- REITs have posted positive total returns in more than 77% of both rising and falling interest rate periods since 1992, according to Nareit.

- Strong economic growth, rather than the direction of interest rates, has been a more decisive factor in REIT performance outcomes over time.

- Historical returns suggest REITs remain attractive for investors even during volatile rate environments, thanks to balance sheet strength and market access.

REITs Defy Rate-Driven Market Fears

In an environment where elevated or potentially rising interest rates have become the norm, many real estate investors are understandably cautious, questioning whether CRE can deliver strong returns. But as Nareit reports, fears of weak performance tied solely to interest rate levels often miss the mark.

Their recent analysis shows that listed REITs have historically logged positive total returns across a wide range of rate environments, consistently outperforming private real estate vehicles. This counters the market’s knee-jerk expectations that rising rates spell trouble for public real estate investments. Such results suggest that the interest rate narrative, while important, may be less predictive of performance than commonly assumed.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

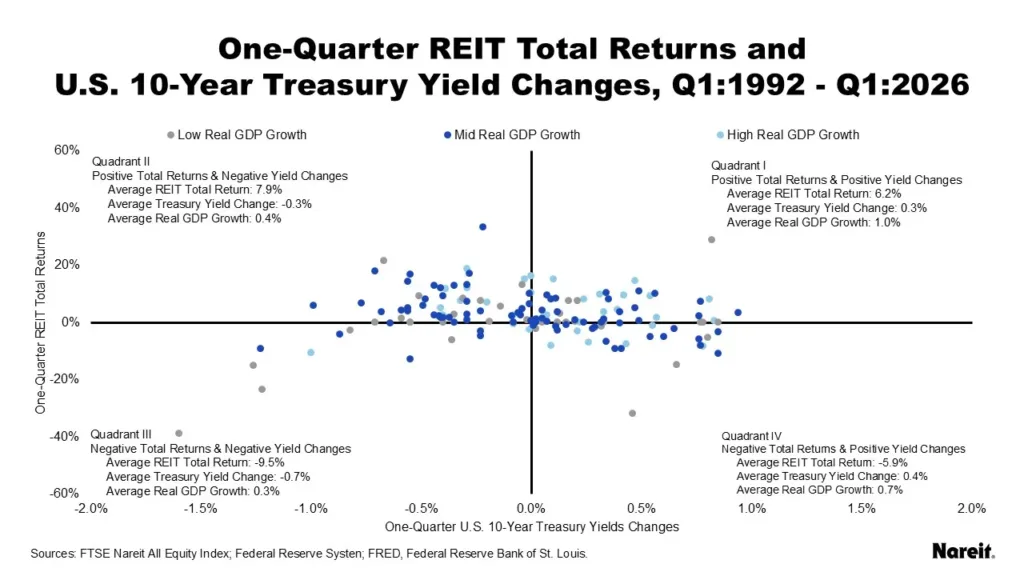

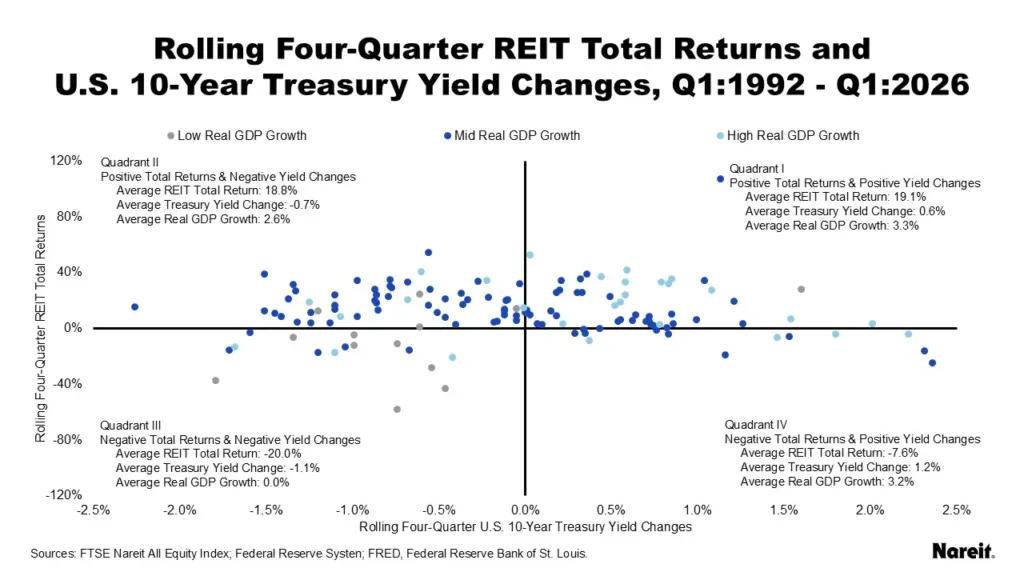

Digging into the data, Nareit’s review of rolling four-quarter periods from Q1 1992 through Q1 2026 found REITs produced positive total returns in 77.4% of rising interest rate periods and 78.7% of declining periods. Notably, during rising yield stretches (Quadrant I), the average four-quarter total return for the FTSE Nareit All Equity REITs Index hit 19.1%.

In comparison, REITs averaged an 18.8% total return in falling yield periods correlated with economic growth (Quadrant II). Conversely, weak economic conditions—most often paired with declining rates—delivered the poorest REIT returns, averaging -20% in the worst quadrant. Single-quarter analysis came to similar conclusions, reinforcing the trend across shorter time frames as well.

Economic Growth as the Deciding Factor

While the direction of the US 10-year Treasury yield has some bearing, it’s the health of the underlying economy that most directly drives REIT performance. According to the data, during periods of robust GDP growth (above 1% or 4% annualized thresholds), REITs put up stronger returns regardless of whether rates were climbing or declining. On the other hand, most poor REIT results occurred during stretches of low or negative GDP growth, and these periods coincided mainly with falling Treasury yields.

For example, Quadrant III (negative total returns and negative yield changes) saw average returns of -20% alongside near-zero GDP growth. Even on a one-quarter basis, the majority of weak economic periods—marked by GDP growth under 0.25%—surfaced in falling yield contexts, with average returns also negative.

Why It Matters

Given the industry focus on the impact of interest rate hikes—particularly the steady increases seen through 2023 and 2024—this analysis offers essential perspective. Despite persistent market anxiety, the evidence underscores that REITs are more resilient than the rate cycle alone would suggest. That aligns with recent market research showing CRE performs best when rate expectations remain predictable, even without aggressive Fed easing. Nareit’s findings show that listed REIT indices delivered positive total returns in over three-quarters of both rising and falling 10-year Treasury yield intervals from 1992 to 2026.

Notably, returns were highest in periods where rate increases coincided with robust GDP growth, averaging over 19% in four-quarter windows. In contrast, the worst results accompanied economic slowdowns, not just lower rates, where average annualized returns turned negative and GDP stagnated. This suggests that for CRE professionals and investors, monitoring macroeconomic expansion may be more useful than obsessing over the yield curve alone.

From a portfolio construction perspective, the asset class’s performance track record—regardless of rate direction—bolsters the argument for public real estate allocations within a diversified strategy. With operating experience, robust balance sheets, and access to capital markets cited by Nareit as additional strengths, REITs remain well positioned should current or future tightening cycles continue. The broader implication: focusing solely on rate direction likely shortchanges the true drivers of returns in listed real estate.

What’s Next

Looking ahead, investors and operators will continue to weigh interest rate direction, but this history suggests an even greater focus on macroeconomic signals and REIT fundamentals. As the US economy remains comparatively strong—and as REITs invest in operational expertise, prudent leverage, and capital access—the sector appears prepared to weather further volatility.

With the Federal Reserve’s path still uncertain and economic projections mixed for 2026, the interplay between growth and rates will remain in sharp focus. CRE advisors and portfolio managers may want to recalibrate their risk frameworks, emphasizing economic context over simple rate forecasting, as they navigate the next cycle.