Capital markets conditions also tightened. Survey participants reported stricter underwriting standards and declining capital availability, with lenders increasingly favoring high-quality assets in top-performing markets. Many lenders now require lower loan-to-value ratios, recourse financing, and reserve holdbacks for future tenant improvements and leasing costs.

Meanwhile, CRE borrowing activity slowed. Mortgage Bankers Association data cited by SitusAMC showed commercial and multifamily borrowing fell 30% quarter over quarter, although volumes remained roughly 50% above year-ago levels.

Multifamily Leads While Office Stabilizes

Among property sectors, apartments emerged as the clear winner. Investor favorability jumped from 44% to 60%, the highest reading in a year. Investors pointed to multifamily’s relative stability and continued demand support from elevated homeownership costs and economic uncertainty. Multifamily remained the only major property type to receive an overall buy recommendation from survey respondents.

Office sentiment, while lower than the previous quarter, continued its gradual recovery. Favorability fell from 22% to 16%, but remained the second-highest reading since the pandemic began. Investors increasingly believe office values may be approaching a bottom, particularly for newer, well-located assets that have already undergone significant repricing.

Industrial sentiment also eased, dropping to 16%, while retail fell to 8%, its lowest level in nearly five years. Investors cited slowing demand, softer rent growth, and concerns about valuation levels across both sectors. Hotel sentiment was the weakest of all property types, falling to 0% as investors worried about travel demand, geopolitical instability, and higher transportation costs

A Market Searching for Conviction

The shift toward cash reflects a broader wait-and-see approach among institutional investors. CRE fundamentals have improved in several sectors. Property returns have also turned positive after a lengthy downturn. Even so, many investors remain unconvinced that a full recovery is near. That caution contrasts with other sentiment indicators that suggest investors still see underlying strength in commercial real estate.

Overall CRE posted a 4.9% trailing one-year return through Q1 2026, according to SitusAMC. That marks one of the strongest readings since 2022. However, rising Treasury yields continue to pressure valuations. Persistent inflation also weighs on sentiment. At the same time, tighter lending standards cloud the recovery outlook.

Why It Matters

Investor sentiment often serves as an early indicator of capital flows. The move toward cash suggests institutional investors are prioritizing liquidity and flexibility over risk-taking, potentially slowing transaction volumes and price discovery in the months ahead. At the same time, multifamily’s growing appeal and improving office sentiment hint at where capital could re-enter the market first once confidence returns.

What’s Next

The next phase of the CRE recovery will likely depend on inflation, interest-rate expectations, and capital availability. If Treasury yields remain elevated and lenders continue tightening underwriting standards, investors may maintain their defensive posture. However, sustained rent growth in apartments and improving sentiment around select office assets could create pockets of opportunity even as the broader market remains cautious.