- CMBS lodging’s purported recovery is a compositional illusion; disaggregated data reveals deepening risk in limited-service hotels.

- Extended stay hotels have structurally de-risked, full-service hotels have stagnated, and limited-service is entering a new cycle of deterioration.

- The next stress point for the sector is the looming maturity wave of modified limited-service loans, not a broad market shock.

CMBS Lodging’s Divergent Recovery Five Years After COVID

Aggregate numbers suggest US CMBS lodging has nearly clawed back to pre-pandemic occupancy and delinquency rates. But a microscope on subtype data tells a sharply different story: the sector is fractured between structurally de-risked extended stay hotels, full-service assets stuck in a new, lower equilibrium, and limited-service properties showing renewed signs of distress. According to Trepp’s May 2026 data, the recovery headlines are glossing over pronounced risks accumulating in particular segments and markets.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Lodging’s Precedent as CRE’s Credit Canary

Historically, lodging leads commercial real estate’s credit cycle. During the global financial crisis, hotel CMBS delinquencies spiked roughly two years before distress rippled into office, retail, and industrial. The pandemic reversed quickly—the sector initially bounced twice as fast as after the GFC—but today’s apparent stability is masking bifurcated realities beneath the surface. The big question for underwriters is whether the sector’s current plateau signals a new equilibrium or conceals another wave of stress.

The Details

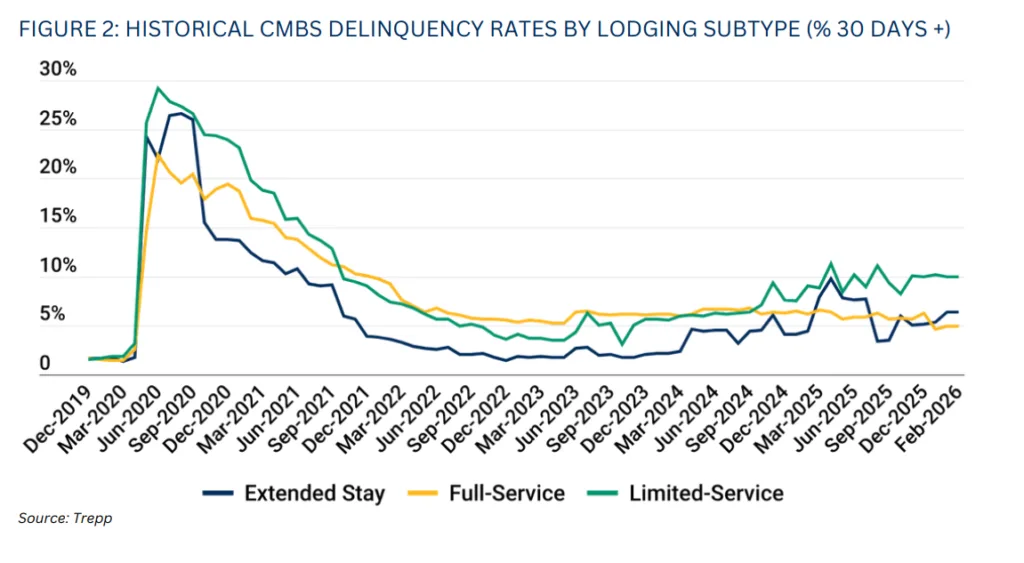

Trepp data highlights the diverging trajectories of the three major lodging categories. Extended-stay hotels recovered the fastest after the pandemic. Delinquencies fell below 5% by mid-2021 and now sit at a normalized 5–6% range. Persistent demand from remote workers, traveling nurses, and insurance-related relocations has supported performance and reduced credit risk.

Full-service hotels have struggled to regain momentum. Delinquencies remain between 5% and 7%, roughly matching 2021 and 2022 levels. Weak group travel and convention activity continue to weigh on results. Occupancy also remains 7–8 percentage points below 2019 levels, with little evidence of a meaningful rebound.

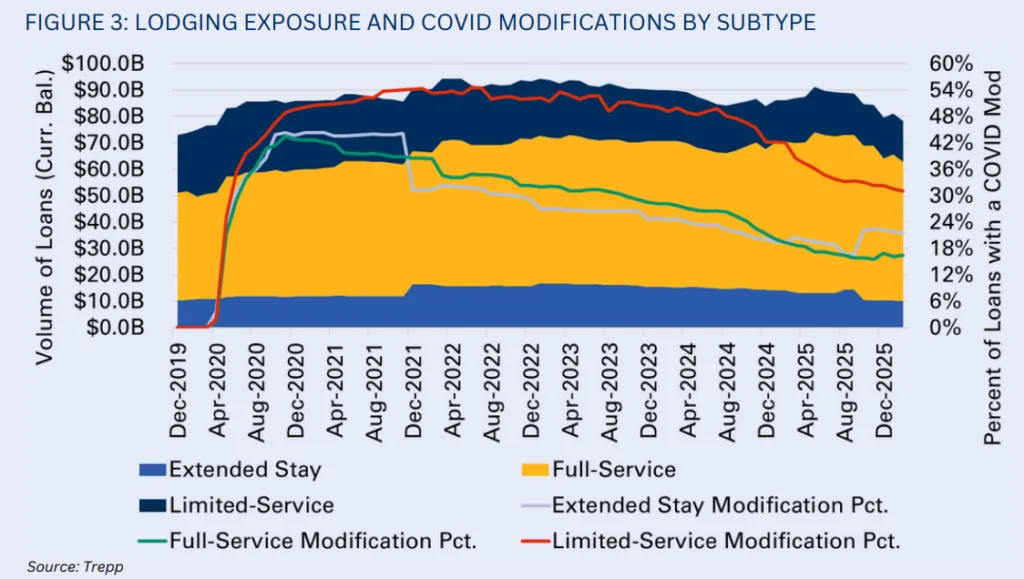

Limited-service hotels face the most concerning outlook. After stabilizing at 4–6% delinquency rates during 2023 and 2024, distress has started to rise again. Stagnant RevPAR, deferred capital spending, and increasing delinquencies are creating a negative cycle. Higher borrowing costs have only added pressure. Nearly 30% of loans in this segment still carry modifications, compared with less than 20% in the other lodging categories.

Composition Effects Mask Real Risk

The sector-wide delinquency rate has improved mostly because distressed assets exited the CMBS pool and high-performing hotels entered. On a same-store basis, no major market has recovered occupancy across all subtypes. Extended stay’s solid overall numbers are concentrated in Sunbelt and Midwest markets like Dallas and Houston, whereas New York and San Francisco lag. Full-service hotels in cities like Philadelphia, San Francisco, and Houston remain 10–17 points below pre-pandemic occupancy. Limited-service performance swings widely by MSA but has generally stagnated, with pockets of deeper underperformance driving aggregate risk.

Why It Matters

The maturity wave for limited-service hotels is materializing as modified loans approach their extended due dates but lack the operating fundamentals to refinance or qualify for further extensions. According to Trepp, this group makes up nearly one-third of limited-service lodging exposure. These developments indicate that new losses and special servicing transfers are a question of “when,” not “if.” Investors relying on aggregate metrics risk missing localized and subtype-driven vulnerabilities. That aligns with broader investor behavior, as many institutions are taking a more defensive stance and increasing cash allocations amid growing uncertainty across commercial real estate.

What’s Next

The CMBS lodging sector will likely see more special servicing transfers and liquidations. Limited-service hotels face the greatest refinancing pressure as maturities approach. Extended-stay properties should remain resilient in select Sunbelt and Midwest markets. However, investors should stay cautious in coastal and high-cost metros, even within that segment. The biggest underwriting challenge now sits at the property, market, and subtype level. Sector-wide averages increasingly mask meaningful differences in performance. For lenders and active managers, stress-testing limited-service portfolios should remain a top priority through 2027.