- Newmark’s research found commercial real estate generated its strongest forward returns during periods of stable Fed policy rather than rate-cutting cycles.

- The analysis argues that Fed rate cuts often coincide with weaker economic conditions, limiting the benefit of cheaper financing for property owners.

- Slowing job growth and productivity-led economic expansion could reshape how investors underwrite assets and allocate capital over the coming decade.

Many CRE investors have treated lower interest rates as the key to restoring deal activity.

According to Newmark, history points to a different conclusion. The firm’s research suggests stable rate environments have produced stronger long-term returns than periods when the Federal Reserve was cutting rates.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

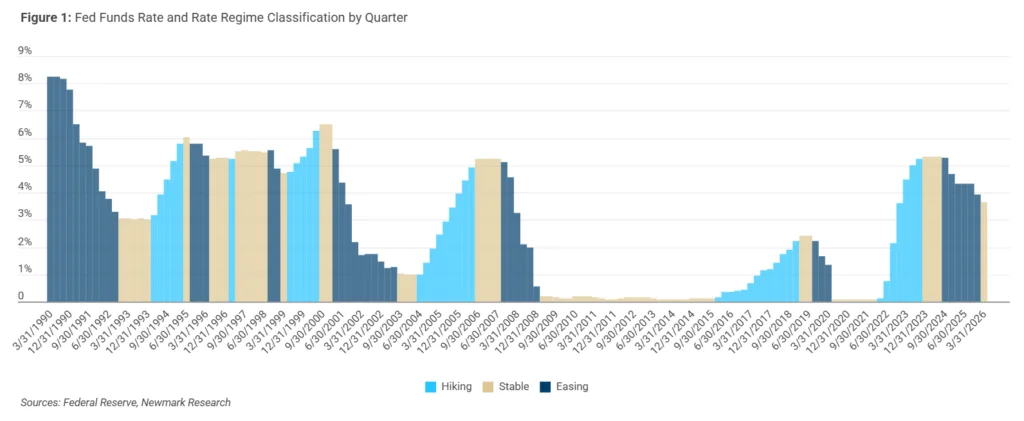

Stable Rate Periods Delivered Better Returns

For years, lower borrowing costs have been viewed as the catalyst for stronger CRE performance. Newmark’s latest research challenges that assumption by separating the effect of interest rates from the economic conditions that usually accompany them.

Using NCREIF data spanning 1990 through 2023, the firm found stable Fed policy consistently produced the strongest three-year forward returns. According to Newmark, easing cycles often begin as economic conditions weaken, reducing investor confidence, slowing capital flows, and limiting appreciation despite lower financing costs. The report argues that economic fundamentals matter more than borrowing costs alone.

The Details

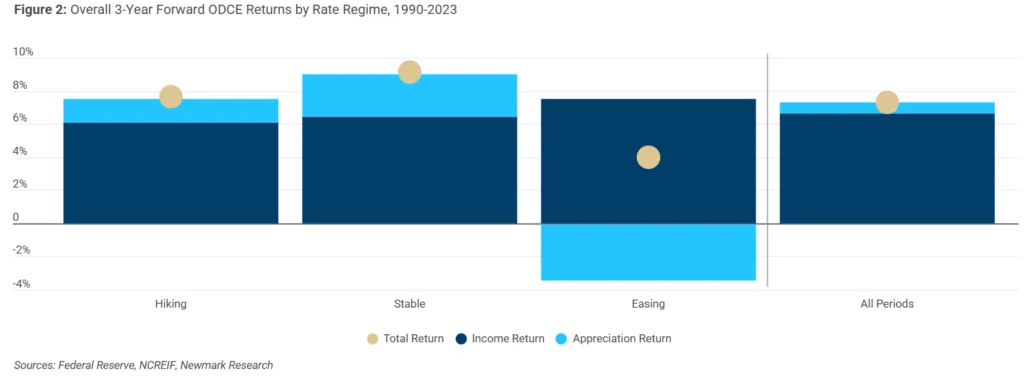

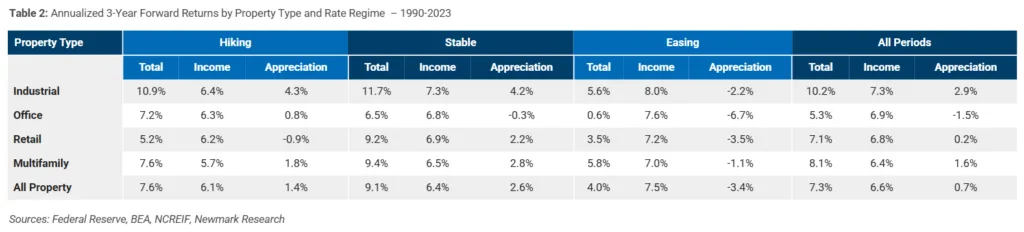

Newmark found commercial real estate returned an average of 8.3% over the three years following periods of stable Fed policy. That compares with 6.9% after rate hikes and just 3.0% following Fed rate cuts, according to data cited by Bisnow.

The relationship held across office, multifamily, industrial, and retail assets after accounting for GDP growth and property type. Joe Biasi, Newmark’s head of capital markets research, told Bisnow that lower borrowing costs help investors mechanically. However, deteriorating labor markets and weaker investment activity typically outweigh those benefits once the Federal Reserve begins easing policy.

Slower Growth Changes The Investment Playbook

Newmark argues the next challenge extends beyond interest rates. Demographic trends are slowing labor force growth, reducing the employment gains that historically supported demand across many property sectors.

The firm’s research cites Federal Reserve analysis showing break-even job growth has fallen close to zero because of aging demographics and slower immigration. At the same time, productivity improvements, including those driven by artificial intelligence, may support GDP growth even if payrolls remain flat. That shifts investor attention toward assets leased to tenants capable of expanding profits through productivity rather than workforce growth alone.

Why It Matters

The findings challenge one of commercial real estate’s most common assumptions. Lower rates may improve financing conditions, but they rarely arrive in healthy economic environments. Investors relying on monetary easing to lift valuations could face weaker leasing demand, slower transaction activity, and reduced capital appreciation.

The research also reinforces the importance of asset selection. According to Newmark, properties with durable cash flows, pricing power, and high-quality tenants may outperform if economic growth increasingly depends on productivity instead of employment gains. That could favor sectors and markets supported by strong tenant fundamentals rather than broad labor expansion.

What’s Next

The market’s outlook will depend on inflation, Federal Reserve policy, and economic growth over the remainder of 2026. Persistent inflation has already complicated expectations for rate cuts, while several Federal Reserve officials have signaled rates could remain elevated longer, according to Bisnow.

Rather than waiting for cheaper debt, Newmark believes investors should underwrite deals based on rent growth, tenant quality, and long-term operating performance. If slower job growth becomes the new normal, commercial real estate strategies may shift away from betting on interest rates and toward owning assets positioned to grow regardless of the next Fed decision.