- Data center demand is booming, fueled by cloud, AI, and data sovereignty, with capacity projected to approach 200 GW globally by 2030.

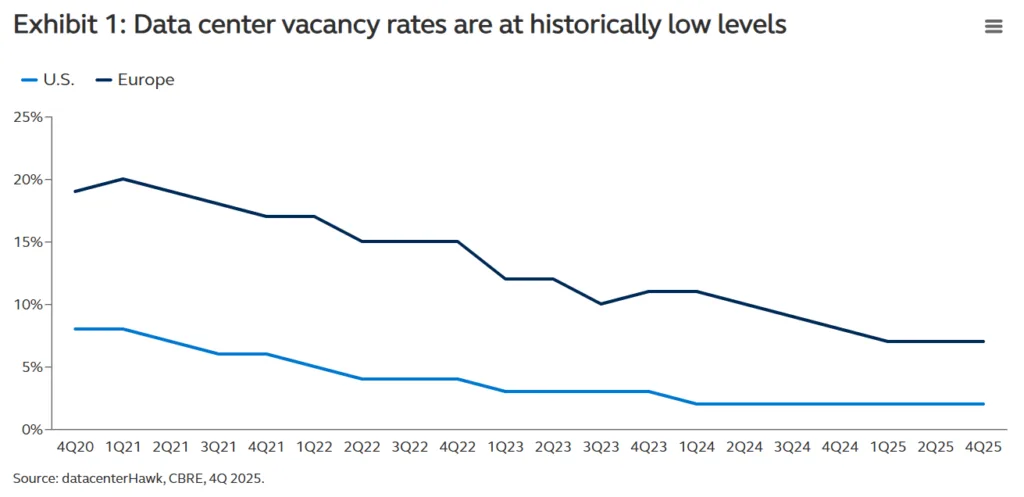

- Vacancy rates in primary US and European markets remain at historic lows as utility and permitting constraints limit new development.

- Stable, infrastructure-like returns are attracting investors, but success now depends on securing power, permits, and disciplined risk management.

Structural Changes Redefine Data Center Investment

Principal Asset Management reports that investors eyeing data centers face a sector in transformation, shaped by five structural shifts in demand, supply, leasing, capital needs, and development complexity. Surging data generation and evolving technology are keeping demand on an upward trajectory in 2026, but tight supply and infrastructural hurdles are raising the stakes for new entrants.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Historic Supply Constraints Squeeze Capacity

Chronic undersupply is a defining feature of today’s data center market. Per CBRE and datacenterHawk data from Q4 2025, US and European vacancy rates have rarely been lower. Development timelines are stretching, with utility hook-ups now taking 24–48 months compared to 12–18 months historically. Growing power and permitting constraints, compounded by surging AI and manufacturing-related load, are inhibiting the pace of new supply.

Pre-Leasing Drives Lease Certainty and Cash Flow Stability

Hyperscale and enterprise tenants now routinely commit to data center space years in advance, locking in 10–20-year leases. According to sector data, new facility pre-leasing rates frequently hit 70–90% in leading markets, improving income predictability for investors. Developers tailor designs to tenant needs, which drives long lease terms but also raises capital intensity and requires disciplined underwriting.

Capital Must Come Sooner and Smarter

Investors capture the strongest returns by deploying capital earlier in the development cycle. Early investment offers greater upside potential. However, it also demands stronger risk management and careful partner selection. Execution discipline matters more than ever. Developers who secure power and permits in constrained markets hold a clear advantage. Experienced financial sponsors also benefit from their sector knowledge and relationships.

Why It Matters

Data centers now form the backbone of digital infrastructure. Growth extends far beyond AI demand alone. Industry data shows digital data creation has increased 19,600% since 2010. Analysts also expect the sector to grow 14% annually through 2030. These trends make data centers one of CRE’s strongest long-term investment themes. Similar supply-demand imbalances are emerging elsewhere. Student housing operators, for example, report weaker pre-leasing activity than recent years. Long leases and hyperscale tenants support stable cash flows. As a result, many investors view data centers more like infrastructure assets. That stability helps reduce exposure to short-term technology cycles.

What’s Next

Expect more capital to flow into data center development, especially from investors prioritizing power-secured, well-permitted projects. With utilities forecasting grid load growth of nearly 16% over the next five years—a pace six times historical experience—the bottleneck will be site and utility access, not tenant demand. Construction delays and creative retrofits will define the immediate pipeline. CRE players should watch for emerging secondary markets and evolving pre-leasing standards as the sector adapts to longer timelines and greater capital intensity.