- US office vacancy declined in 49 of 92 major markets during Q2 2026, marking the second straight quarter of improvement, according to Cushman & Wakefield.

- Office inventory continues shrinking as conversions remove obsolete buildings, tightening supply despite modest net absorption.

- The recovery is spreading beyond a handful of gateway markets, suggesting healthier leasing fundamentals across the broader office sector.

Commercial office fundamentals strengthened again during the second quarter, extending a recovery that is reaching more markets across the US.

According to Cushman & Wakefield, national office vacancy fell 10 basis points during Q2 2026, with 49 of the 92 markets it tracks reporting lower vacancy rates. The gains come despite ongoing economic uncertainty and point to a broader recovery fueled by steady leasing demand and a shrinking supply of older office space.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Office Recovery Broadens

The latest data suggests the office rebound is no longer limited to a few trophy buildings or coastal gateway markets. Cushman & Wakefield says vacancy has now declined for two consecutive quarters as tenants continue favoring high-quality properties. As premier space becomes scarcer, demand has started spilling into other Class A buildings. At the same time, obsolete offices continue leaving the inventory through redevelopment, helping improve market balance. David Smith, Cushman’s head of Americas insights, said the first half of 2026 demonstrated that office recovery has expanded beyond a small group of leading markets.

The Details

National vacancy declined 10 basis points during the quarter, while total office inventory contracted by 33M SF over the past five quarters. Cushman reports that roughly 90,000 apartments remain in the office-to-residential conversion pipeline, reducing available office supply in many cities. Twenty markets have removed at least 1% of their office inventory through conversions or other redevelopment efforts.

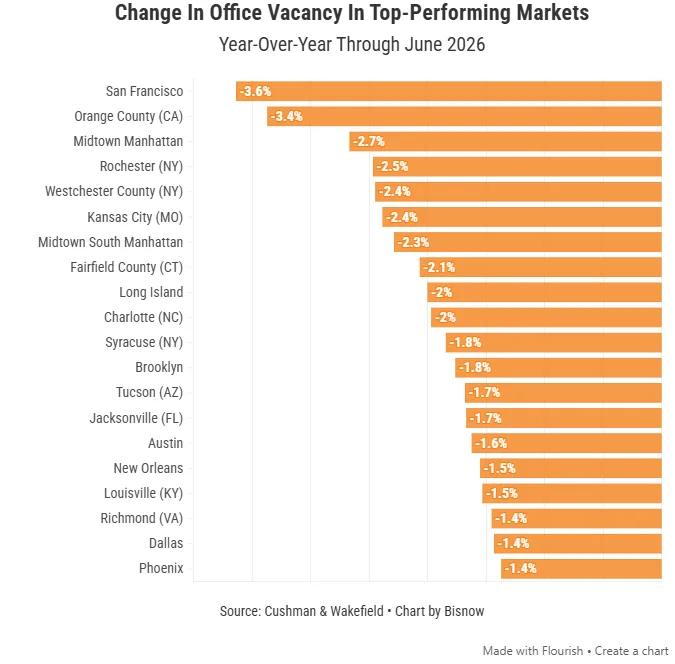

Leasing remains strongest in technology-driven markets. San Francisco, Orange County, and Midtown Manhattan posted the largest year-over-year vacancy improvements. Several secondary markets also ranked among the strongest performers, including Kansas City, Charlotte, Jacksonville, and Austin. San Francisco recorded a 364-basis-point occupancy gain, although its overall vacancy rate remains elevated at 30%.

Conversions Continue Reshaping Supply

Office-to-residential conversions remain one of the industry’s strongest recovery drivers. Removing outdated buildings has reduced excess supply and improved occupancy even as overall leasing activity remains measured. Cushman’s data shows shrinking inventory is helping offset weaker demand in certain markets.

Sublease availability also continues moving in the right direction. Available sublease space declined 15% year over year to 96M SF, its lowest level since early 2021. Historically, Cushman notes, falling sublease inventory has often preceded broader improvements in the office market as companies regain confidence in their long-term space needs.

Why It Matters

The latest figures suggest the office market is becoming healthier across a wider geographic footprint. Earlier in the recovery, leasing gains centered largely on trophy assets in a handful of coastal markets. Today’s improvement spans more than half of the country’s largest office markets, indicating demand has become more diversified.

Supply dynamics are also playing a larger role. Even though tenants posted negative net absorption of roughly 300K SF during Q2, Cushman revised prior quarterly figures upward, bringing rolling 12-quarter absorption to 14.3M SF. Combined with fewer sublease offerings and continued conversions, those trends point toward gradually improving occupancy across the sector.

What’s Next

Office fundamentals are likely to continue improving if conversions maintain their current pace and leasing demand remains steady. Cushman expects additional office-to-residential projects to enter the pipeline, further reducing outdated inventory. Investors will also watch whether technology hiring, AI-related leasing, and expanding tenant demand continue supporting recovery outside traditional gateway markets.

Not every city is improving at the same rate. Cleveland posted the largest year-over-year vacancy increase, while Boston, Oklahoma City, Seattle’s Eastside, and Downtown Los Angeles also recorded weaker performance. Still, the broader trend indicates the office recovery is becoming more durable as supply and demand gradually move back into balance.