- The majority of CRE investors surveyed by CREFC now have a neutral outlook on the market, a shift from earlier pessimism.

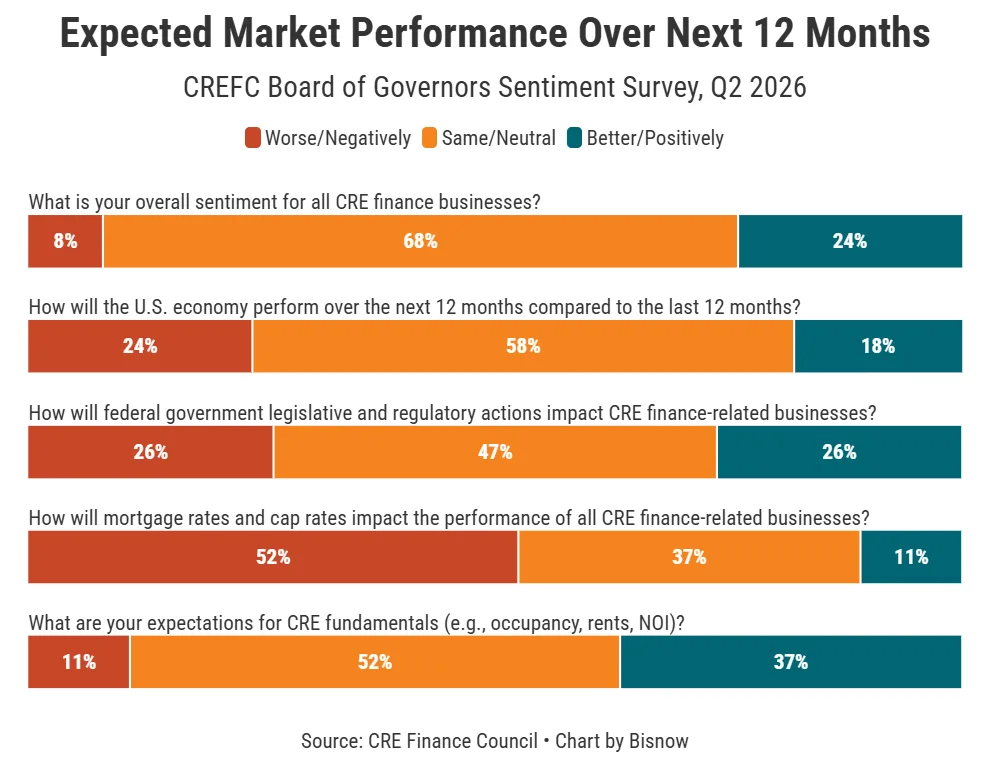

- Only 8% of respondents hold a negative view for the coming year, while higher-for-longer rates and geopolitical uncertainty continue to weigh on sentiment.

- Stable fundamentals in occupancy, rents, and NOI counterbalance a more cautious outlook on capital markets and transaction volumes.

Neutral Sentiment Becomes the Baseline

Commercial real estate’s top finance professionals are finding themselves in a holding pattern, according to Bisnow’s coverage of the latest Commercial Real Estate Finance Council (CREFC) Board of Governors survey. Market sentiment in CREFC’s second-quarter 2026 findings ticked just above its 2017 baseline, showing stability after a dramatic first-quarter drop that had previously soured investor outlooks.

Investors are now largely positioning themselves for a market defined by less conviction and expectation that status quo will persist. According to the survey, only 8% of respondents expect a more negative environment over the next year, while 24% are optimistic and a notable 68% are neutral — the highest neutral rating for any quarter since at least 2022. This signals broad industry acceptance that neither a sharp downturn nor a meaningful near-term rebound appears likely.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

The End of Mood Swings

The neutral tone marks a sharp shift from recent quarters. In CREFC’s Q1 2026 survey, 22% of respondents expressed pessimism. Many cited rate concerns and geopolitical risks.

That share has since fallen to just 8%. Meanwhile, 58% now expect the US economy to remain about the same next year. That figure stood at 34% in the prior quarter. The share expecting a worse year ahead dropped from 54% in March. The reversal follows a sharp sentiment collapse earlier this year, when investors braced for a far weaker outlook.

Transaction volumes moved alongside sentiment. JLL reported $113B in US CRE deals during Q1 2026, up 25% year over year. However, April sales volume fell 33% to $25B as rate pressures intensified.

By May, the market regained some momentum with $42B in sales, according to MSCI. Still, M&A activity drove most of the rebound rather than single-asset transactions.

Cautious Capital Markets Activity

Uncertainty around tariffs and US involvement in Iran continues to unsettle capital markets in 2026. Legislative risk remains another important variable.

Nearly half of survey respondents took a neutral view on pending government actions. The remaining respondents split evenly between positive and negative expectations.

The volatility also shaped expectations for borrower demand and liquidity. Only 45% of CRE investors expect stronger debt demand next year. That figure stood at 71% in March and 97% at the end of 2025.

Positive expectations for transaction demand also declined for the third straight quarter, according to CREFC.

Why It Matters

The move toward neutrality carries important strategic implications for CRE investors. Borrowers no longer expect refinancing delays to solve their challenges. Instead, they are adapting to higher rates that may persist for years.

Most respondents expect property fundamentals to remain stable. A majority of 52% expect occupancy, rents, and NOI to hold steady. Only 11% expect further deterioration. That marks the lowest negative outlook since mid-2024.

The capital stack also shows growing divergence. Most respondents remain cautious on mortgage rates and cap rates. However, confidence in liquidity and CMBS spreads remains relatively strong.

MSCI reported $42B in May transaction volume. M&A deals contributed $6.8B of that total. The figures highlight persistent pricing gaps in single-asset transactions.

The survey also points to measured expectations for artificial intelligence. Half of respondents expect AI to create sector-specific effects rather than market-wide changes. Only 13% expect AI to materially reduce office demand within a year.

The industry’s message is clear. Stability now matters more than volatility. Defensive positioning will shape investment strategies in the near term.

What’s Next

Transaction activity will likely remain flat through the rest of 2026. Investors continue adjusting to higher financing costs and macro risks.

Liquidity concerns appear manageable for now. Only 5% of respondents expect conditions in CRE credit markets to worsen.

However, borrower demand and transaction demand continue to soften. As a result, deal activity may remain uneven in the months ahead. Geopolitical tensions and monetary policy add further uncertainty.

For now, investors should expect neutral sentiment to persist. That outlook could change if major macro catalysts emerge.