- US average apartment rents rose 0.1% in June, with San Francisco leading among major metro areas at 0.7% monthly growth.

- The national average rent reached $1,742, while annualized gains slowed to 0.8%, down from 1.2% a year prior.

- Surging supply still pressures rents, especially in the South and Mountain regions, while tech-heavy Bay Area markets outperform.

Subdued Spring Caps Sluggish Growth

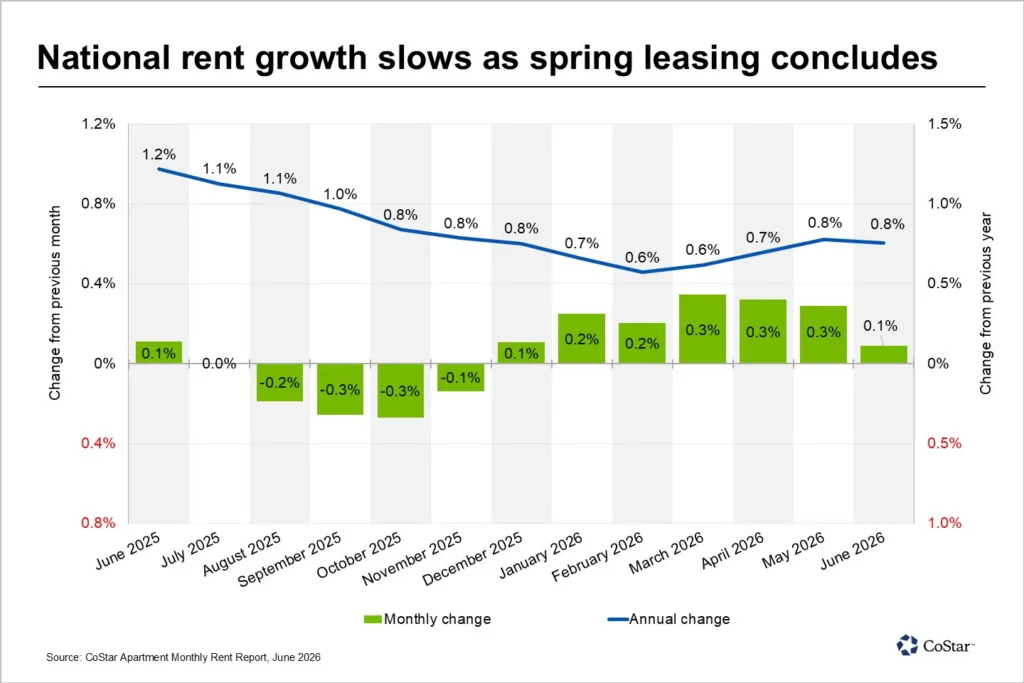

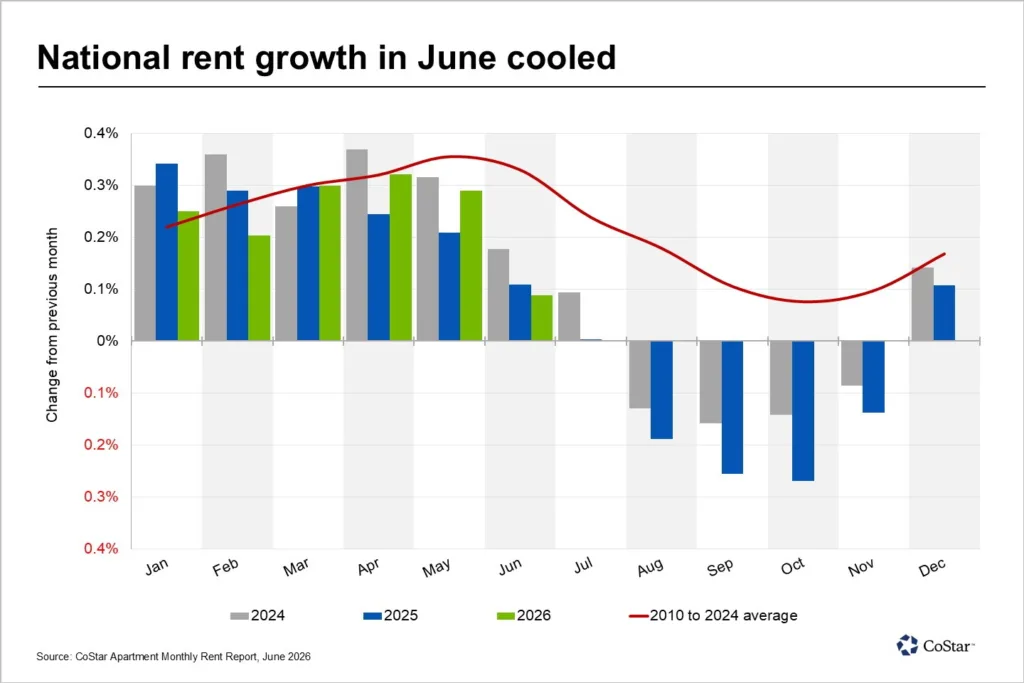

The apartment market ended the spring leasing season on a muted note, as US rents inched up an average of 0.1% in June, per CoStar Analytics. This modest increase lifted national average rents to $1,742, up just $2 from May’s revised $1,740. Despite seasonal expectations for stronger leasing activity, supply overhang and restrained demand weighed on pricing, with elevated inventory still keeping a lid on momentum nationwide.

CoStar Analytics’ most recent data shows that while monthly rent gains have stabilized since late 2025, year-over-year rent growth hit only 0.8% in June. This remains below the 1.2% annual gain logged for June 2025, reflecting persistent headwinds for the multifamily sector. While the Pacific region posted the highest monthly gains, overall national growth remains sluggish compared to previous years.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Construction Surges Cool Rent Gains

Developers slowed groundbreakings in many markets starting in early 2026, but a substantial pipeline of new deliveries continues to challenge landlords. CoStar’s analysis notes that broad inventory growth, especially across the Sun Belt and Mountain metros, has left several markets working through an inventory surplus. While construction activity is gradually easing, newly delivered units in supply-heavy markets continue to exert downward pressure on rent growth, undercutting gains even in typically robust leasing windows. This softer backdrop mirrors broader signs that apartment demand and pricing momentum remained subdued entering the 2026 spring season.

In prior high-growth periods, spring leasing often fueled sharper rent hikes. The underperformance this year highlights a market that is shifting focus from relentless expansion to stabilizing occupancy and moderating concessions amid economic uncertainty and cooling renter demand.

The Details

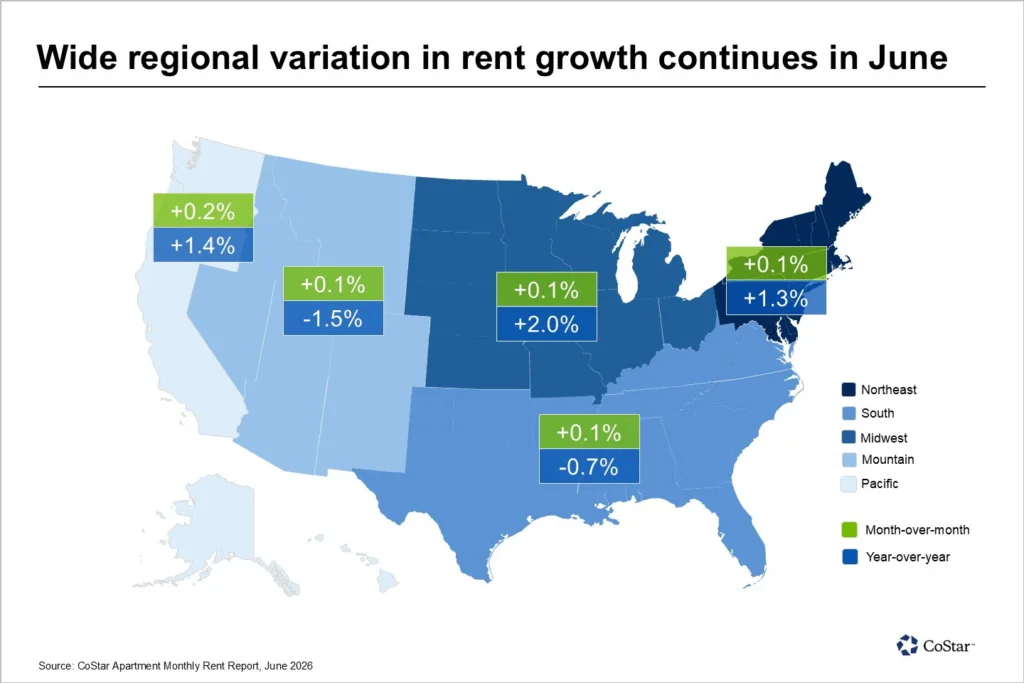

All five major US regions posted average rent increases in June, with the Pacific region in front at 0.2%. The Midwest, South, Northeast, and Mountain regions each saw 0.1% monthly gains. National annual rent growth clocked in at 0.8%—steady with May, but a marked slowdown from 2025.

San Francisco led major metros in monthly rent growth for June with a 0.7% gain, surpassing other Bay Area hubs San Jose (0.6%) and East Bay (0.4%). CoStar attributes this regional strength to surging demand tied to the local AI and tech sectors. Conversely, nine large markets posted declines, led by Fort Lauderdale, Florida (-0.3%) and Richmond, Virginia (-0.2%). Overall, 41 of the top 50 metros saw rents rise month-over-month, slightly fewer than the previous month.

Regional Disparities Persist

Rent growth remains uneven across US regions. Annualized, the Midwest leads with a 2% gain, followed by the Pacific (1.4%) and Northeast (1.3%). The South (-0.7%) and Mountain regions (-1.5%) continue to see year-over-year declines, reflecting the impact of heavy new supply. Markets like San Antonio, Denver, Austin, and Phoenix are all dealing with excess inventory and posted annual rent drops between 2.3% and 3.4%.

By contrast, the Bay Area stands out for outperformance: San Francisco rents are up a sector-leading 9.2% year-over-year, with San Jose (5.6%) and East Bay (3.1%) also showing strong momentum. This divergence underscores how concentrated job and wage growth—particularly in tech—can supersede broader national headwinds.

Why It Matters

For multifamily investors and operators, the sluggish rent growth of spring 2026 sends a clear signal: supply-demand imbalances are still the overriding theme in most markets. According to CoStar, despite some regional standouts—including the Bay Area—broadly higher vacancies and abundant new deliveries are tempering landlords’ pricing power.

New lease signings are no longer commanding the premiums seen during the peak pandemic rebound. Instead, rent appreciation has flattened across much of the country, forcing many owners to compete via amenities, concessions, or more flexible leases. The South and Mountain regions, long the top performers, now appear most at risk of negative rent growth due to continued inventory surges and shifting migration patterns.

Meanwhile, the resilience of the San Francisco market—helped by deep tech sector demand—demonstrates the enduring value of constrained, high-opportunity metros even in slower cycles. For developers, the lesson is clear: future groundbreakings must be more closely aligned with true market absorption rates. Oversupply in secondary markets will likely prolong the current period of underwhelming rent growth and fuel continued bifurcation between high- and low-demand regions.

What’s Next

Heading into the second half of 2026, CoStar anticipates that national rent growth will remain muted, barring a notable shift in absorption or a sharp slowdown in new deliveries. Inventory is expected to peak in several Sun Belt and Mountain markets during the coming quarters, before trailing off as project pipelines dry up. Observers should watch for stabilization first in supply-constrained coastal markets, where strong labor markets buoy rents. Nationwide, only tighter underwriting and recalibrated development schedules can restore balance—suggesting investors should brace for a slow, uneven recovery in multifamily rent growth through at least early 2027.