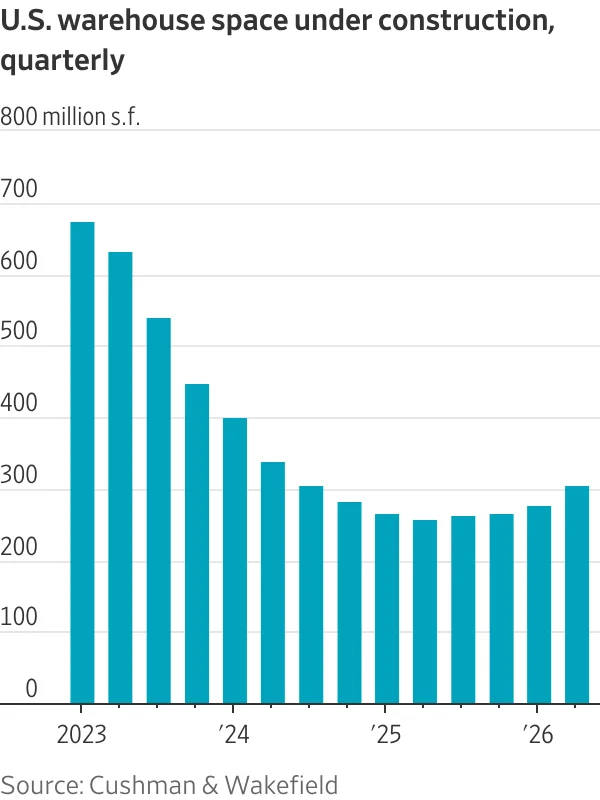

- US warehouse construction is rising, with 305M SF underway in Q2, marking an 18% annual increase, according to Cushman & Wakefield.

- The rebound follows two years of slumping demand and record-high vacancy, but leasing picked up sharply in Q2, signaling a possible turning point.

- Developers are now launching projects more cautiously, targeting real demand from sectors like data centers, logistics, and reshoring manufacturers.

Developers Respond to a Changing Market

Warehouse developers are getting back to work after a prolonged pause, breaking ground on projects they deferred during the 2024–2025 slowdown. According to The Wall Street Journal, more than 305M SF of warehouse space was under construction in the US as of Q2 2026. Cushman & Wakefield data shows this is an 18% increase compared to the previous year and the second consecutive quarter of annual growth. After two years on the sidelines due to excess vacancy and weaker tenant demand, builders like Prologis and Panattoni are repositioning their pipeline—this time with a sharper eye on real tenant needs rather than speculative supply.

This renewed developer activity reflects a notable turnaround from last year, when the nationwide industrial vacancy rate reached its highest level since 2013. Cushman & Wakefield puts much of the new confidence down to strong Q2 leasing activity, the best since mid-2022. Mark Russo, head of industrial research at Savills, told the Journal the market “has found its footing” after years of uncertainty about just how high vacancies might climb.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Pandemic-Era Expansion Paused, Now Recalibrated

The surge in new construction stands in contrast to the retrenchment that followed pandemic-era overbuilding. Per Cushman & Wakefield, the US industrial pipeline peaked at over 725M SF in Q3 2022 as e-commerce fueled a warehouse arms race. In 2024 and 2025, developers like Prologis and Panattoni cut back sharply, completing in-progress assets and working to fill empty spaces rather than break ground on new ones.

That two-year pause allowed supply to catch up and tenants—who had over-leased during the e-commerce surge—to shed surplus inventory. The recent resurgence is less speculative: Jason Tolliver of Cushman & Wakefield says developers are now “following demand, not chasing it.”

The Details

Prologis, the world’s largest industrial landlord, is upping its spending to $4.5B–$5.5B in new developments this year, up from $3.1B last year. Roughly 40% of these starts are dedicated to data centers, a direct play on the surging demand for AI-powered infrastructure. Privately-held Panattoni intends to increase new construction starts by 62% versus last year and is acquiring land for future projects.

On the leasing side, companies committed to more industrial square footage in Q2 2026 than at any time since mid-2022, bolstering developer confidence. Coastal gateway markets, which had been subdued, are seeing renewed interest, while Sun Belt metros like Houston remain robust, per Trammell Crow’s Jeremy Garner.

Leasing Momentum and Sector Shifts

Demand is coming from data center operators and their supply chain, retailers restocking ahead of potential tariff changes, manufacturers reshoring to US soil, and third-party logistics firms fulfilling outsourcing needs. Industrial landlords are benefiting as tighter conditions gradually shift negotiating leverage back toward owners in several major markets. These segments are driving what Cushman & Wakefield and Savills view as a more sustainable rebound than the pandemic-era boom.

Despite the momentum, the pipeline is running at less than half its pandemic peak. Ongoing economic concerns—including the possibility of higher interest rates if inflation persists, low consumer sentiment, and volatility in import patterns—are keeping some developers and tenants cautious. Still, companies like Trammell Crow see “green shoots” in markets that have lagged, with key players facing mounting pressure to make long-deferred space decisions and hedge supply chain risks.

Why It Matters

The uptick in new warehouse development signals renewed confidence in US industrial fundamentals, but with a more conservative bent than in the pandemic boom years. Developers, having learned hard lessons from oversupply and erratic demand, are now matching build-to-suit and spec projects to firm tenant interest and increasingly diversified end-users. For investors and capital providers, Cushman & Wakefield’s Q2 data showing a national vacancy recovery and leasing acceleration supports the thesis that industrial is stabilizing after a rocky patch.

Yet new headwinds persist. The Federal Reserve’s posture on inflation could keep borrowing costs from falling, impacting both user demand and construction economics. Consumer sentiment indexes remain near multi-year lows, and any sharp slowdown in import activity—especially later this year if companies front-load holiday inventory—could sap near-term warehouse absorption. However, long-term drivers remain intact. Henry Steinberg of EQT Real Estate notes that supply-chain volatility is prompting tenants to diversify locations and inventories, which could underpin steady if unspectacular warehouse demand even if broader economic growth slows.

The biggest storyline to watch may be the convergence of industrial and data center demand. With data centers accounting for a large slice of this year’s development pipeline, logistics landlords are positioning for the next secular growth wave, even as e-commerce normalizes.

What’s Next

The construction pipeline remains below its pandemic-era highs but is trending upward as developers take a cautiously optimistic stance. Cushman & Wakefield analysts expect industrial demand to stay resilient, especially from reshoring manufacturers and the booming data center ecosystem. However, significant new supply is not expected to reach 2021–2022 levels in the near term, with most players prioritizing fill rates and tenant pre-commitments over speculative risk. The Federal Reserve’s rate decisions and global supply-chain disruptions will continue to dictate the pace of development. All eyes are on upcoming Q3–Q4 leasing numbers and the earnings announcements from major logistics REITs like Prologis to confirm whether the recovery momentum holds through year-end.