- US apartment rents rose 0.2% in May, matching April’s pace as the spring leasing season remained relatively subdued compared with historical trends.

- San Jose, San Francisco, and several Midwest and Northeast markets posted the strongest rent gains, while supply-heavy metros such as Austin, San Antonio, and Denver continued to see annual declines.

- A large pipeline of recently delivered multifamily units is still weighing on pricing power nationwide, even as new construction activity begins to slow.

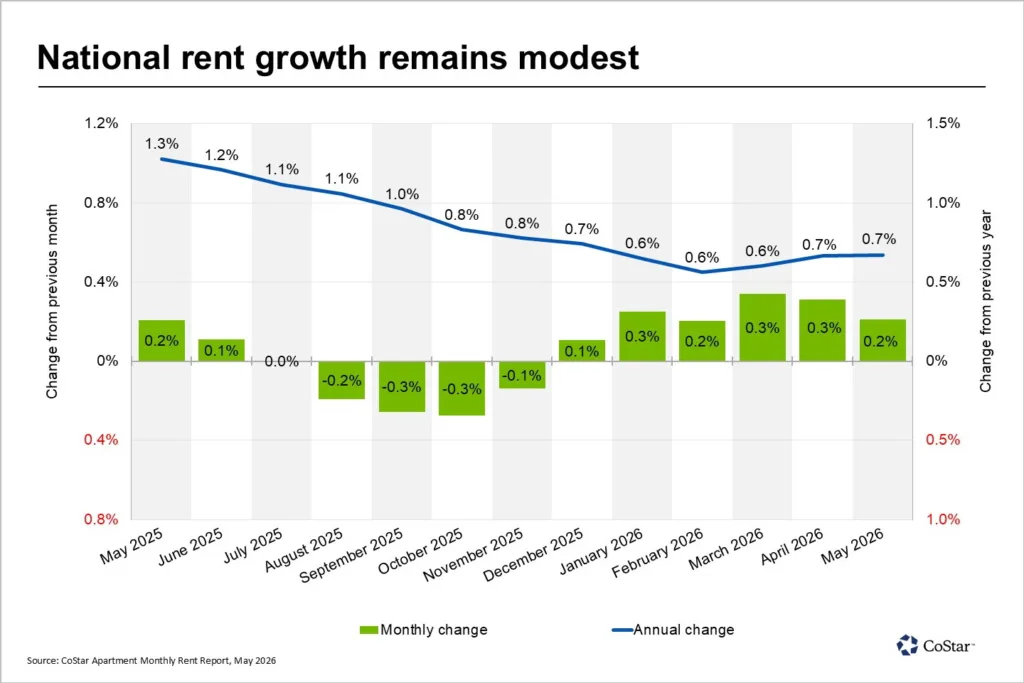

US apartment rents continued their gradual climb in May, extending a string of modest gains that began late last year. According to Apartments.com data reported by CoStar Analytics, average monthly rents increased 0.2% to $1,737, up from April’s revised average of $1,733. While pricing remains positive, rent growth continues to trail more typical spring leasing seasons as elevated apartment supply limits landlords’ ability to push rents higher.

Get Smarter about what matters in CRE

Stay ahead of trends in commercial real estate with CRE Daily – the free newsletter delivering everything you need to start your day in just 5-minutes

A Slower-Than-Normal Spring Leasing Season

The latest figures suggest the apartment market remains stable but far from overheating. Monthly rent growth has held steady since late 2025 after a period of flat-to-declining performance during the second half of last year.

CoStar Analytics noted that both March and April 2026 were revised upward from initially reported 0.2% gains to 0.3%, indicating slightly stronger demand than first estimated. Even so, annual rent growth remained unchanged at 0.7% in May, well below the 1.3% year-over-year increase recorded in May 2025.

The Details

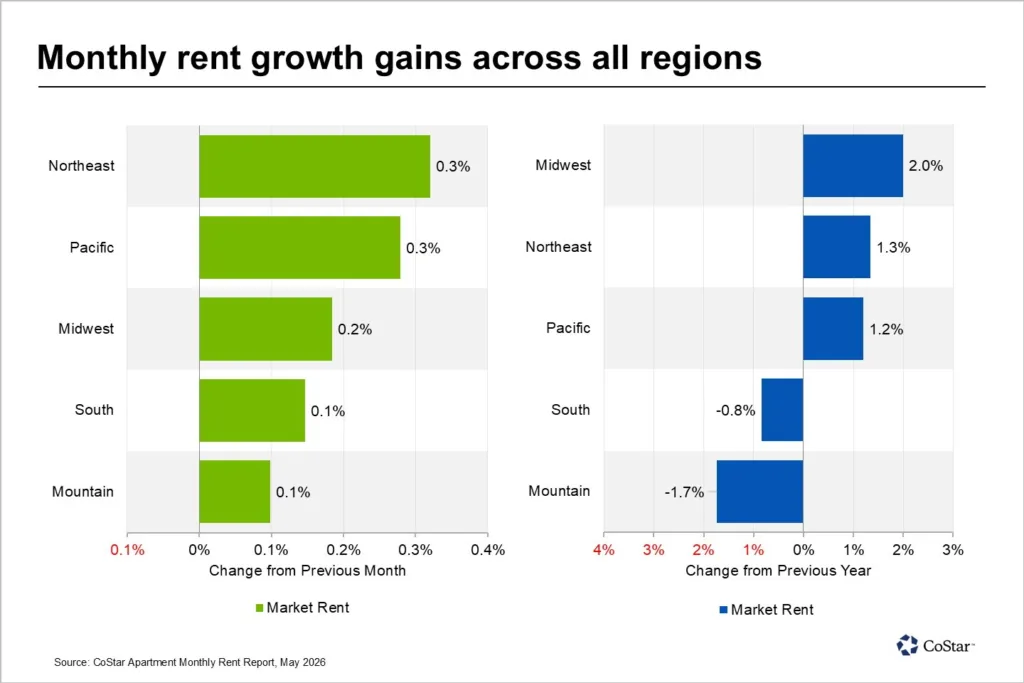

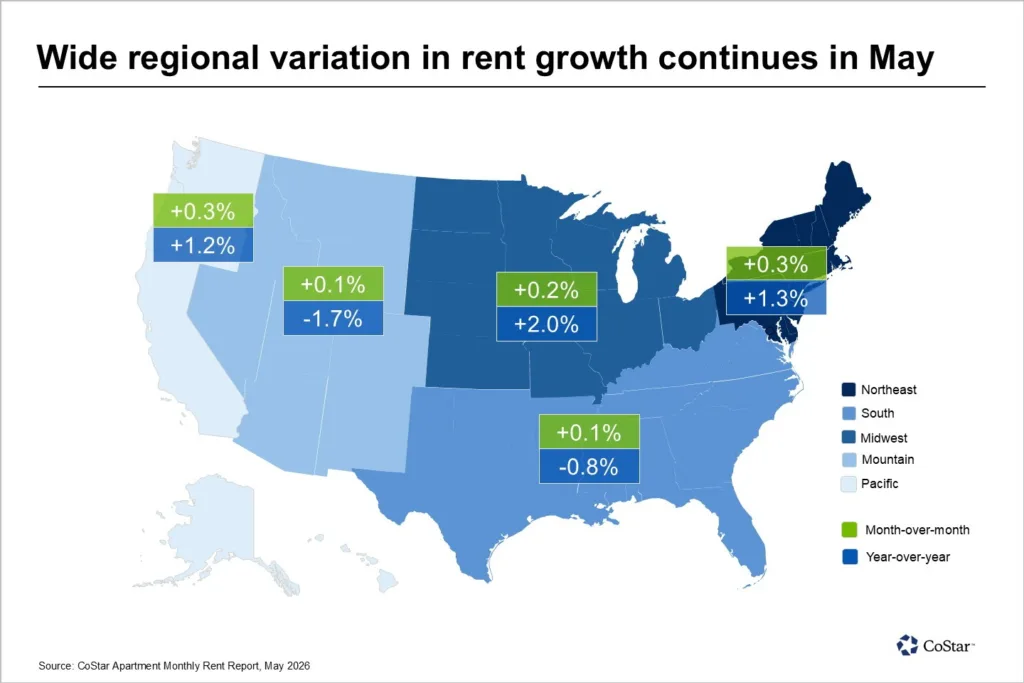

Regional performance was broadly positive in May, with all five major US regions posting monthly rent increases. The Northeast and Pacific regions led the country with 0.3% monthly growth, followed by the Midwest at 0.2%. The South and Mountain regions each recorded more modest 0.1% gains.

Year-over-year trends painted a more uneven picture. The Midwest led annual rent growth at 2.0%, according to Apartments.com data, followed by the Northeast at 1.3% and the Pacific region at 1.2%.

Meanwhile, the South and Mountain regions remained under pressure, posting annual rent declines of 0.8% and 1.7%, respectively. Markets with large volumes of recently delivered apartments continue to face the greatest challenges in achieving rent growth.

At the metro level, 43 of the nation’s 50 largest apartment markets recorded monthly rent increases in May. San Jose posted the strongest monthly gain at 1.2%, followed by Tucson at 0.9% and San Francisco at 0.8%.

On an annual basis, San Francisco remained the standout performer, with rents rising 8.4%, followed by San Jose at 4.9%, Norfolk at 4.4%, and Chicago at 2.9%, according to CoStar Analytics.

Supply-Heavy Markets Remain Under Pressure

The biggest rent declines continue to occur in markets where apartment deliveries have significantly outpaced demand. Austin and San Antonio each recorded annual rent declines of 3.3%, while Denver posted a 3.1% drop and Las Vegas fell 2.5%.

The divergence highlights how local supply conditions increasingly determine performance. Pacific Coast markets such as San Francisco and San Jose have benefited from more constrained new development pipelines, while Sun Belt markets that experienced aggressive construction activity during the past several years are still working through excess inventory.

The result is a bifurcated multifamily landscape where strong job growth alone is no longer enough to support rent increases if new supply remains abundant.

Why It Matters

For apartment owners and investors, the data reinforces a central theme shaping multifamily performance in 2026: demand remains healthy, but supply remains the dominant force influencing rent growth.

National rent gains have stabilized, yet landlords in many markets continue to compete aggressively for tenants through concessions and promotional offers. Markets with limited new construction are regaining pricing power faster, while high-delivery metros face a longer recovery period.

The uneven performance also creates opportunities for investors seeking stronger rent growth in supply-constrained regions such as the Midwest, Northeast, and parts of the Pacific Coast.

What’s Next

The outlook for multifamily rent growth will largely depend on how quickly excess inventory is absorbed. CoStar Analytics noted that apartment construction activity has begun to slow across many markets, which should gradually reduce supply pressure over time.

New apartment development has slowed sharply nationwide, pushing construction starts to their lowest level in 15 years. That trend could help restore pricing power as excess inventory is absorbed.

However, a substantial inventory overhang remains in place entering the second half of 2026. Until absorption catches up with recent deliveries, national rent growth is likely to remain positive but modest, with local supply conditions continuing to drive winners and losers across the apartment sector.