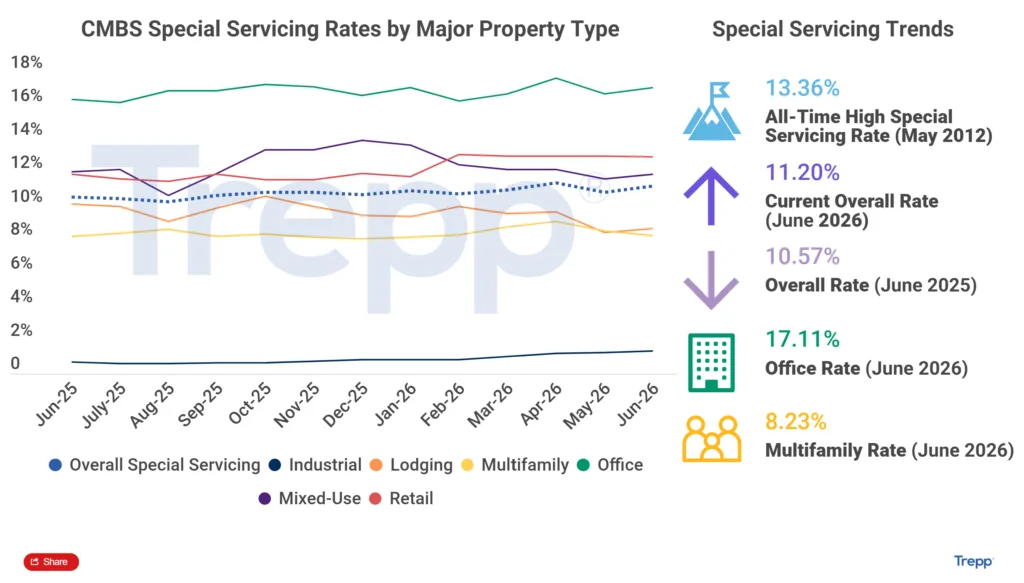

- The US CMBS special servicing rate rose 34 basis points to 11.20% in June, reversing May’s decline, per Trepp.

- Growth was driven by large new transfers in retail, office, and lodging, led by a $975M retail portfolio and a $430M hotel loan.

- Office distress remains severe at 17.11%, while multifamily posted modest recovery thanks to major loan resolutions.

Large Transfers Drive Special Servicing Uptick

The commercial mortgage-backed securities (CMBS) special servicing rate in the US climbed sharply in June, undoing the previous month’s improvement, according to Trepp’s June 2026 Special Servicing Report. The spike was predominantly attributed to a wave of large retail, office, and lodging loans entering special servicing. Notably, portfolio-level distress remains pronounced as lenders and borrowers navigate challenging refinancing and maturity environments, adding to the sector’s complexity.

Trepp reported that new special servicing transfers outpaced successful resolutions, with $3.08B of loans moved into special servicing against $1.16B of cures and payoffs. Retail, office, and lodging assets represented the core of new distress, highlighting sector-specific vulnerabilities that continue to challenge even the best-capitalized borrowers and experienced operators.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The Details

June’s jump in special servicing came from two major transfers. The $975M IMC Portfolio retail loan led the increase. The portfolio spans 9.6M SF across Las Vegas and High Point. The $430M Fairmont Austin hotel loan also entered special servicing.

The IMC loan received a modification in April after a $175M paydown. Lenders also granted a two-year extension. However, the loan transferred due to an approaching balloon maturity default.

The Fairmont Austin loan transferred despite remaining current on payments. The borrower used reserve funds for property taxes without approval. That move triggered a technical, non-monetary default.

Office loans also drove transfer activity. New additions included 26 Broadway, 79 Madison Avenue, and Champion Station. As a result, the office special servicing rate climbed to 17.11%.

Lodging rose 44 basis points to 8.89%. Industrial increased slightly to 1.37%.

Office and Retail Distress Outpaces Resolutions

Special servicing activity remained concentrated in sectors facing refinancing and maturity pressure. Office and retail loans represented a large share of balances in special servicing. Office continued to lead all major property types.

Several large Manhattan office and multifamily loans entered or exited special servicing. The moves highlighted stress across multiple sectors. The South Plains Mall loan in Texas illustrates the trend. The property was reappraised at $114M, down 69% from securitization levels. However, negotiations led lenders to approve an extension.

Meanwhile, the Yorkshire & Lexington Towers multifamily loan in Manhattan secured a broad modification after default.

Resolution activity remained limited. Only 15 loans, totaling $1.16B, returned to the master servicer or resolved during June. New transfers far exceeded that figure.

According to Trepp, four of six major property types posted higher special servicing rates. Only multifamily and retail improved slightly after several large extensions.

Why It Matters

The CMBS special servicing rate climbed to 11.20%, signaling continued stress in CRE credit markets. Refinancing options continue to shrink as values reset lower.

Office remains the biggest outlier. Its special servicing rate reached 17.11% despite a year of workouts and modifications. The figure sits well above long-term averages for both office and the broader market.

The slow pace of balance-sheet resolution remains a major challenge. Post-2010 CMBS 2.0+ deals reached an 11.13% special servicing rate, according to Trepp.

Lodging also appears increasingly vulnerable. The sector rose 44 basis points to 8.89%. Many borrowers exhausted reserves while revenue growth stalled. Technical defaults also increased as short-term modifications expired.

Retail remains under pressure despite a slight improvement. The sector’s special servicing rate fell to 12.95% in June.

Distressed sales remain uncommon. Most resolutions still come through extensions, forbearances, or new equity contributions. Trepp notes that technical defaults partly mask deeper distress. Many lenders remain unwilling to seize assets in a market with few buyers. That caution mirrors a broader divide in lending markets, where the largest banks have recently reduced CRE delinquencies while smaller institutions continue to face pressure.

Older CMBS 1.0 loans continue to post striking distress levels. Pre-2008 portfolios carried special servicing rates above 62% in June. Legacy structures and lower property values continue to weigh on performance.

Meanwhile, distress has spread into newer CMBS 2.0+ vintages. Even traditionally stable sectors now face pressure. The trend points to broader repricing and rising risk aversion.

What’s Next

Special servicing volumes will likely remain elevated through the second half of 2026. More loans will reach maturity without clear refinancing options. Asset values also remain volatile.

Lenders will continue to favor extensions, modifications, and forbearances over distressed sales. That preference will likely remain strongest for large trophy assets.

Investors should expect further increases in sector servicing rates. Office and hotel portfolios appear especially vulnerable.

According to Trepp, next quarter’s results will depend heavily on upcoming maturities. Capital markets demand for refinancing and distressed acquisitions will also play a major role.