- First American’s Q1 2026 data showed all-asset cap rates climbing to roughly 6.3%, up from 5.2% in late 2021 as higher interest rates continue reshaping CRE valuations.

- The spread between cap rates and the 10-year Treasury remains historically tight, suggesting cap rates could move even higher if bond yields stay elevated.

- Persistent financing volatility and slower price discovery are freezing transaction activity across commercial real estate markets, especially in sectors facing refinancing pressure.

Commercial real estate investors spent the last four years adjusting to a dramatically different interest rate environment. But according to new analysis from First American Financial Corp., the cap rate reset may still have further to run.

Globe St reports that the firm’s Q1 2026 Potential Cap Rate (PCR) Model showed the all-asset PCR increasing 10 basis points quarter-over-quarter to 5.8%, while actual market cap rates averaged closer to 6.3% to 6.4%. That marks a sharp increase from the roughly 5.2% average cap rate recorded in Q4 2021, when borrowing costs hovered near historic lows.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Higher, But Not Historically High

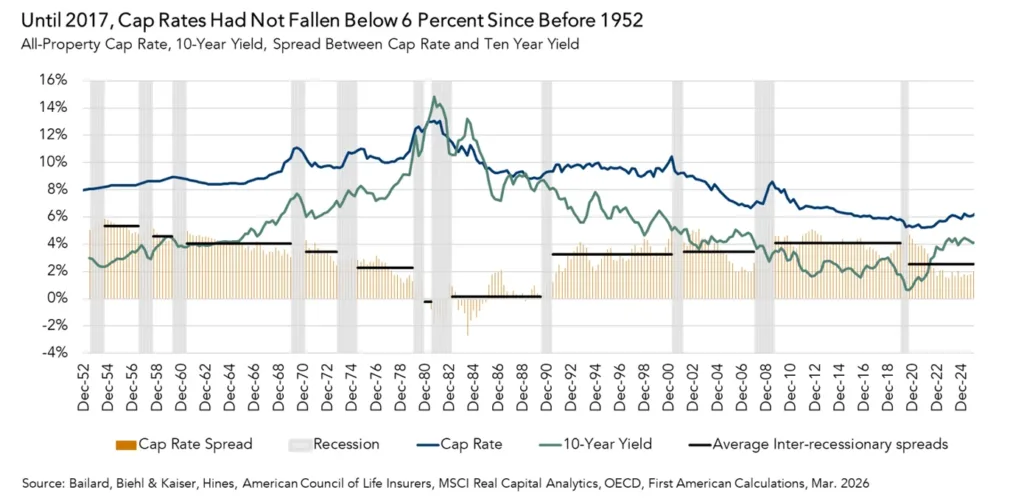

The recent move upward feels dramatic because cap rates spent much of the late 2010s and early 2020s below historical norms. According to First American economist Xander Snyder, cap rates below 6% were virtually unheard of before 2017, outside of the postwar era.

Today’s roughly 6.3% cap rate environment may feel elevated compared to pandemic-era pricing, but long-term comparisons tell a different story. With the 10-year Treasury yield sitting around 4.4% to 4.6%, the spread between CRE cap rates and risk-free government debt remains historically narrow.

That spread matters because Treasurys establish the baseline “risk-free” return investors compare against commercial real estate yields. Historically, investors demanded a larger premium to compensate for illiquidity, leasing risk, and operational complexity.

The Details

Snyder said cap rate spreads could still expand. He pointed to prior inter-recession averages as a benchmark. Under that scenario, all-asset cap rates could reach 7% to 10%.

First American’s PCR Model estimates cap rates using several market fundamentals. These include occupancy, rental income, interest rates, debt levels, and pricing trends. In Q1 2026, the model showed fundamentals supported lower cap rates. However, actual market cap rates sat roughly 60 basis points above PCR levels.

That disconnect reflects how rapidly capital markets changed after the Fed’s 2022 tightening cycle. Commercial real estate reprices far slower than bonds, since transactions take months to negotiate, finance, and close.

Treasury Volatility Complicates The Reset

Beyond higher base rates, Treasury market volatility is creating additional friction for buyers and sellers. Snyder argued that fluctuating yields increase financing uncertainty, making it harder for buyers to confidently underwrite acquisitions.

If loan pricing changes materially between due diligence and rate lock, buyers demand a larger margin of safety. That dynamic widens bid-ask spreads, suppresses transaction volume, and delays price discovery across the market.

The slowdown is already visible. Deal volume across multiple CRE sectors remains well below pre-2022 levels. Sellers continue anchoring to yesterday’s valuations while buyers underwrite more conservatively. Treasury volatility is also widening performance gaps between stronger and weaker CRE markets.

Why It Matters

The broader concern is what sustained higher cap rates mean for asset values. Because cap rates move inversely to property pricing, additional expansion would put renewed downward pressure on valuations across office, multifamily, retail, and industrial assets.

That risk is especially acute for owners facing near-term refinancing cliffs. Properties acquired during the low-rate years of 2021 and 2022 often relied on aggressive rent growth assumptions and cheap leverage that no longer exist in today’s market.

At the same time, higher-for-longer rates may have permanently lifted the floor for CRE pricing. Unless Treasury yields decline meaningfully, investors accept structurally tighter spreads, or NOI growth accelerates materially, a return to pandemic-era cap rates appears unlikely.

What’s Next

Investors are now watching three variables closely: Treasury yields, income growth, and credit spreads. If bond yields remain elevated while rent growth softens, the case for additional cap rate expansion strengthens.

The market may also continue splitting between high-quality and challenged assets. Properties with durable cash flow, strong locations, and limited near-term capital needs are likely to hold value better than commodity office buildings or overleveraged assets approaching refinancing deadlines.

For now, cap rates have clearly moved off their pandemic lows. The bigger question for CRE investors is whether today’s levels represent a new equilibrium—or simply the middle innings of a longer repricing cycle.