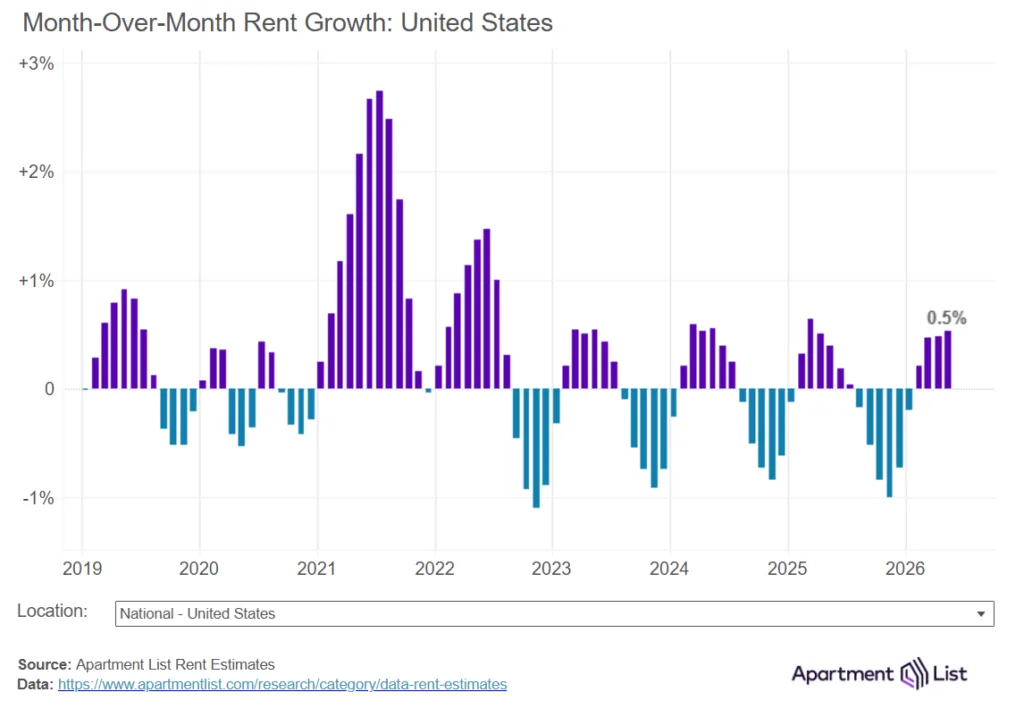

- US median rent climbed 0.5% in May to $1,379, marking the fourth straight monthly increase.

- Despite the uptick, national rents are still 1.5% lower compared to May 2025 and remain 4.4% below the 2022 peak.

- The multifamily vacancy rate declined to 7.2%, the first drop in over four years, but market conditions remain muted amid ongoing supply pressures.

Rents Edge Up as Leasing Season Heats Up

The US apartment market saw the national median rent rise 0.5% to $1,379 in May, marking the fourth consecutive month of increases as leasing activity picked up for the summer season, according to Apartment List’s May 2026 National Rent Report. Although rental prices are up from earlier this year, the national median remains 1.5% cheaper than in May 2025 and stands 4.4% below the 2022 peak.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

Surplus Supply Caps Rent Growth

Rents are following usual spring and summer patterns, but the market’s annual rent growth remains near decade-lows due to persistently high supply. The record wave of multifamily construction peaked in 2024, with more than 600,000 new units delivered— the most since 1986. Although this pipeline has slowed, the market’s absorption rate is still struggling to match new inventory, keeping a lid on rent growth and pushing seasonal patterns toward weaker annual results.

The Details

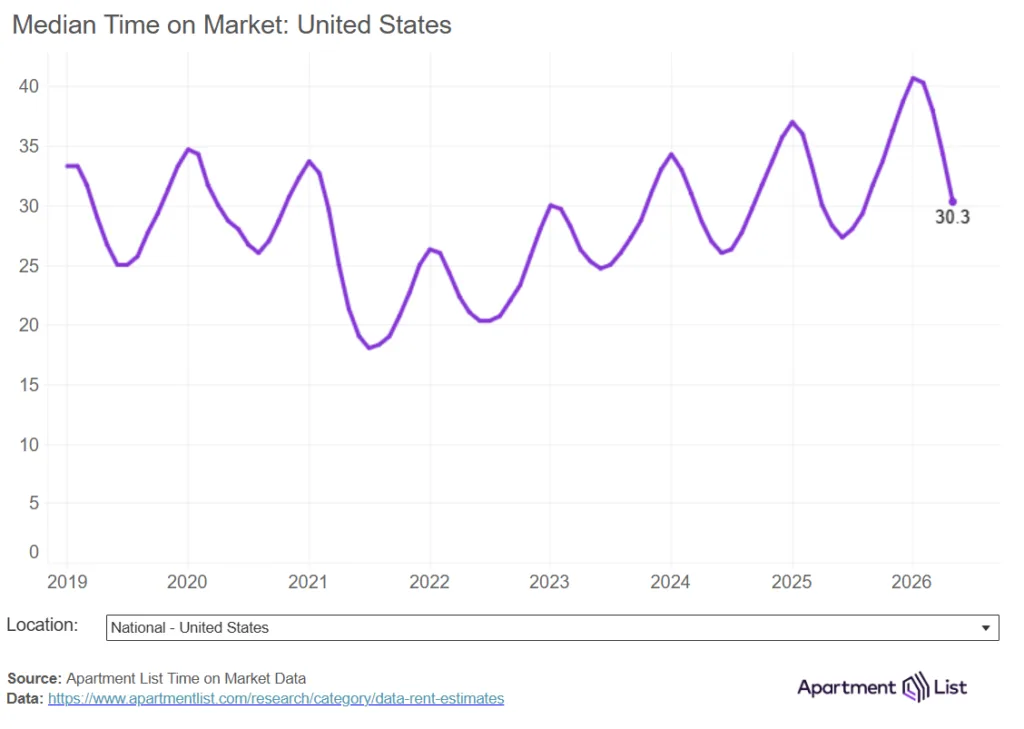

Median rent nationally is currently $1,379, down $20 compared to this month in 2025. Rents are now 20% higher than at the start of 2021. The national multifamily vacancy rate fell to 7.2% in May after peaking at 7.3% in February, marking the first decline since late 2021. Units are taking an average of 30 days to lease, down from 34 days in April, but still longer than at the same time last year.

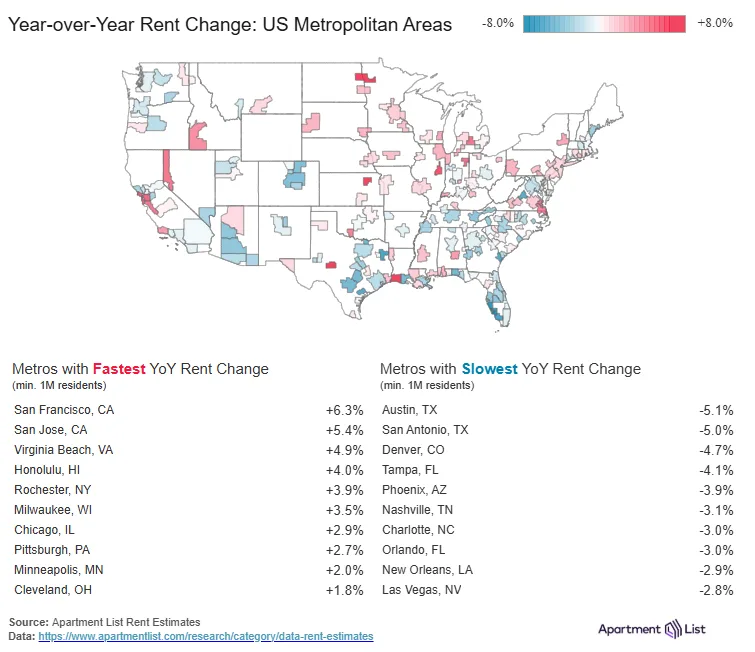

In metro-level trends, Austin recorded the steepest annual rent drop among large cities, falling 5.1% over the past year, while San Francisco leads for annual growth with a 6.3% gain.

Regional Disparities Persist

Year-over-year rent declines are most acute in the Sun Belt and Mountain West, where Austin’s supply surge has made it the hardest-hit major market. Other high-supply metros such as San Antonio, Denver, Phoenix, Tampa, and Nashville are also seeing year-over-year declines. In contrast, the Bay Area is leading growth due to tech-sector demand, and several Midwest cities are posting steady gains, aided by relative affordability. Meanwhile, stronger tenant demand and limited new supply have kept retail fundamentals comparatively stable in many markets.

Why It Matters

While the slight drop in vacancy and moderate rent increases indicate some stabilization, market fundamentals remain weak relative to historical norms. Elevated supply, slow lease-up times, and wider economic uncertainty suggest the sector could face ongoing challenges even as headline rents tick up during peak season. According to Apartment List data, this is the third consecutive year with negative annual rent growth, with average lease-up times still above any May since 2019.

What’s Next

Looking forward, the rental market’s trajectory will hinge on its ability to absorb persistent new supply and on macroeconomic factors like job growth and inflation. If current trends hold, vacancy may plateau at high levels rather than return to historical lows. Keep an eye on whether deceleration in delivery volume and the summer leasing rush can bring the market meaningfully back toward balance. Analysts and investors should watch regional shifts, especially in supply-heavy Sun Belt metros, as an early signal for national direction.